Kalkine has a fully transformed New Avatar.

I. Sector Landscape and Outlook

Telecommunication is the lifeline of our society, supporting the entire economy and influencing how we live and work in today’s rapidly evolving environment. Most of the major telecommunication service providers have relatively secure recurring revenues from mobile, television and internet customers. Besides, the 24/7 criticality of the telecom space makes it kind of a safe bet for investors who hold stocks for long-term to infuse stable income into their portfolio of a different asset class.

Today’s digital world is made possible thanks to the telecom sector. It plays an important role in people’s lives, and it would not be amiss if we consider telecom expenditure more of a non- discretionary in nature. And, their importance has been demonstrated in the current environment as a result of the restrictions that have been put in place. When most of the businesses have been closed amid coronavirus outbreak, telecom sector players are experiencing a sharp jump in demand for their services and uninterrupted operation of critical communications networks. Thus, understanding the sector landscape becomes crucial.

NBN – Changing the Telecom Market Dynamics:NBN, initiated by the Federal Government in April 2009, is designed to ultimately become the predominant wholesale provider of fixed line access services in Australia. NBN project is expected to play a transformative role in the future telecommunications landscape of Australia, as its use, upgrades and integration with private sector services would have a significant impact on quality, accessibility, and affordability of the services delivered.

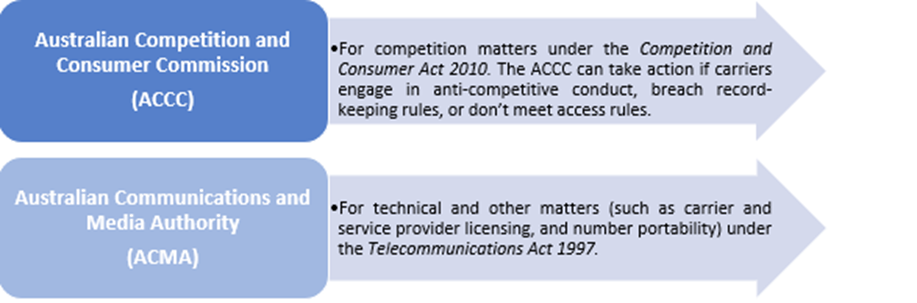

The telecommunications sector in Australia is regulated by the Australian Communications and Media Authority (ACMA) and the Australian Competition and Consumer Commission (ACCC).

Fig 1: Telecom Regulators in Australia

Source: Kalkine's secondary research

Australia’s telecommunications ecosystem can be defined as broad with healthy competition. Entry is open to all telecommunications markets with minimal requirements concerning entry and ongoing operations.

There are two kinds of operators-

- Carriers are those that operate key telecommunications facilities

- Service Providers are those that use a carrier’s facilities to provide axillary services such as internet, phone, or TV services to the public

The Australian telecom market is ruled by mobile broadband and Fibre-to-the-Node (FttN) services. New fibre technologies are replacing aged technologies in the sector. Traffic from the fixed line telephony has reduced significantly, contributing much lower revenues to the telecom market. Fixed-line DSL broadband and copper networks have declined with fibre and fixed wireless broadband services garnering demand following the wider availability across Australia. The expanded availability can be credited to NBN's multi-technology architecture, with NBN activations increased to 10.5 million premises in FY18/19.

Let’s now delve into the competitive landscape of this sector.

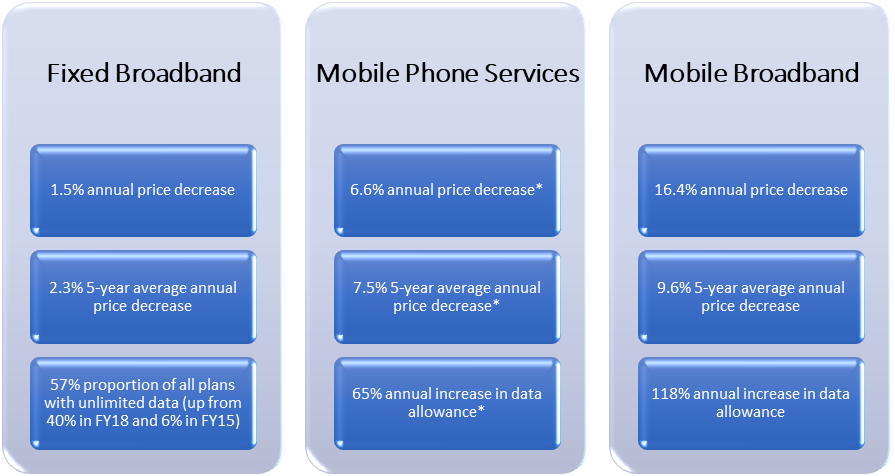

Fig 2: Competition and Price Changes in Australian Telecommunication services in 2018-19

* compound average 2014–15 to 2018–19

Source: ACCC Communications Market Report 2018–19

Major players operating in the Australian telecom market include telecommunications and information services provider Telstra Corporation Limited, consumer, wholesale and corporate telecommunications services provider TPG Group, telecommunication services provider Singtel Optus Pty Ltd (Optus) and Australia’s specialist fibre and network solutions provider Vocus Communications Limited (Vocus Group).

