I. Sector Landscape and Outlook

Iron ore is the world’s most common element which forms over 80% of the earth’s inner and outer core. It is, in fact, the backbone of the infrastructure sector. Even during the unfavourable investment environment such as the current one when the US oil benchmark futures were seen to be dropping to the negative US$40 range, Iron ore stands tall as an outlier amongst most of the traditional commodities, despite the intrinsic market complexities and challenges of its own.

Iron has been for long associated with the development of an economy. We believe that post the coronavirus pandemic, Iron will continue to play an even stronger role in the recovery. To clearly understand the Iron ore industry; it is imperative to throw light on demand, supply, prices trends, as well as the innate issues of the sector.

In light of that, in this sector report, we have exhaustively examined the supply and demand within the industry to understand the pricing and competition and demystify the performance of the companies operating within the industry.

Understanding Demand and Supply Dynamics

The demand for iron ore is largely dependent on the demand for global steel. The steel market is anticipated to grow in the near to medium term with a major boost from infrastructure development but, with its unique stipulations. Let’s discuss the steel industry and the outlook for the same.

Steel and Iron Ore: The Intertwined Commodities

Almost 98% of the iron ore is used for the manufacturing of the steel. Steel market rules the demand for iron ore, with the processed product crude steel finds significant applications in the infrastructure development, construction, automotive and equipment sectors. The close association of the steel with the infrastructure development and construction sectors makes the developing world go to markets for steel. In the past few years, steel witnessed growth in demand in China, India, Africa and some regions of Europe.

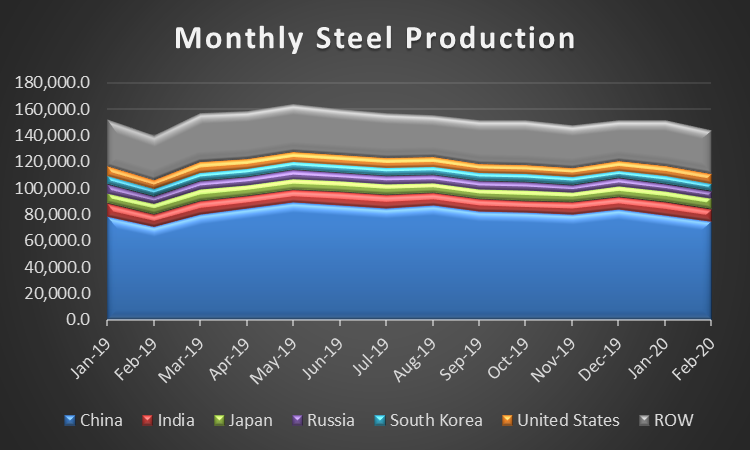

Despite the coronavirus outbreak, originating from Wuhan in Hubei province, China managed growth in the crude steel production to 154.7 million tonnes during the first two months of 2020, registering a growth of over 3% on a y-o-y basis. Global crude steel production also increased to almost 294 million tonnes increasing by almost 1.05% during January and February. Resumption of Chinese economic activities and the global recovery from the pandemic is likely to boost the steel demand during the remaining months of 2020 and 2021.

Fig 1: Monthly Steel Production

Source: World Steel Organisation

Now that we know about the Steel Industry let us ponder on the demand dynamics in the iron ore market.

What Drives the Demand for Iron Ore?

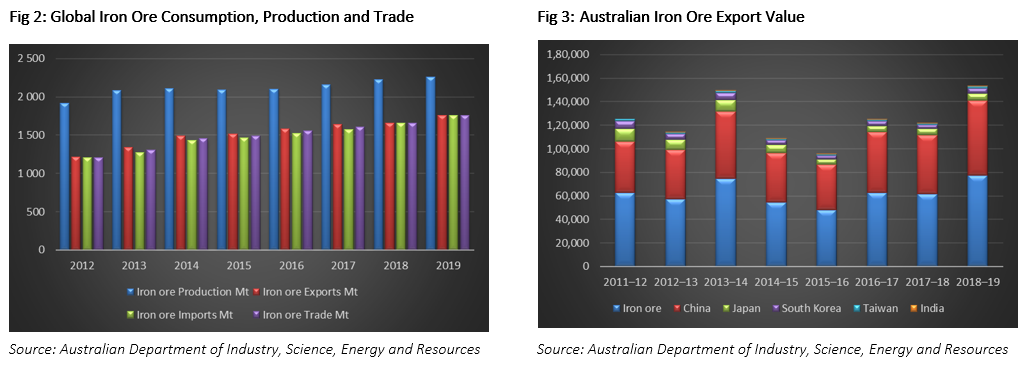

Historically China is seen participating in almost 70% of the global iron ore trade; however, the current coronavirus outbreak situation could pose a substantial risk to the iron ore prices, trade and access to seaports.

Iron ore follows the economic growth story and in future, the demand would be dependent on the trade negotiations between China and the United States.

The resumption of industrial activity in Chinese industries would further help improve the current demand and supply situations. The uncertainty over the recovery of the global economy raises some ambiguity over the Iron ore demand.

