Kalkine has a fully transformed New Avatar.

Company Overview: IPH Limited (ASX: IPH) provides filing, prosecution, enforcement and management of patents, designs, trademarks and other IP in various countries like Australia, New Zealand, Asia, etc. and is engaged in the development and provision of IP data and analytics under the subscription licence model whereby the software is licensed and paid for on a recurring basis. The Group is organized into three segments, namely Intellectual Property Services, Australia & New Zealand; Intellectual Property Services, Asia; and Data and Analytics Software..png)

IPH Details.png)

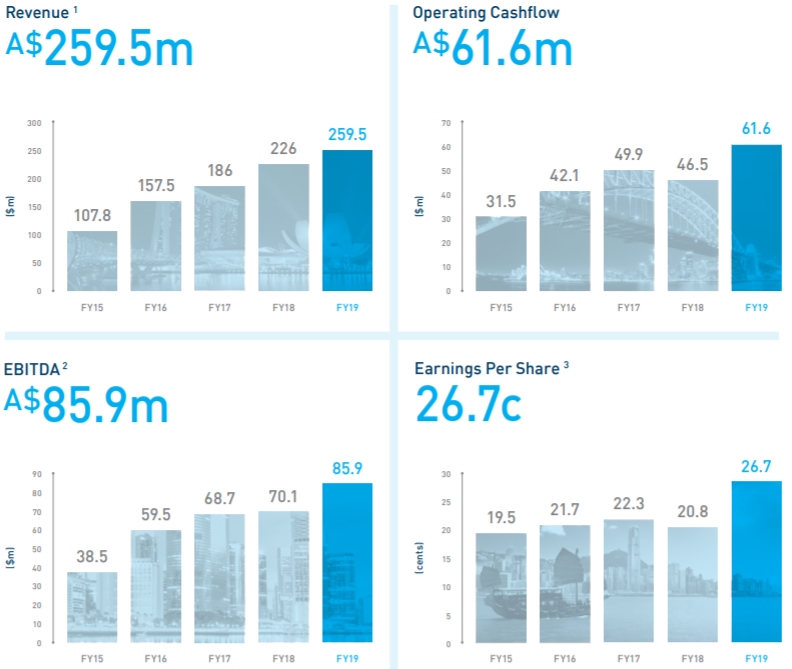

Continued Double-Digit Revenue and Earnings Growth: IPH Limited (ASX: IPH) provides filing, prosecution, enforcement and management of patents, designs, trademarks and other IP in various countries and is engaged in the development and provision of IP data and analytics under the subscription licence model whereby the software is licensed and paid for on a recurring basis. As on 23 March 2020, the market capitalization of the company stood at ~$1.46 billion. During FY19, the company delivered strong results with continued double-digit revenue and earnings growth in its Asian operations and improved margins in its Australian and New Zealand businesses. In FY19, the company reported an increase in revenue to $259.5 million, up from $226 million in FY18. In the same time span, the company delivered an underlying EBITDA of $89.7 million, reflecting an increase of 21% on the prior period. The main contributors to these results were four months of acquisitive growth from the AJ Park business in comparison to the prior year; changes in foreign currency rate; and organic growth from its existing businesses, particularly in Asia. This resulted in an increase in statutory NPAT by 31% to $53.1 million, equating to an increase of 29% in diluted earnings per share to 26.7 cents. As a result of the improved financial performance, the Board declared a partially franked final dividend of 13 cents per share, which bought the full-year dividend to 25 cents per share, up by 11% on the prior year. Over the span of 4 years, the company witnessed a CAGR (Compound Annual Growth Rate) of 29.91% in revenue, reflecting the evolution of the company and the strong platform it has created for future growth.

The company has recently declared its interim results for the period ended 31 December 2019 wherein it reported decent growth across all financial metrics. IPH Limited maintained a healthy market share in the growing market with excellent growth across Asian jurisdictions. It has a continued focus on potential overseas acquisitions in secondary IP markets and is aiming for development in the digital platform.

The company made substantial progress in implementing its growth strategy, supporting its future growth and continued to leverage its existing network to grow its Asian business. In FY19, IPH Limited had a continued focus on attracting, motivating and retaining key talent across the platform and made its largest acquisition of Xenith IP, which reinforced its leadership position in the Australian and New Zealand markets.