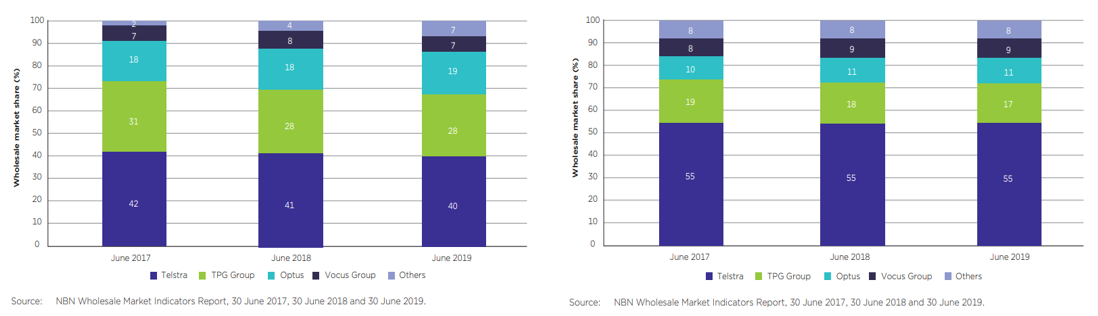

National market shares on the NBN broadband services nationwide (June 2019):According to NBN Wholesale Market Indicators Report, Telstra holds 49%, while TPG Group, Optus and Vocus Group account for 22%, 14% and 8%, respectively.

By access technology, of the total market share in wholesale fibre-based services, Telstra accounted for 49%, reflecting a decline of 1 percentage point when compared with the same period a year ago. The two other key players - TPG Group and Vocus also lost 1 percentage point year-on-year, while Optus registered a year-on-year increase of 1 percentage point. For number of fixed wireless services, Telstra accounted for 55%, with TPG Group and Optus capturing 14% and 10%, respectively.

In terms of region, Telstra accounts for the dominating position in regional areas, while TPG Group and Optus hold the majority market share in metropolitan areas. Meanwhile, Vocus holds almost the same market share in regional as well as metropolitan areas.

Market shares for fixed broadband services: Telstra dominated the market share in the retail market for fixed broadband services with a 49% stake, followed by TPG Group and Optus with 25% and 15%, respectively.

Market shares for mobile phone services: Telstra captured a market share of 41%, with Optus and Vodafone Hutchison Australia (VHA) accounting for 27% and 19%, respectively.

Retail market share for fixed line voice services: Telstra and Belong (57%), TPG Group (21%), Optus (19%) and Vocus Group (3%).

It is pertinent to look at the driving forces within the sector’ let’s have a quick look at the same.

Factors Driving Australian Telecom Sector

Light-speed innovation, technological developments and consumer preferences are shaping the telecom industry, with the following major forces shaping the future for the Australian telecom sector.

The Voice to Data Revolution – A quick shift from voice to data is resulting in revolutionary changes in the revenue mix, a major challenge for wholesale carriers. There is a consistent decline in the conventional wholesale voice business, with an exponential increase in data consumption, on account of VoIP services enabling audio call, messaging or even seamless video calls for a longer period and free of cost to customers without the need for payment to network providers.

The emergence of Amazon Prime, Netflix and other OTT services, in addition to video on-demand services such as Telstra TV Box Office and many IPTV players such as Flip TV, are other factors leading to the data revolution.

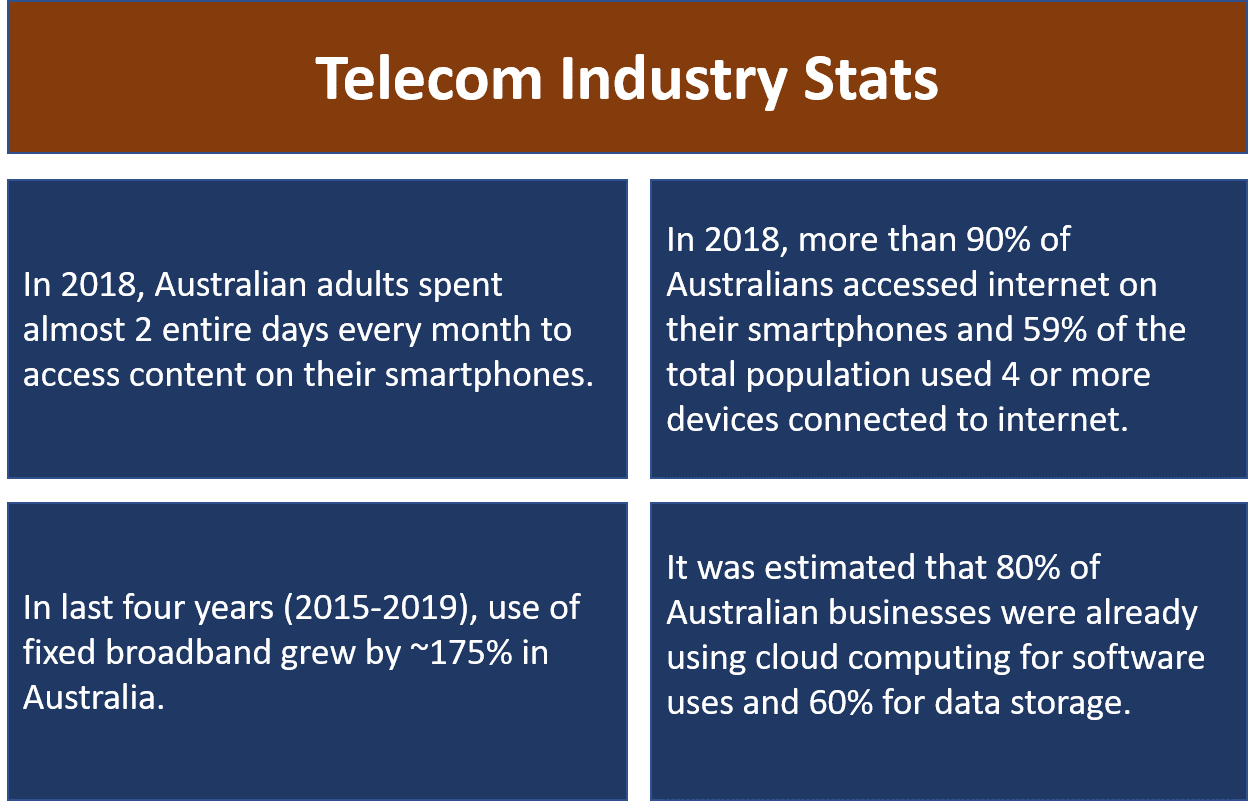

Fig 4: Key Industry Statistics

Source: Kalkine's secondary research

As at June 2019, 35.82 million mobile voice and data services remained in operation in Australia, representing a 2.8% increase year-on-year, while the number of homes and businesses connected to the NBN grew by 38% to 5.5 million and 83 per cent (approximately 16.4 million) of Australian adults had a smartphone. Internet subscriptions in Australia in June 2019 stood at 43.6 million, including 35.9 million mobile and 7.7 million fixed subscriptions.