Further, iron ore supply is impacted by the weather disruptions in Australia and Brazil. With Brazil’s Vale already announcing the revision in the production guidance, the supply disruptions from the country’s largest Iron ore producer may impact the entire global iron ore industry, putting considerable upward pressure on the commodity prices. With China approaching its way to recover completely, the steel plants are expected to lead to a sudden increase in the iron ore demand in April and rest of the second quarter until the infrastructure demand comes online in full. Other major players such as India, Japan, South Korea and Europe have either suspended the operations at their steel plants or are operating at a reduced utilisation rate.

However, further disruptions among major producers, unforeseen delays in reinstating production, or additional Chinese stimulus measures could each put countervailing upward pressure on prices over 2020. Although China has emerged as the demand setter in the iron and steel markets, other important global players will help boost the demand while on recovery from the pandemic.

The global iron ore trade in 2019 stood at 1,760 million tonnes and is expected to increase further to 1,775 million in 2020.

Industry Majors back sharp Chinese revival: Industry majors including both RIO and BHP expect a strong rebound in the steel production in China. The metals majors anticipate that if China manages to avoid the second wave of coronavirus infections in the country, it may further boost up the steel output in 2020. The recovery is already underway as the utilization rates of the blast furnaces increased to 79% in April from 73%.

Rebar transactions have already reached the normal seasonal levels. The port outflows since March has also grown 10% higher than the previous year, leading to accelerated depletion of port stocks which is welcome by the Australian iron ore majors. Demand for the June quarter is expected to remain strong amid the low port stocks and supply disruptions.

Now, that we understand how the demand dynamics in the industry is anticipated, let’s look at the supply side scenario which includes both Australia and Brazil, the two top Iron Ore Exporters.

Australia gearing up for a stronger year amidst Coronavirus pandemic

With Brazil under stress due to operational, safety and weather constraints, Australia aims for higher iron ore export volumes to 892 million tonnes in 2020 from 836 million tonnes in 2019. The supply disruptions and the Chinese port stocks are expected to maintain strength in the commodity prices. The iron ore exports earnings for 2019-20 are expected to rise to a record level of $101 Billion due to strength in the prices and larger production volumes.

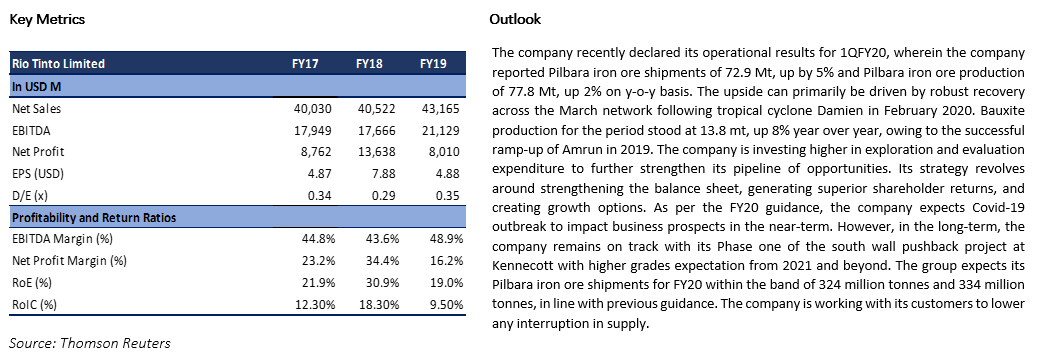

Major iron ore producers are committed to have more iron ore while battling the coronavirus pandemic and remain committed to safeguard the health and safety of their employees, contractors and communities. Rio Tinto, now the world’s largest iron ore producer, reported a steady growth of 5% (y-o-y) in the iron ore supply to 72.9 Million tonnes even after facing operational and supply chain issues during cyclone Damien in February 2020.

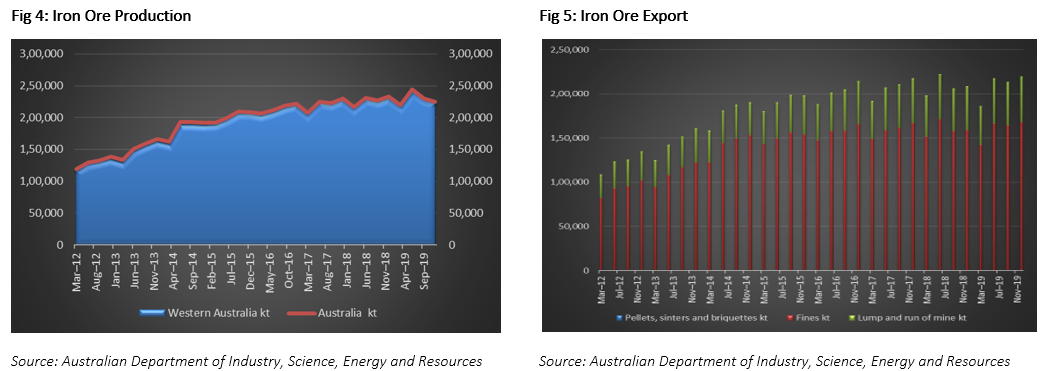

On recovery from the current pandemic, new outputs from the commencement of substantial projects can be anticipated in the Pilbara region of Western Australia. Though the major focus of the year would be to ramp up production from the existing operational mines, Pilbara, Australia’s richest iron region, may experience commencement of projects including BHP’s South Flank project, Fortescue’s Eliwana project and Brockman’s Maraillana operations by 2021.