FY19 Financial Highlights (Source: Company Reports)

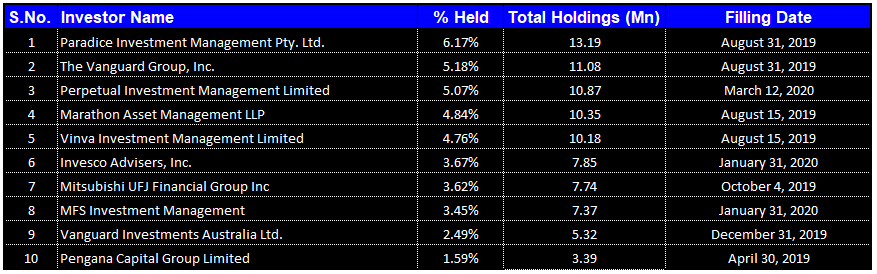

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of IPH Limited. Paradice Investment Management Pty. Ltd. is the largest shareholder in the company, with a percentage holding of 6.17%.

Top 10 Shareholders (Source: Thomson Reuters)

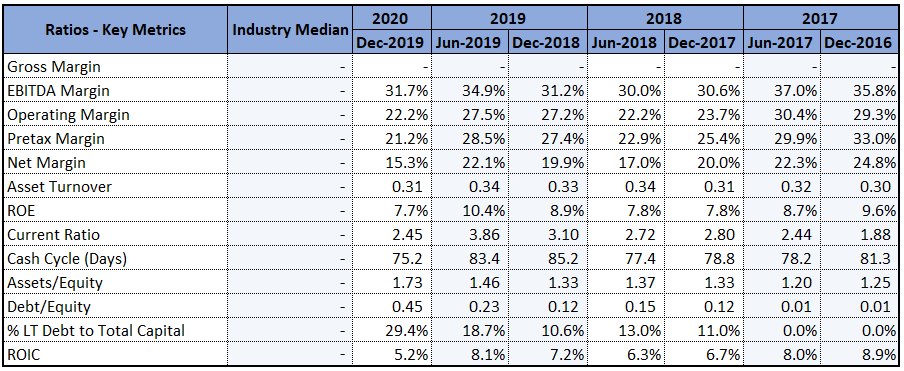

Cost Management and Decent Liquidity Levels: Over the span of 2 years, the company has witnessed a slight improvement in its EBITDA margin, which stood at 31.7%, up from 30.6% in 1H18. This indicates that the company is managing its costs well and is able to convert its revenue into profits. In the same time span, net margin of the company stood at 15.3%. During 1HFY20, Return on Equity of the company was 7.7%, in line with ROE of 1H18. In the same time span, current ratio of the company stood at 2.45x, up from 1.88x in 1H17. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. During 1HFY20, Assets/Equity ratio of the company was 1.73x with Debt/Equity ratio of 0.45x.

Key Margins (Source: Company Reports)

Successful Completion of Xenith IP Group: The company had acquired all the shares of Xenith and marked a significant milestone in continued implementation of its strategy to be the leading IP group in secondary IP markets and adjacent areas of IP. The expanded group is now operating across 27 offices in 8 countries, providing enhanced career pathways for people. The company also announced the integration of Watermark into its IP services business, Griffith Hack, to create one firm operating under the Griffith Hack brand from April 2020. It is anticipated that this integration will provide annualized net financial benefits between $2 million to $2.5 million from FY21.