Data consumption through cloud computing is anticipated to increase multi-folds in the upcoming years.Australia’s cloud Infrastructure-as-a-Service (IaaS) market is estimated to grow from $688 million in 2018 to $1.2 billion by 2022.

5G rollout to drive significant changes in mobile markets: Widespread adoption of 5G is expected to bring significant changes in mobile markets, offering huge benefits such as faster data speeds, ultra-reliability and low latency, and ability to separate services on the same network. 5G is expected to enable new revenue streams that do not exist today as well as delivering capital efficiency by reducing the cost per bit of data travelling over the network.

Australia is currently experiencing an early stage of 5G network rollout, including 5G mobile network infrastructure deployment by Telstra and Optus in select areas.

Before the pandemic, Telstra, the first Australian telco to launch 5G network and also a global leader in the development of 5G, had plans to roll out the first "millimetre wave " 5G customer trials during mid-2020. More than 4 million people now pass through the Company’s 5G footprint. By the end of FY19, the Company had already rolled out more than 320 5G enabled mobile base stations across the country in 10 cities nationally, with 5G coverage expected to fivefold over the next 12 months as a further 35 Australian cities and major towns are connected.

Australia could become one of the first countries to host a full-scale high-speed 5G network once more and more 5G mobile handsets are rolled out following the end of the coronavirus outbreak.

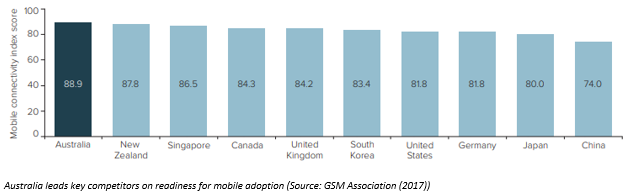

Fig 5: World Mobile Adoption

Internet of Things: A substantial growth opportunity for communication service providers lies with IoT as part of the growing mobile ecosystem.

IoT is a collection of devices that are connected to the internet and are added to things, enabling automation of varied household and business processes including virtual assistants, autonomous vehicles, smartwatches and smart home applications.

According to industry estimates by the Australian Communications and Media Authority (ACMA), the number of devices to be connected globally is expected to reach 29 billion by 2022. Of the total, more than 60% will relate to the IoT. Moreover, the

Bureau of Communications and Arts Research (BCAR) has estimated that by 2026, at least 50 IoT devices will be available in an average household in Australia.

Additionally, 5G introduction will accelerate the IoT growth in the country. IoT is expected to deliver a boost to the local economy worth up to $116 billion and a 2% increase in national productivity by 2025.

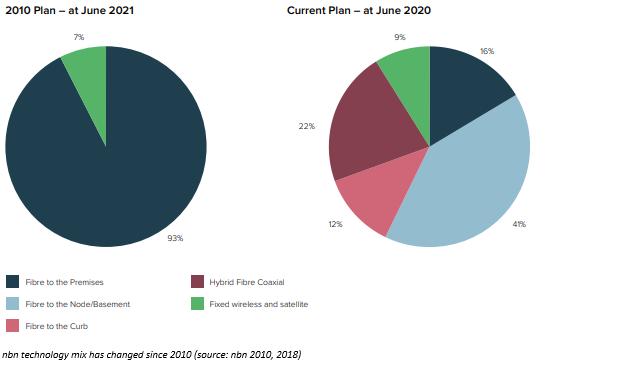

NBN Project: The NBN (National Broadband Network) project, expected to complete in 2020, is being undertaken by government corporation NBN Co Limited (trading as nbn) to upgrade the country’s existing phone and internet infrastructure. The project is designed to provide access to next-generation affordable, fast broadbandto all Australians, whether individuals or businesses, involving migration of consumers from other telcos’ network to the NBN.

Under the project, NBN is targeting to deliver access to peak wholesale download data rates of at least 25Mbps to premises and peak wholesale download data rates of at least 50Mbps to 90% of the fixed-line network. By the end of FY19, the network deployment and activations grew significantly, crossing more than 10.5 million premises and 5.5 million activations.

NBN Co has set itself ambitious revenue targets to recoup the significant cost of building its network, in addition to making payments to Telstra and Optus for migrating their customers from their legacy networks to the National Broadband Network. The Company is expected to become cash flow positive in 2023.

Fig 6: NBN Technology Mix

No analysis is complete if it does not address the challenge that has been posed by the novel coronavirus. Let’s look at the possible impact of COVID-19 on this sector.

COVID-19 Impact on Australian Telecom Sector

Amid the COVID-19 scenario, Telstra, holding more than 50% stake in the Australian telecom sector, has observed a sudden spike in demand for upgraded capacity in the enterprise market and mobile broadband in the consumer and small and medium business market. The Company has experienced a significant increase in requests for capacity upgrades across the corporate sector, with Telstra taking initiatives to bestow unlimited data on retail and small business fixed broadband.

According to Telstra, assessing the full impact or rather the long-term impact of COVID-19 is difficult in the current times. Though the impact on sector players is expected to be material, it is anticipated to be dependent on how the impact on the economy and their customers evolves.

Meanwhile, telecom players are making a significant contribution towards the national response and supporting their customers as they grapple with the challenge of shifting to working and studying from home in these unprecedented times.