Brazil struggles to maintain iron ore export volumes

Brazil, the world’s second largest exporter of iron ore, experienced major iron ore supply disruption following the heavy rainfall in the southern and eastern portions of the country leading to flooding of the iron ore mines. The flooding and heavy rainfall also resulted in a larger proportion of tailings dam under stress. ANM, the Brazilian National Mining Agency had announced in early April that a total of 47 mining dams lacks Stability Condition Declaration (DCE) and would suspend the operations at all such sites. Out of 47 mining dams, at least 25 were owned by the Vale, previous world’s largest iron ore producer.

In January 2019, the Brumadinho tailings dam collapsed at the Córrego do Feijão mine claiming over 270 lives, some of the victims were never actually found and were later assumed dead. Vale was recently replaced by the homegrown Rio Tinto as the largest iron ore producer in the world. Vale produced 59.6 Mt of Iron ore fines during Q1,2020, a 23% decrease in production in comparison to the previous quarter. The production volume was below the production guidance of 63-68 Mt due to unscheduled maintenance, operational issues at the south-eastern and northern system, delay of new Morro 1 mining section.

Vale recently revised the production outlook for iron ore fines for 2020 to 310-330 Mt from 340-355 Mt (initially) and 35-40 Mt for pellets from 44 Mt (initially). The revision was in line with the lower Q1 production, partly on the back of operational issues as well as additional impact due to pandemic. Large parts in the South and eastern Brazil faced heavy rainfall, leading to floods that had impacted Brazil’s output. On the country level, the supply from Brazil may face disruptions during 2020.

Having understood the demand and supply conditions, let’s have a look at how iron ore is faring on the price front.

How is Iron Ore Placed on the Price Front?

Iron ore prices in the recent times followed a volatile trajectory, the collapse of the Brumadinho tailings dam led to supply disruption from Brazil shooting up the iron ore prices to extravagant ranges. The resumption of the supply from Brazil to recovered volumes helped facilitate the iron ore prices to the normal ranges.

The prices did face transient but strong challenges such as cyclone Damien in the Pilbara region, which luckily was not as destructive as Veronica, but did cause some supply disruption in February this year. On Brazil’s end, the Latin American country faced larger supply issues due to the floods in the south and east of Brazil.

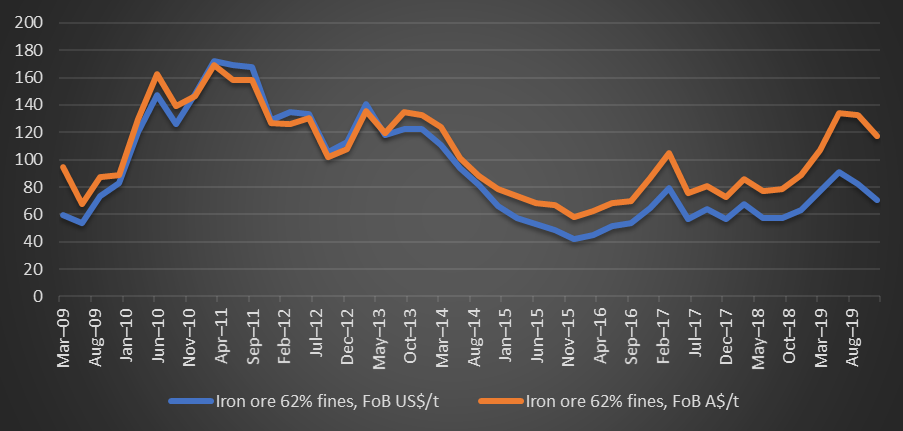

Fig 6: Iron Ore 62% Fines Price

Source: Australian Department of Industry, Science, Energy and Resources

Port stocks in the 5-year low ranges: As the iron ore inventories swirls in the five-year low ranges, even the smallest shift in the iron ore production is affecting the iron ore production largely. Australia, the largest iron ore producer in the world, sells most of its ore on the FOB Iron ore prices which peaked around $110 per tonne in July 2019, with the decline in iron ore prices to $75 a tonne by November and thereafter recovering to US$85 ranges in January and February 2020.

As per the Australian energy and resources quarterly March Edition, the iron ore prices are expected to average at US$81.9 a tonne of iron ore in 2020.

Chinese recovery may emerge as the sole demand setter in the current challenging times. The increasing port outflows and the utilization rates of the steel plants across China holding strong grounds for recovery following the coronavirus outbreak in China. Industry majors have indicated that the strong revival by the dragon would require an increased volume of iron ore feed, and with Brazil being plagued by operational and safety constraints, Australia could benefit from the opportunity.