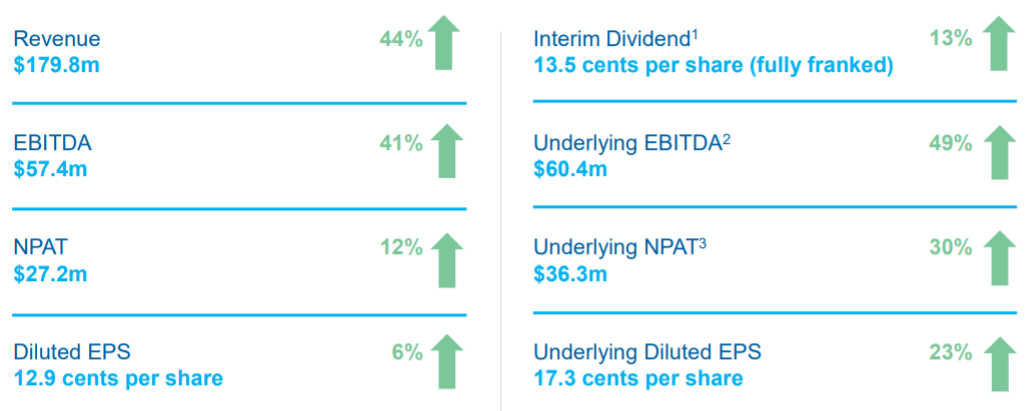

Growth Across Financial Metrics: The company has released its interim results for the period ended 31 December 2019 wherein it delivered an increase of 46% in underlying revenue to $179.3 million and reported a growth of 49% in underlying EBITDA to $60.4 million. This resulted in underlying NPAT to rise by 30% to $36.3 million. The result reflects ongoing improvement from IPH’s pre-existing business and a solid performance from the Xenith IP businesses, which were acquired by IPH effective 15 August 2019. The decent financial and operating performance enabled the Board to declare a fully franked interim dividend of 13.5 cents per share, up by 13% on the pcp. The increase in the number of cases transferred from new and existing clients continues to deliver margin accretion. The company’s filing activity increased across key Asian jurisdictions with total patent filing growth of 27.5% on the pcp.

During 1HFY20, the company continued strong cash conversion, reflecting the collection of receivables from the strong second half of FY19. IPH Limited also reported a robust balance sheet, reflecting the acquisition of Xenith IP and the adoption of AASB16.

Growth Across Financial Metrics (Source: Company Reports)

Future Expectations and Growth Opportunities: The company has a continued focus on implementing its growth strategy and is prioritizing growth in sales of WiseTime. It is also focusing on maintaining a leading market position in Australia and New Zealand and is aiming for continued expansion in margins. IPH has a continued focus on Asia to develop the network effect and is also concentrating on potential overseas acquisitions in secondary IP markets. The company has seen an enhanced performance from the Xenith businesses compared to the pcp and expects to see further earnings accretion over time. IPH Limited is on target to attain synergies of ~$3.4 million in FY20 from Xenith IP.

The company is also monitoring the impact of the outbreak of novel coronavirus in various countries and stated that there might be some disruption to the business, but it doesn’t anticipate any significant loss of revenue. IPH also expects to generate further efficiencies from the integration of Watermark into Griffith Hack. The company is continuing to create a more robust and diverse platform to deliver growth in revenue and earnings and increased returns for shareholders.

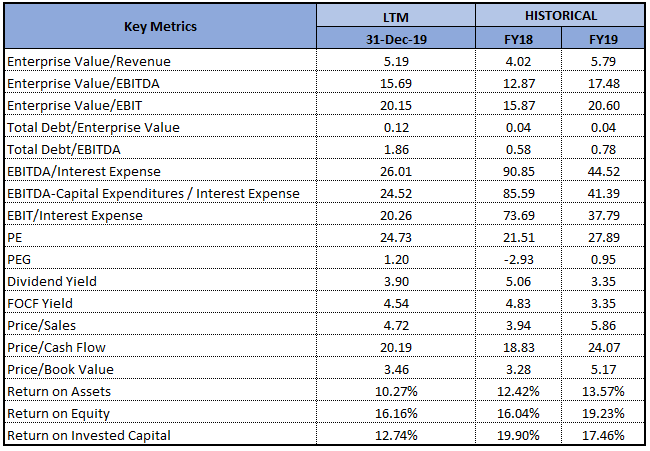

Key Valuation Metrics (Source: Thomson Reuters)

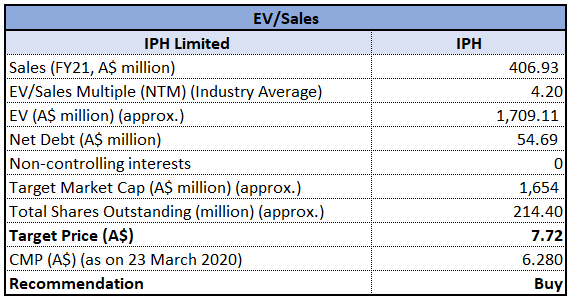

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Approach

EV/Sales Multiple Based Relative Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.

Stock Recommendation: As per ASX, the stock of IPH is trading very close to its 52-weeks’ low level of $6.010, proffering a decent opportunity for accumulation. The company has delivered total shareholder return of 370% over the past five years, which includes the increase in share price and dividends paid to shareholders. During FY19, the company achieved double-digit growth across its key financial metrics and reported strong performance in the first half of FY20. IPH continued to leverage its existing network to grow the Asian business and add further value to the group. Considering the trading levels, high shareholder returns, decent financial performance and long-term outlook, we have valued the stock using EV/Sales multiple based relative valuation approach and have arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $6.280, down by 7.647% on 23rd March 2020..png)

IPH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...