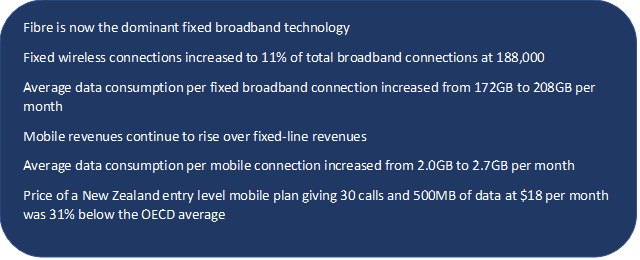

Fig 7: Few Facts About New Zealand Telecom Market – as of 2019

II. Investment Theme and Stocks under Discussion (TLS, CNU, TPG and VOC)

With the understanding of the sector, lets deep dive into 4 major telecom players that are well placed to capture the market opportunities in the coming few years. The stocks are evaluated based on ‘Discounted Cash Flow’.

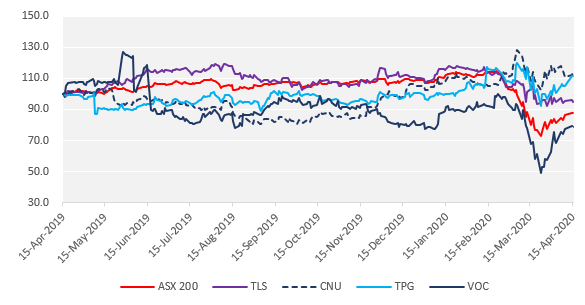

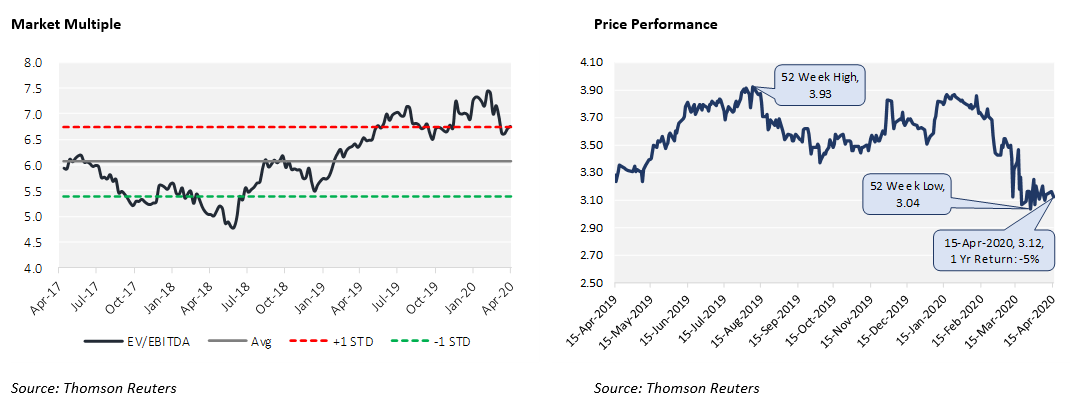

Fig. 8: Relative Performance of the companies under discussion against ASX 200

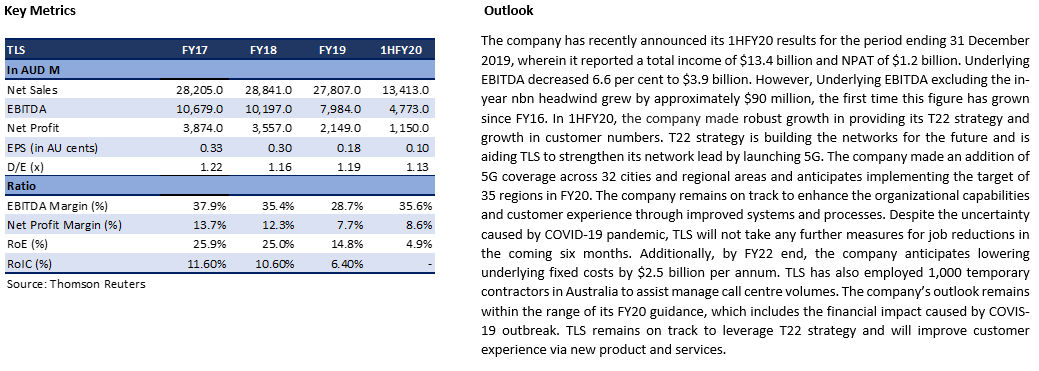

1. ASX: TLS (TELSTRA CORPORATION LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit)

Telstra Corporation Limited is engaged in providing telecommunications and information services, which includes mobiles, internet, and pay television. The stock is offering a dividend yield of ~4.6% on 15 April 2020 closing price.

