Company Overview: James Hardie Industries Plc is a manufacturer of fiber cement products and systems for internal and external building construction applications in the United States, Australia, New Zealand, and the Philippines. The Company's operating segments are North America and Europe Fiber Cement, and Asia Pacific Fiber Cement. The North America and Europe Fiber Cement manufactures fiber cement interior linings, exterior siding products and related accessories in the United States. The Asia Pacific Fiber Cement includes fiber cement manufactured in Australia, New Zealand and the Philippines, and sold in Australia, New Zealand, Asia, the Middle East (Israel, Saudi Arabia, Lebanon and the United Arab Emirates) and various Pacific Islands. The Company offers a range of fiber-cement building materials for both internal and external use across a range of applications, including external siding, internal walls, floors, ceilings, trim, fencing and facades.

.png)

JHX Details

Synergistic Acquisition of Fermacell- Catalyst for Future Growth: Dual-listed company, James Hardie Industries PLC (ASX: JHX, NYSE: JHX) is one of the leading manufacturers of fiber cement building materials products and systems for internal and external building construction applications in the United States, Australia, New Zealand, and the Philippines. As on July 15, 2019, the market capitalization of James Hardie stood at ~A$8.38 billion. The company recently released an annual review for the fiscal year 2019 in which the company stated that they are aggressively driving organic growth above the market throughout all the businesses as well as geographies. The company stated that substantial deployment towards people, plants and market development programs, has enabled it to maintain the strategic industry leadership and create profitable growth and deliver long-term returns. The company also released its results for Q4 FY 2019 which ended in March 2019. The company’s adjusted net operating profit amounted to US$73.8 million for Q4 FY 2019 while, for the full year, the figure stood at US$300.5 million. The company’s net sales amounted to US$624.8 million for the quarter and, for the full year, it was US$2,506.6 million. The following image provides a breakdown of the net sales by the operating segment:

.png)

Breakdown Of Net Sales (Source: Company Reports)

The company stated that, on April 3, 2018, they have wrapped up the acquisition of Fermacell involving an aggregate purchase price amounting to €516.4 million. After the acquisition of Fermacell, the company happens to be a market leader with respect to the European dry lining business, especially in Germany. The company markets gypsum and cement-bonded boards under the Fermacell® brand and its fire-protection boards under the AESTUVER® brand.

Moving forward, there are expectations that the respectable liquidity levels might help the company when it comes to making deployments towards the strategic business objectives. Also, sound operational capabilities can support its long-term growth prospects.

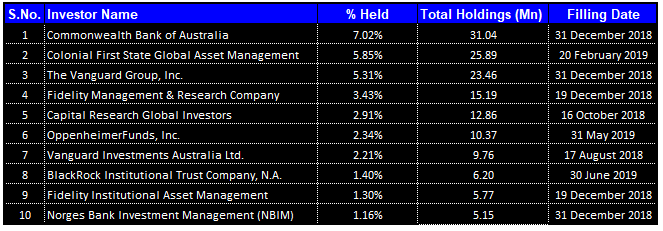

Top 10 Shareholders: The following table provides a broad overview of the top 10 shareholders in James Hardie Industries PLC:

Top 10 Shareholders (Source: Thomson Reuters)

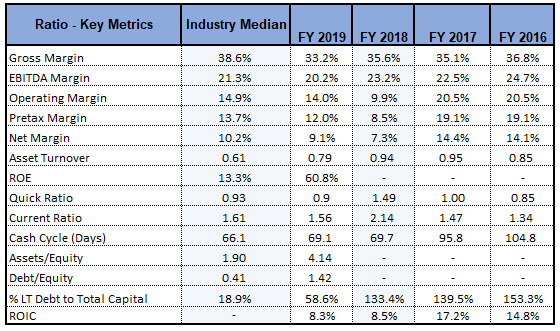

Decent Key Metrics: JHX’s key financial ratios have witnessed an improvement in FY19 as its net margin stood at 9.1%, reflecting a rise of 1.8% on the YoY basis that implies that the company had improved its capability to convert its top line into the bottom line. Also, its operating margin stood at 14.0% in FY19, a YoY improvement of 4.1%. Current ratio stood at 1.56x in FY19, indicating decent liquidity level to meet its short-term obligations. Talking about the leverage ratios, the company’s long-term debt as a percentage to total capital stood at 58.6%, which has fallen 74.8% on the YoY basis. Moreover, the company is generating better returns for its shareholders than its peers as the company reported an ROE of 60.8% in FY19 as compared to the industry median of 13.3%.