II. Investment Theme and Stocks under Discussion (CIA, MGX, FMG and RIO)

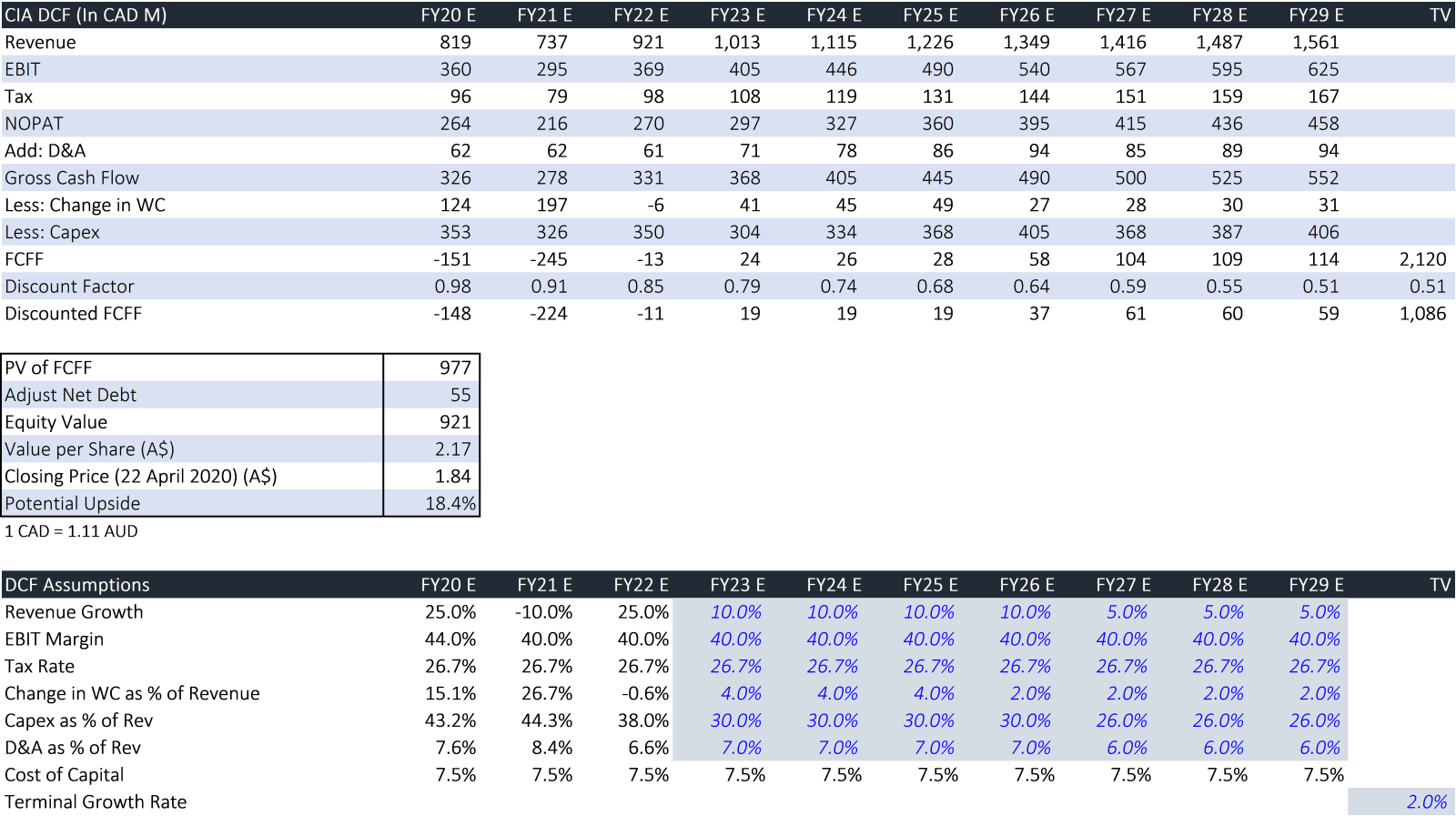

After gauging through the Iron ore market dynamics, let us take a detailed look at the companies operating in this sector, in terms of their performance and outlook. We have assessed the iron ore companies stocks based on Discounted Cash Flow (DCF) method.