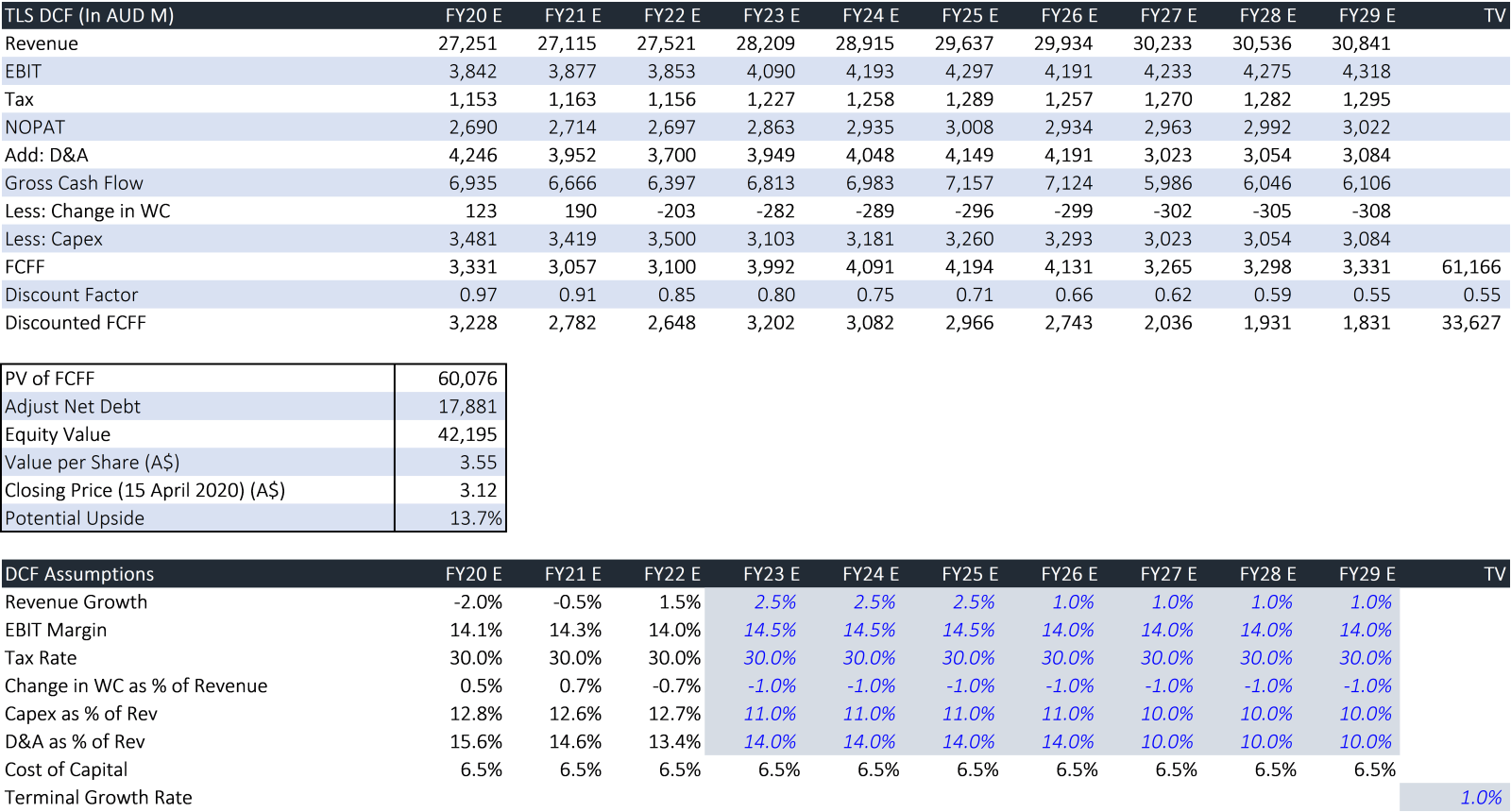

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~14% on 15 April 2020 closing price.