Key Metrics (Source: Thomson Reuters)

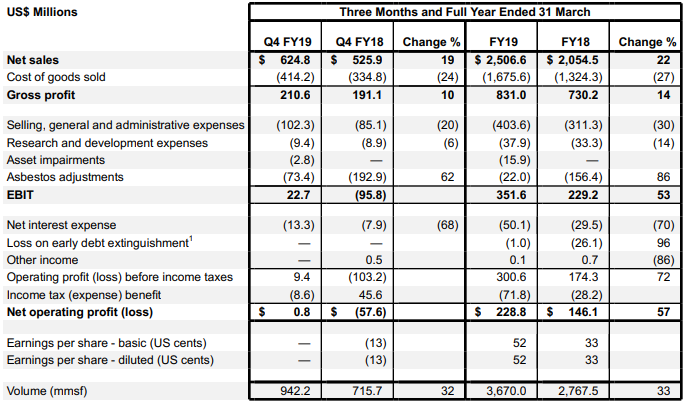

Understanding JHX’s Q4 FY 2019 Results: In Q4 FY19, James Hardie Industries PLC stated that its North America Fiber Cement segment had witnessed the revenue growth of 3% for the quarter as well as 6% for the full year and it also generated good EBIT margins within the target range amidst challenging input cost environment. Additionally, the company stated that The North America housing market demand was soft throughout most of the geographies as well as customer segments in the last 6 months of the fiscal year 2019. In Q4 FY19, the company’s Asia Pacific Fiber Cement segment’s EBIT margin stood at 20.0% while, for the full year, the figure stood at 22.3%.

Overview of Results (Source: Company Reports)

The company stated that its Asia Pacific Fiber Cement segment had witnessed decent top-line growth of 7% and 11% in Australian dollars for the quarter and full year, respectively. In conclusion, it was mentioned that the consolidated group results had reflected good as well as disciplined financial performance in the significant inflationary cost environment.

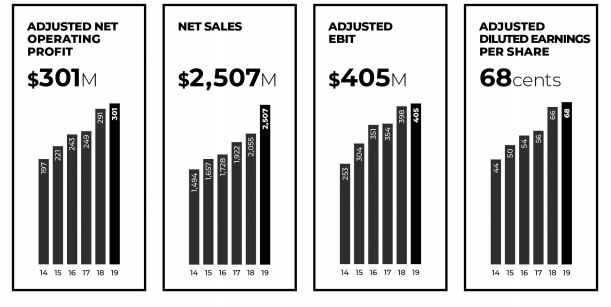

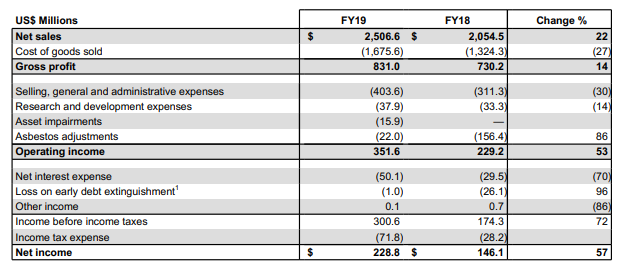

Respectable Financial Performance Witnessed in FY19: JHX’s operating results for the fiscal year 2019 had reflected good as well as disciplined financial performance in the significant inflationary cost environment, and its adjusted net operating profit amounted to US$300.5 million while adjusted earnings before interest and taxes stood at US$404.6 million, reflecting a rise of 3% and 2%, respectively, as compared to the fiscal year 2018. Additionally, the company witnessed net sales amounting to US$2.5 billion, reflecting a rise of 22% as compared to the fiscal year 2018.