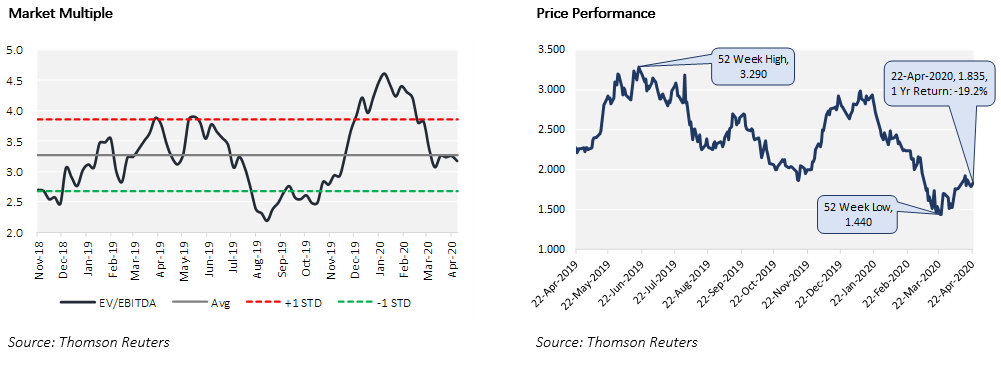

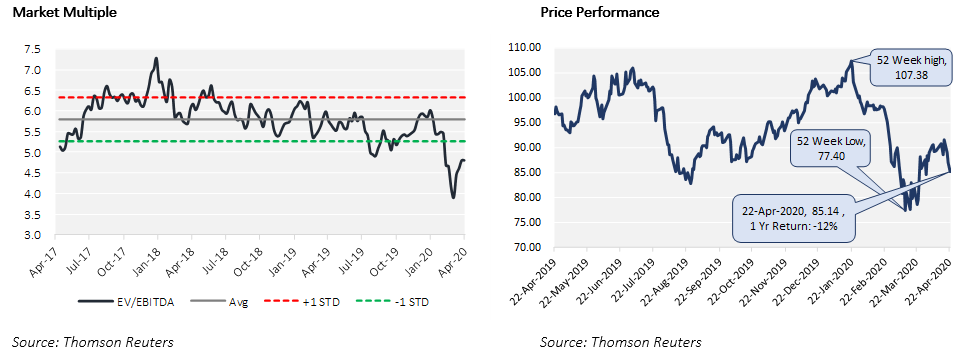

Fig 7: Relative performance of the stocks under discussion against ASX 200

.png)

Source: Thomson Reuters

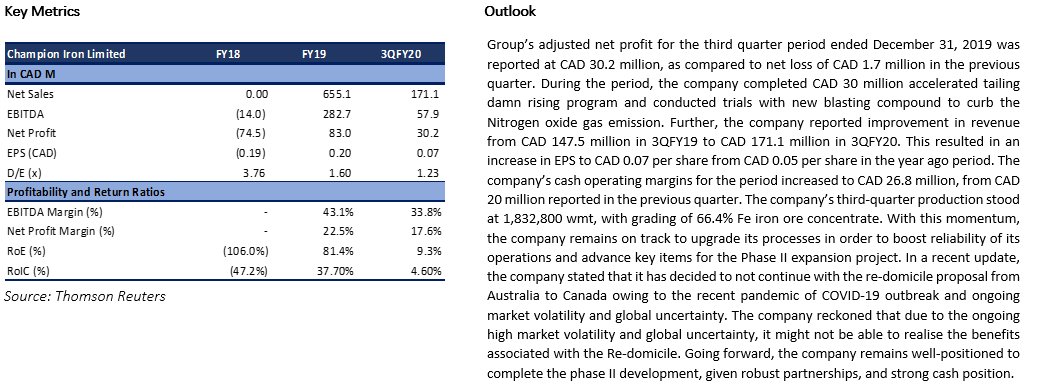

1. ASX: CIA (CHAMPION IRON LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 840.2 Million)

Champion Iron Limited is engaged in the exploration and development of iron-ore and mining projects.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~18% on 22 April 2020 closing price.