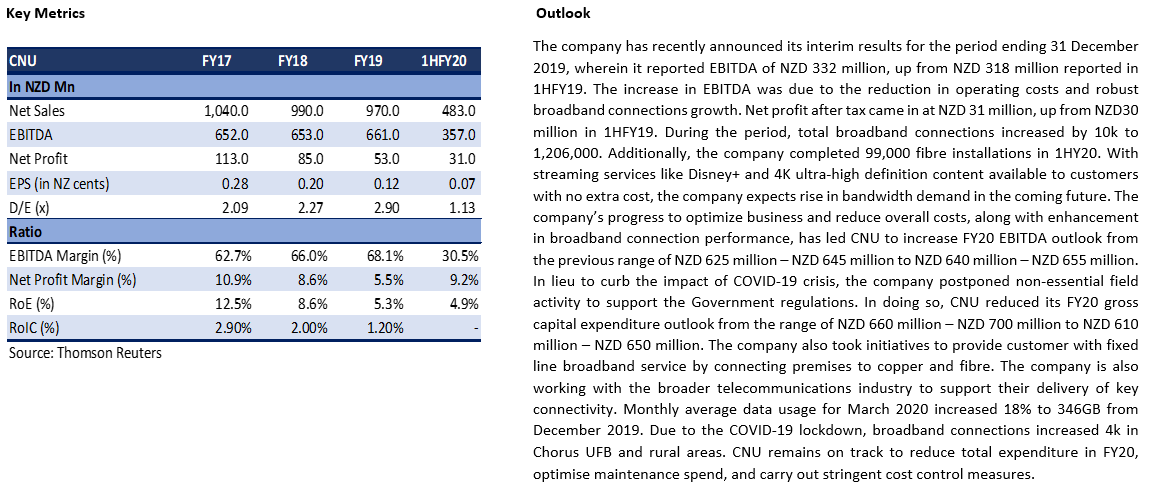

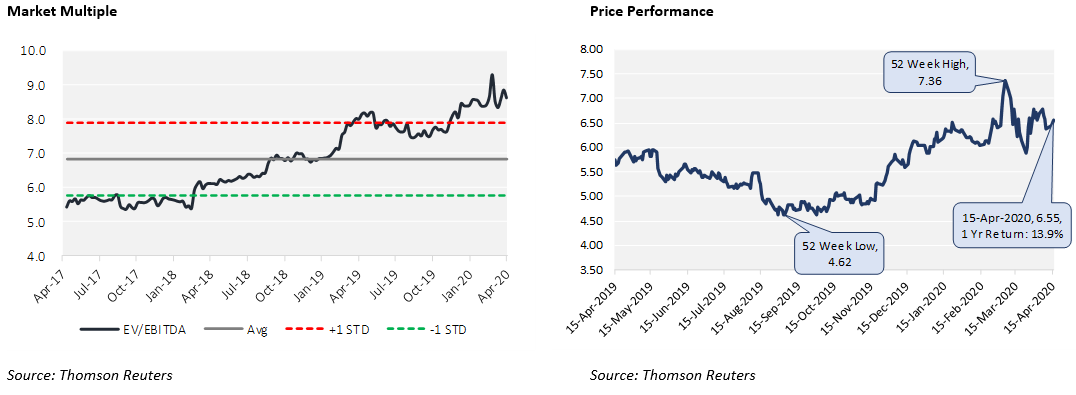

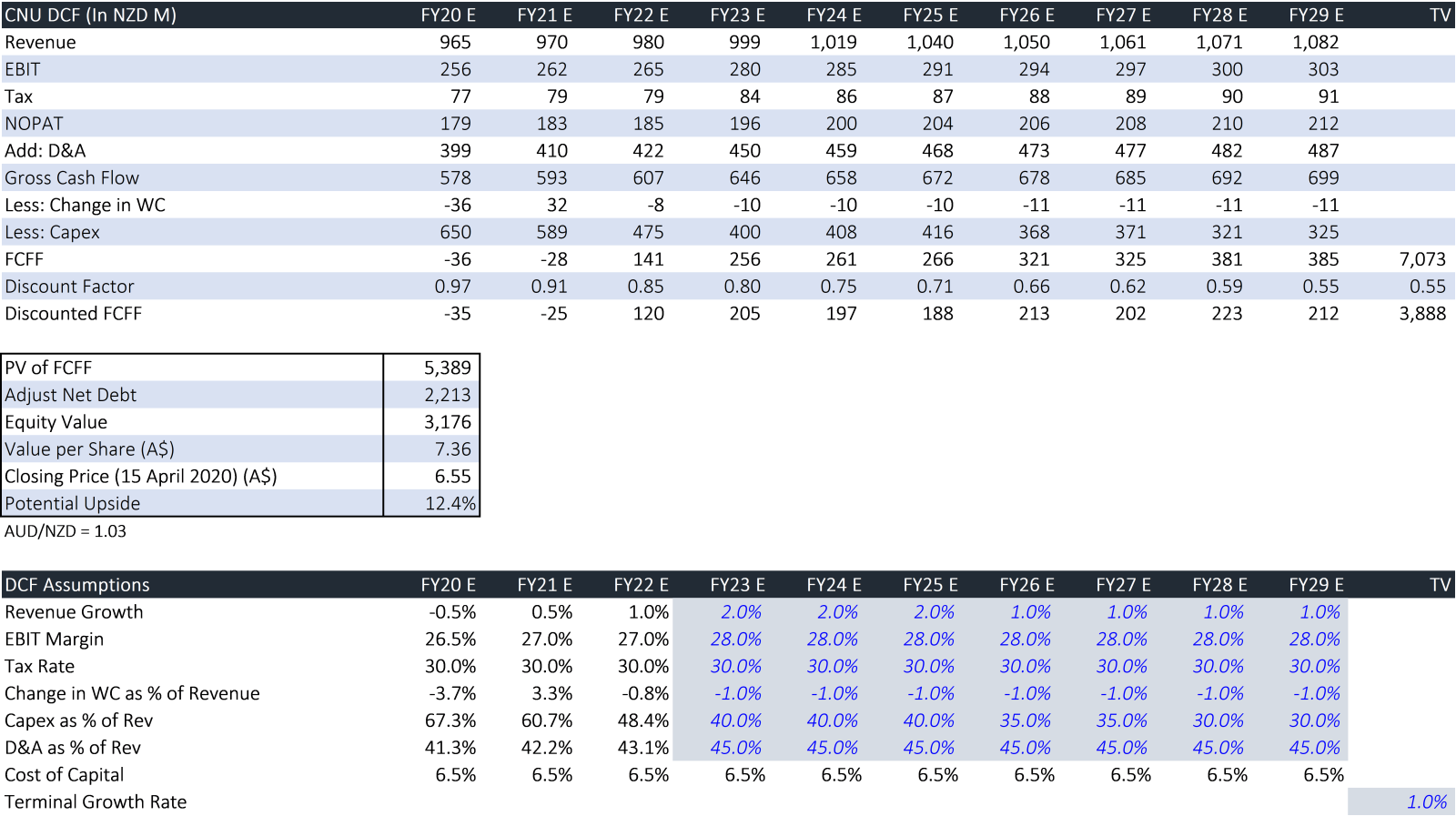

2. ASX: CNU (CHORUS LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit)

Chorus Limited is involved in the business of maintaining and operating nationwide fixed lines access network infrastructure in New Zealand. The stock is offering a dividend yield of 4.9% on 15 April 2020 closing price.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~12% on 15 April 2020 closing price.

