Company Overview - iSelect Limited (iSelect) is an online-driven comparison service that compares insurance, household utilities and personal finance products. The Company operates in two segments: Health and Car Insurance, and Household Utilities and Financial. The Health and Car Insurance segment offers comparison and referral services across private health insurance and car insurance categories. The Household Utilities and Financial segment offers comparison and referral services across a range of household utilities and personal financial products, including life insurance, broadband, retail electricity and gas products, home loans, savings accounts, term deposits, credit cards and personal loans. iSelect has two brands: iSelect (www.iselect.com.au) and InfoChoice (www.infochoice.com.au).

Analysis – iSelect (ISU) has a strong brand, differentiated customer service model and established scale that supports its market leadership in online product comparison. We expect strong growth underpinned by online consumer trends, favourable industry drivers in private health and a normalisation in demand following regulatory change, as well as rapid growth from the newer business units. Cash flow conversion is improving quickly as growth in upfront fees outstrips trail commissions and a strong balance sheet supports potential acquisitions in a fragmented industry. We believe the health business model should deliver double digit growth on average over the next few years, driven by a combination of – (1) a recovery in market demand for health comparison following a subdued FY13 due to increased prepayments in FY12. (2)Mid-high single digit percentage private health premium inflation (3) Above industry growth from ISU’s product providers. (4) Scope for further improvement in the conversion rate ratios. The outlook is complemented by strong growth potential in other divisions like energy and car insurance where online demand is growing and penetration is fairly low.

iSelect Group Portfolio (Source - company Reports)

iSelect Group Portfolio (Source - company Reports)

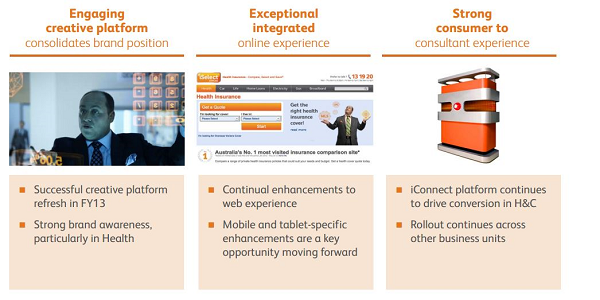

ISU is well placed to benefit from technological developments and consumer preferences that support continued growth in online transacting as well as increased customer desire and propensity to use the internet to more easily search and compare products, maximise value for money and make informed purchasing decisions. ISU has invested significantly in marketing ($110m since inception), resulting in high levels of awareness in the iselect brand and strong organic search positioning. This in turn has led to a degree of first mover advantage and market leadership in traffic to its website. ISU also utilises a differentiated blended/offline model. This makes use of a consumer advice contact centre to receive inbound calls and act as a follow up channel which together with sophisticated needs analysis and data mining, drives high conversion levels ( well ahead of typical online averages ) and increases profitability.

Exceptional Customer Experience (Source - Company Reports)

Exceptional Customer Experience (Source - Company Reports)

iSelect is by far the largest health product comparison business and we believe sold an estimated 15-20% of all new private health insurance policies in FY13. The private health insurance industry is underpinned by government regulation, an ageing population, inflation driving premium price increases (mid to high single digit percentage) and scope for further penetration of online comparison, all of which support an attractive long term growth outlook. In addition to health insurance iSelect has developed businesses across a range of industries which provides numerous opportunities to leverage off its brand presence and established platform and expand the online comparison channel into large markets where penetration is currently fairly low. Cash flow conversion is steadily improving. This is due to various factors including some health funds which originally paid trail commissions changing to paying upfront fees and fast growing businesses typically receiving a greater proportion of upfront fees. A experienced management team has overseen strong historic growth at the same time as constantly developing the business to enhance brand and scale and expanding comparison services into new industries. A solid balance sheet and iSelect’s market leadership in a fragmented industry could also afford acquisition opportunities.

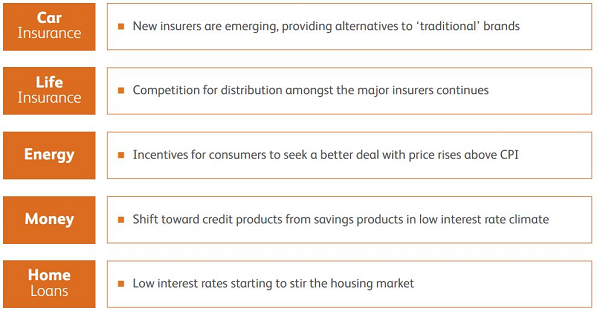

Dynamics Across other Underlying Markets (Source - company Reports)

Dynamics Across other Underlying Markets (Source - company Reports)

Some of the key risks associated with ISU are: (1) There are numerous competitors in the product comparison industry. While most of them are significantly smaller than iSelect, the company could face increased competition. (2) All the sectors iSelect operates in are subject to regulation, which could impact consumer behaviour, affect customer demand or change the way iSelect offers its comparison services and communicates with customers. (3) Various factors could negatively impact consumer traffic to iSelect websites such as in adequate website performance, changes to search engine algorithms, ineffective marketing, security breaches or negative publicity. (4) Cash receipt from trail commissions may be lower than expected. The ultimate receipt of trail commission cash is dependent on customers staying with the product provider. (5) Already high penetration in the insurance market. (6) Some of iSelect’s newer businesses are relatively immature and may fail to reach desired scale, or require greater investment or time than anticipated.

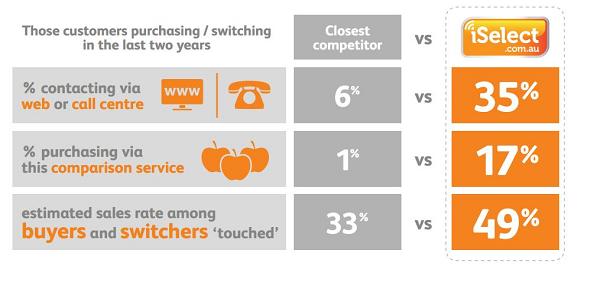

iSelect Leads the market for private health insurance. (Source - company Reports)

iSelect Leads the market for private health insurance. (Source - company Reports)

ISU’s 1H14 result was solid achieving guidance. However the 2H14 outlook was muted. ISU guided to FY14 EBITDA to exceed FY13 and revenue growth to exceed EBITDA growth. It pointed to increased 2H overheads (investment in data mining and partner programs) and increased marketing (Energy). 1H14 revenue and EBITDA both met guidance after normalising for CEO exit/replacement costs, cash flow conversion was ahead of our estimates and the ratio of upfront/total revenue continues to tick upwards. The result was made more impressive when considering it included a $1.7m negative revaluation of the trail commission book, comprising a $2.4m negative impact on the health book, offset somewhat by a positive revaluation on the residual business trail book. A negative revaluation did not come as a surprise to us given the extent of disruption in the private health industry through higher churn levels that have followed the introduction of means testing for the health insurance rebate. This is completely consistent with the commentary from the health insurers themselves. We understand the drivers behind the increased cost and like their strategy to manage and grow the business in the long term.

ISU Daily Chart (Source - Thomson Reuters)

ISU Daily Chart (Source - Thomson Reuters)

Looking to FY15 our belief that the energy channel will grow, an expectation of similar trends in the Health Insurance and continued growth off a low base from other verticals underpin our expectation that ISU will maintain a strong momentum in revenue growth. We find valuation at current levels to be inexpensive which is the main driver behind a BUY recommendation at the current price of $1.075.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...