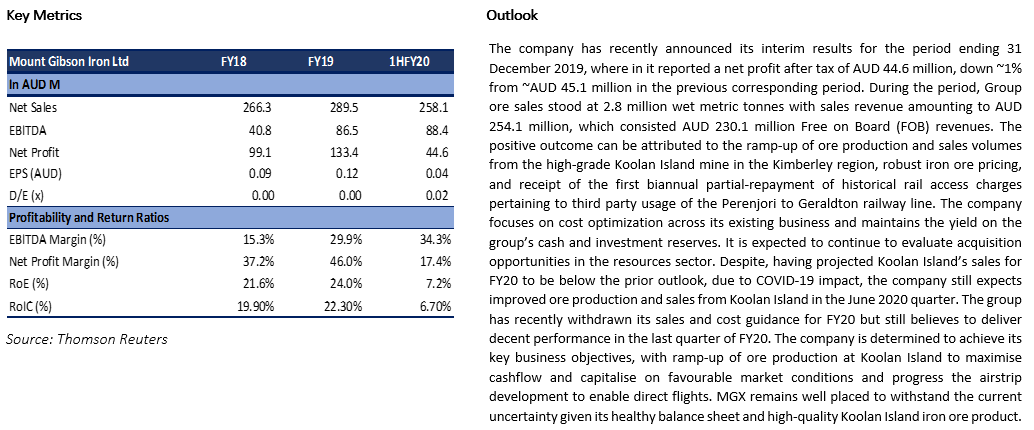

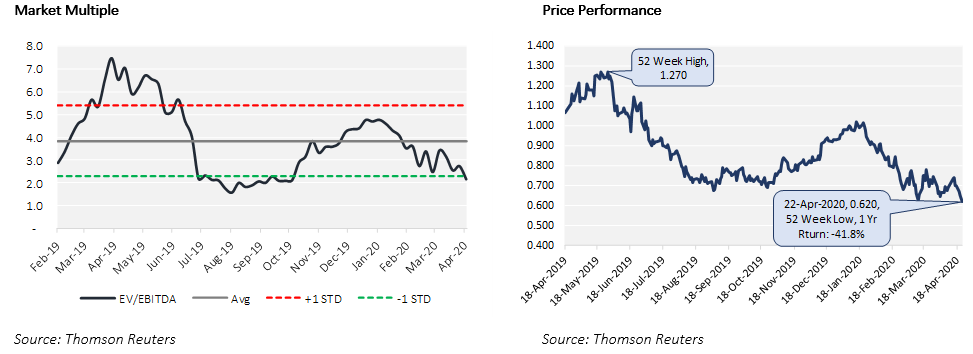

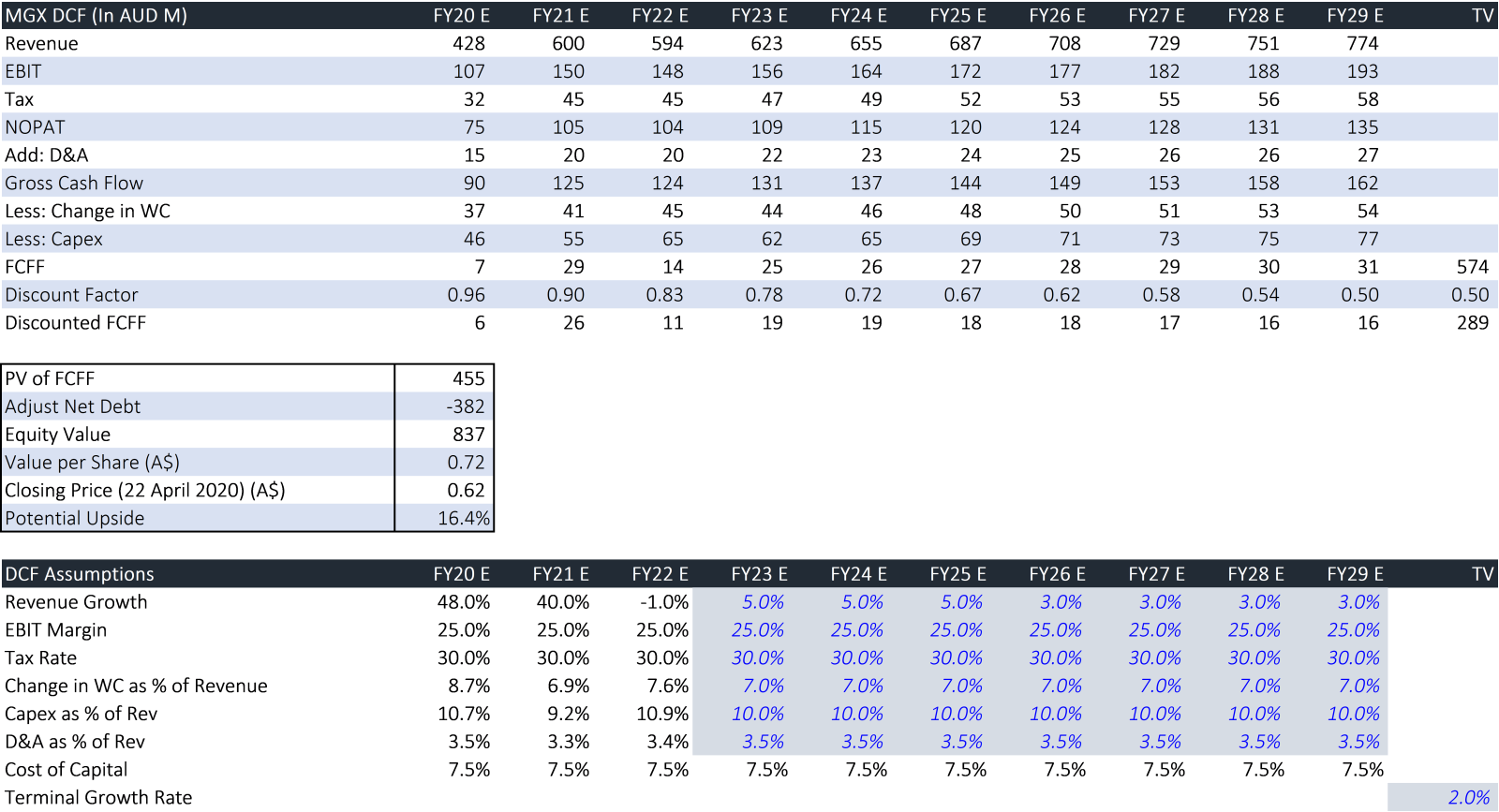

2. ASX: MGX (MOUNT GIBSON IRON LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: AUD 752.5 Million)

Mount Gibson Iron Ltd is engaged in mining, processing, and transportation of hematite iron ore.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~16% on 22 April 2020 closing price.