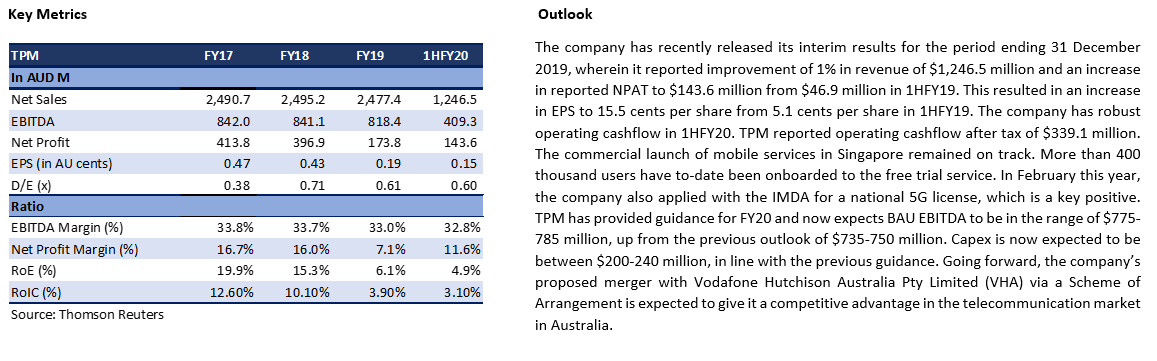

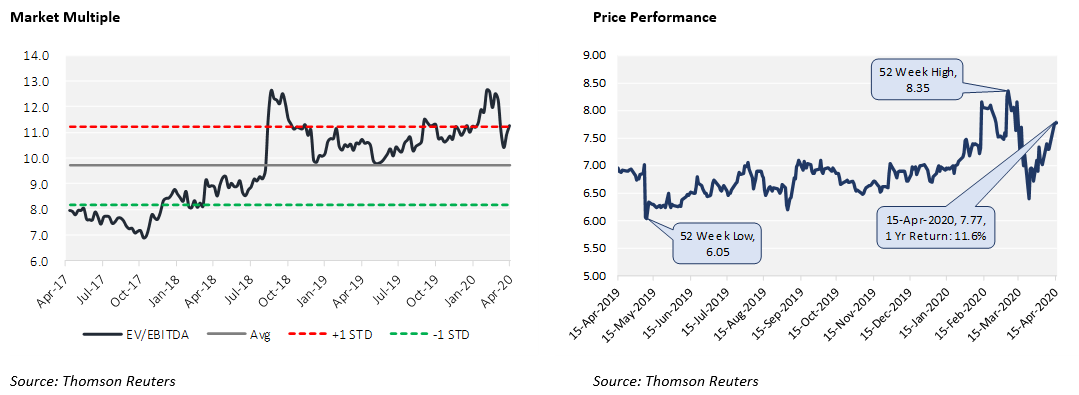

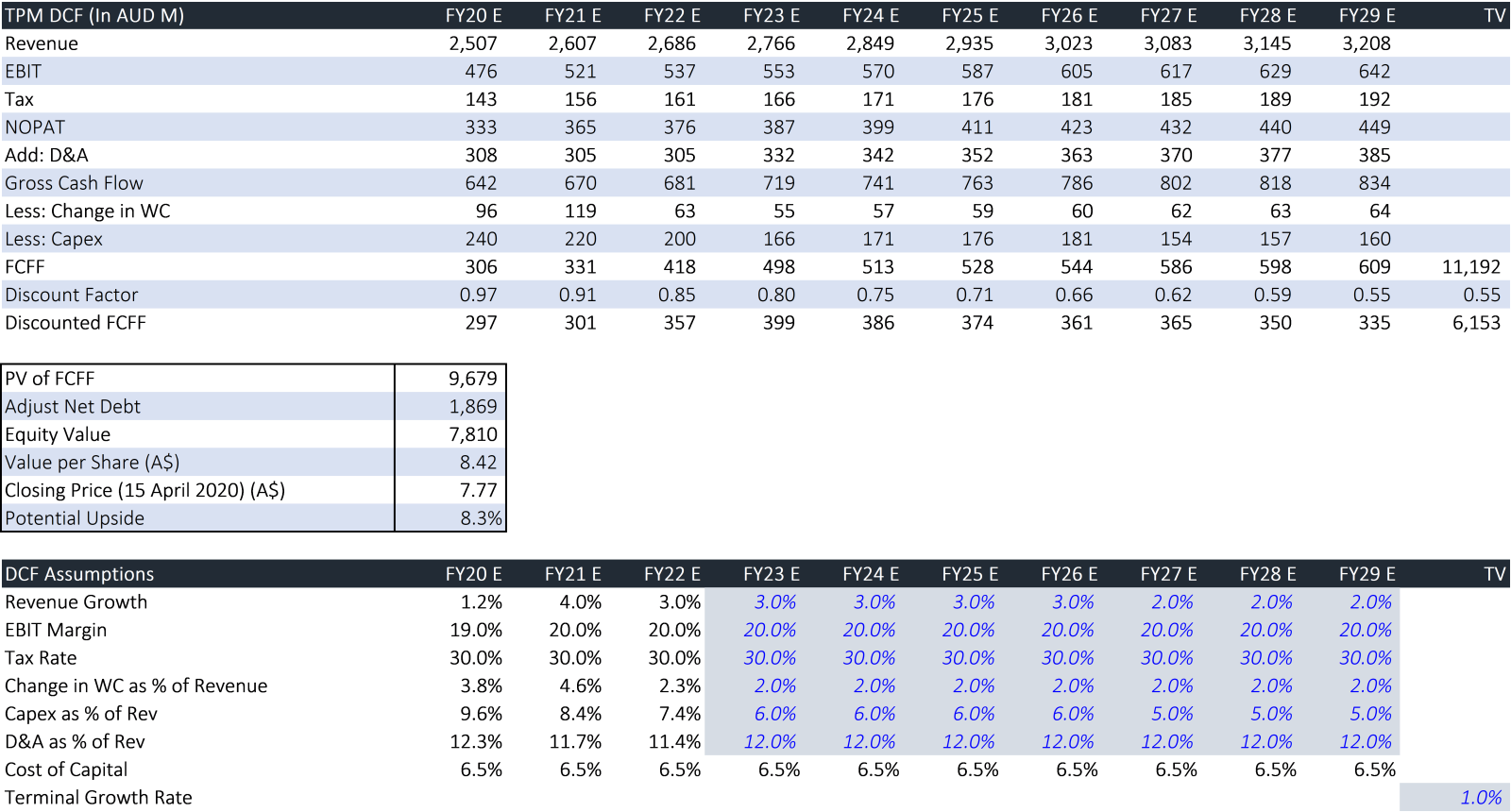

3. ASX: TPM (TPG TELECOM LIMITED)

(Recommendation: Hold, Potential Upside: High Single Digit)

TPG Telecom Limited offers consumer, wholesale, and corporate telecommunications services.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~8% on 15 April 2020 closing price.