Key Financial Measures (Source: Company Reports)

With respect to capital expenditures, the company utilizes a mix of operating cash flow and debt facilities in order to finance the capital expenditure projects and investments. The company continuously deploy towards safety, equipment maintenance and upgrades, and capacity in order to ensure continued environmental compliance as well as operating effectiveness of the plants.

Key Takeaways From 2019 Annual General Meeting Pack: James Hardie Industries PLC had recently released 2019 annual general meeting pack in which it stated that the Net sales for the fiscal year 2019 got favorably impacted by acquisition of Fermacell in Europe as well as higher net sales in the North America Fiber Cement and Asia Pacific Fiber Cement segments. North America Fiber Cement Segment’s net sales for the fiscal year 2019 got favorably due to higher sales volumes and higher average net sales price.

The company’s net income witnessed a rise from US$146.1 million in the fiscal year 2018 to US$228.8 million in the fiscal year 2019, mainly because of the favorable movement in asbestos adjustments as well as higher gross profit. The company’s gross profit amounted to US$831.0 million for the fiscal year 2019, which reflects a rise of 14% as compared to the fiscal year 2018. Its gross profit margin stood at 33.2% for the fiscal year 2019, which was 2.3 percentage points lower than the fiscal year 2018. The company stated that, in the Asia Pacific region, it primarily sells into the Australian, New Zealand and Philippines markets, and residential building industry represents principal market for fiber cement products.

Operating Results (Source: Company Reports)

What to Expect from JHX Moving Forward: James Hardie Industries PLC stated that there are expectations for the modest growth in the US housing market in the fiscal year 2020. It added that the single-family new construction market and repair and remodel market growth rates might grow in the fiscal year 2020, though at the growth rate which would be lower than that in the fiscal year 2019. The company also anticipates new construction starts between around 1.2 million and 1.3 million. Additionally, there are expectations that North America Fiber Cement segment EBIT margin would be in the top half of the range of 20%-25% for the fiscal year 2020. The expectation is based upon the company continuing to improve the operating performance in plants, improved net average sales price and mix, continued inflation for the input costs as well as modest underlying housing growth.

With respect to Australia, there are expectations that the addressable underlying market would be decreasing in the fiscal year 2020 as compared to the fiscal year 2019. Additionally, the company expects that its Europe Building Product segment would be achieving YoY net sales and EBIT margin growth.

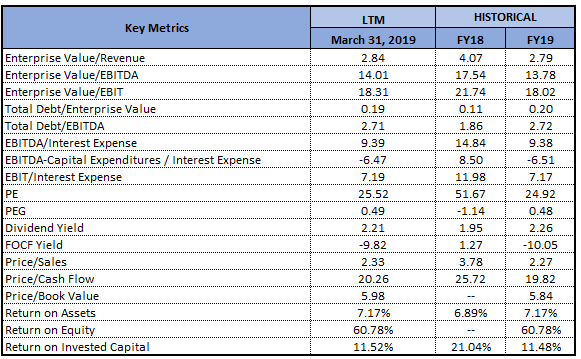

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: The stock of James Hardie Industries PLC had delivered the return of 24.62% in the span of previous six months while, in the time frame of past three months, the stock’s return stood at 2.01% which can be considered at respectable levels. From the analysis standpoint, the company’s stock seems to be attractive as JHX witnessed a CAGR growth of 10.90% in the time span of FY 2015- FY 2019 in its top line which can be considered at respectable levels and, thus, it looks like its revenue-generation capabilities might support its future growth prospects.

Additionally, the company is possessing sound operational capabilities as its cash from operating activities have witnessed the CAGR growth of 12.51% between the time frame of FY 2015- FY 2019. Also, the company’s key personnel stated that FY19 marks the start of a critical transformation that would be launching the next phase of growth at JHX. Moving forward, there are expectations that the company’s global presence, respectable revenue-generation capabilities, and sound operational capabilities might act as the key growth catalysts and can attract the attention of the market players. Based on the foregoing, we have valued the stock using consensus EPS for forward 24 months close to $1 and industry P/E multiple of low double-digit and arrived at a target price upside of about high single digit (in %). Hence, considering the aforesaid parameters, we give a “Buy” recommendation on the stock at the current market price of A$18.890 per share (up 0.586% on 15 July 2019).

JHX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...