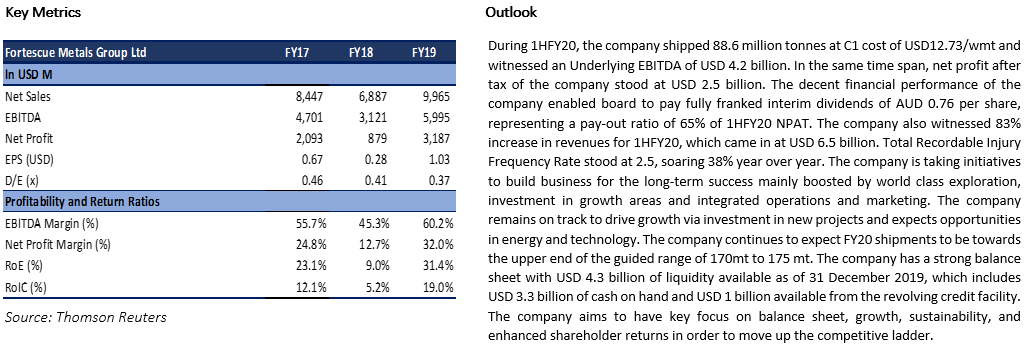

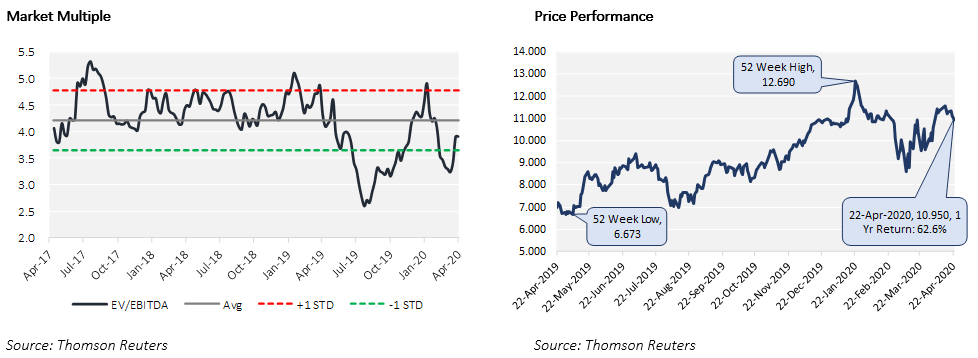

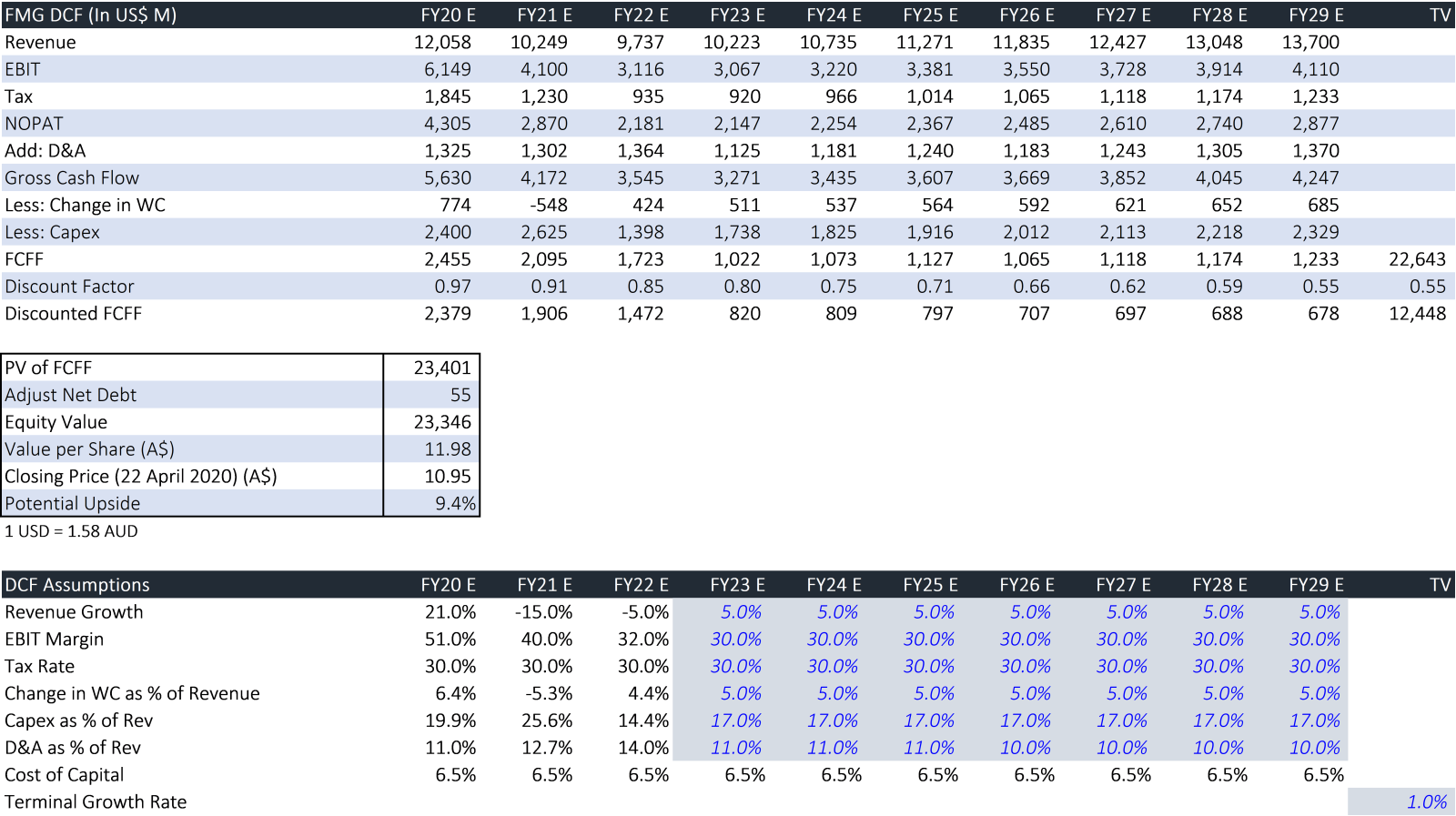

3. ASX: FMG (FORTESCUE METALS GROUP LIMITED)

(Recommendation: Hold, Potential Upside: High Single Digit, Mcap: AUD 34.2 Billion)

Fortescue Metals Group Ltd is involved in mining, processing, and transporting of iron ore for export from the company’s deposits within the Pilbara region.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~9% on 22 April 2020 closing price.