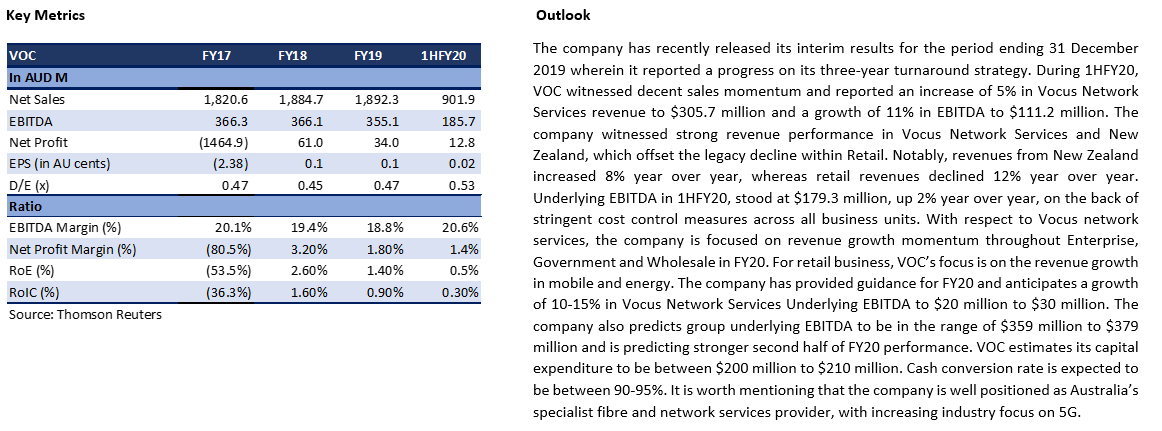

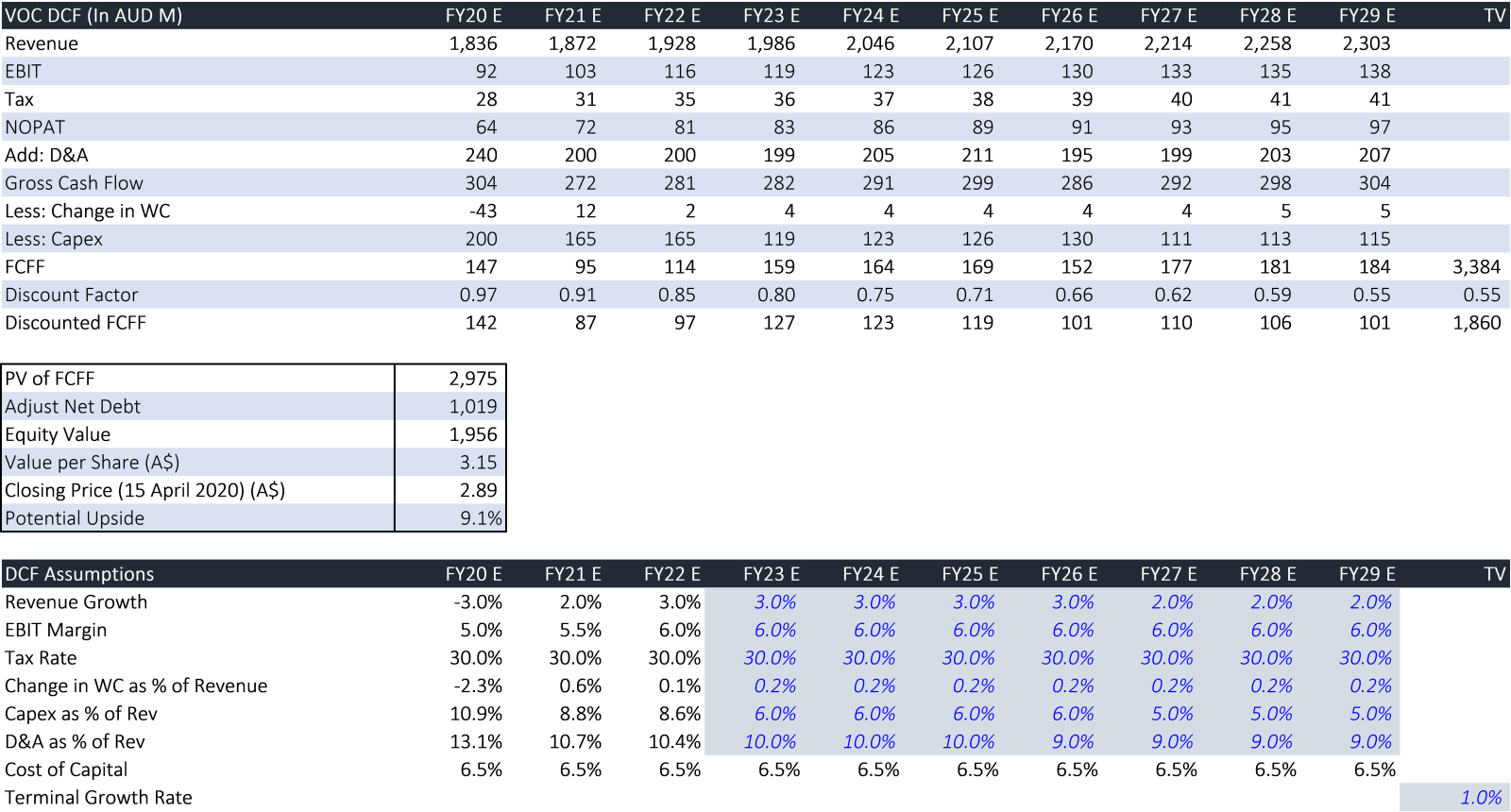

4. ASX: VOC (VOCUS GROUP LIMITED)

(Recommendation: Hold, Potential Upside: High Single Digit)

Vocus Group Limited is a telecommunications provider, which operates in Australian and New Zealand markets.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~9% on 15 April 2020 closing price.

Note: All the recommendations and the calculations are based on the closing price of 15 April 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters. All the recommendations are valid on 16 April 2020 price as well.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...