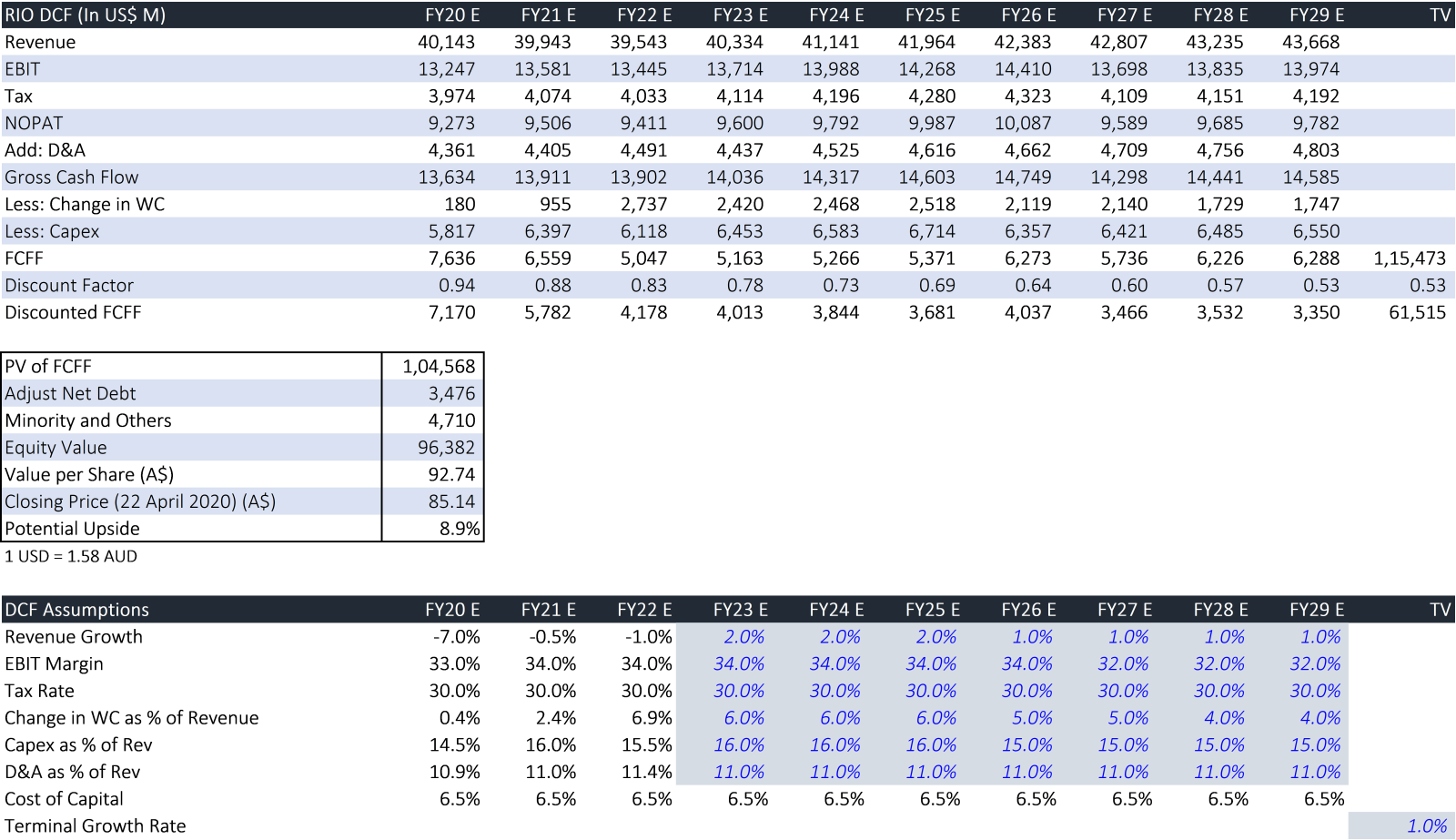

4. ASX: RIO (RIO TINTO LIMITED)

(Recommendation: Watch, Potential Upside: High Single Digit, Mcap: AUD 32.2 Billion)

Rio Tinto Limited is engaged in the production and manufacturing of copper, gold, iron ore, coal, aluminium, borates, titanium dioxide and other minerals.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~9% on 22 April 2020 closing price.

Note: All the recommendations and the calculations are based on the closing price of 22 April 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters. All the recommendations are valid on 23 April 2020 price as well.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

AU

AU

Please wait processing your request...

Please wait processing your request...