Kalkine has a fully transformed New Avatar.

Company Overview: IPH Limited is a holding company. The Company offers a range of intellectual property (IP) services and products to a client base of Fortune Global 500 companies, multinationals, public sector research organizations, small and medium-sized enterprises (SMEs) and professional services firms around the world. The Company operates through the segments, including Intellectual Property Services Australia, Intellectual Property Services Asia, and Data and Analytics Software. The Company's Intellectual Property Services Australia segment is engaged in providing filing, prosecution, enforcement and management of patents, designs, trademarks and other IP in Australia. The Company's Intellectual Property Services Asia segment is engaged in providing filing, prosecution, enforcement and management of patents, designs, trademarks and other IP in Asia. The Company's Data and Analytics Software segment develops and provides IP data and analytics software under a subscription license model.

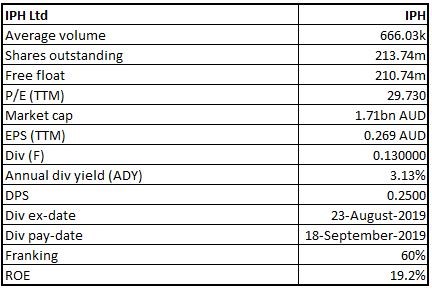

IPH Details

Decent Performance in FY19: IPH Limited (ASX: IPH) is the leading intellectual property professional services group in the Asia-Pacific region. The company offers a wide range of IP services and products to a client base of Fortune Global 500 companies, multinationals, public sector research organizations, small and medium-sized enterprises (SMEs) and professional services firms around the world. As on November 11, 2019, the market capitalisation of the company stood at ~A$1.71 billion. The company reported a decent set of numbers for the period ended June 30, 2019 (FY19), wherein revenue increased by ~15% to $259.5 million as compared to the prior year. It was mainly supported by organic and acquisitive growth during the same period. Statutory net profit after tax for the period increased by 31% on YoY to $53.1 Mn. Resultantly, EPS grew by 29% to 26.7 cents per share in FY19. The company has also demonstrated the ability to leverage its extensive network across Asia, implement its strategy to integrate domestic acquisitions, and further strengthen Australia and New Zealand operations.

Since 2014, the company has completed 8 acquisitions in Australia, New Zealand and Asia and made progress with respect to its vision. It has more than doubled its footprint in Asia-Pacific. As a publicly listed IP services group, the company accesses the capital needed to invest in the group businesses and ensure that they have the capabilities, resources and systems to deliver highest quality services to their clients, provide expanded career opportunities, and continue to evolve in order to meet needs of clients in a rapidly changing IP services market.

Based on the performance in FY19, the Board of Directors declared a final dividend of 13 cents per share, franked to 60%. This summarized a total dividend payment of 25.0 cps for full-year, which represents an increase in the full year dividends of 11%. During FY19, the company has wrapped up the strategic agreement to acquire Xenith IP Group. This strategic acquisition will support IPH’s leadership position in the Australian and New Zealand markets and provides an exceptional opportunity to harness the network across the Asia-Pacific region.

Looking at the past performance of the company, revenue over the period FY15-FY19 posted a decent CAGR growth of 24.6% from $107.8 million to $259.5 million from FY15 to FY19. EBITDA of the company witnessed a rise from $38.5 million in FY15 to $85.9 million in FY19, with a CAGR growth of 22.2% over FY15 – FY19, representing that the business generated decent earnings over the said period. NPAT increased from $30.6 million to $53.1 during the time span of 2015-19, reporting a CAGR of 14.8%. In our view, the company has a lot of potential to grow further at the back of (1) strategic acquisition with Xenith IP Group, (2) maintaining its market-leading position in Australia/New Zealand market, (3) continued to focus on Asia to develop the network effect, (4) WiseTime growth in sales, and (5) continued focus on potential overseas acquisition in secondary IP market.

.png)

Five-Year Financial Performance (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in IPH Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Improvement in Key Margins: The company’s net margin in FY19 stood at 21%, which is higher from FY18 figure of 18.3% and, therefore, it can be said that IPH has decent capabilities to convert its top-line into the bottom-line. In FY19, IPH’s EBITDA margin stood at 33.1% as compared to FY18 figure of 31.2%. The company’s RoE stood at 19.2% as compared to 16% in FY18 and, thus, it looks like IPH has delivered improved returns to its shareholders in FY19. The company’s current ratio stood at 3.86x in FY19, which is higher than FY18 figure of 2.72x and, thus, it can be said that IPH is in a better position to meet its short-term obligations. Additionally, decent liquidity levels might help it in making deployments towards strategic objectives, which can help it in achieving overall growth in the long-term. There are expectations that improvement in RoE might help the company in getting traction among the market participants.

.png)

Key Metrics (Source: Thomson Reuters)

Significant Opportunity in China: IPH Limited recently presented its business prospects at the Morgans Queensland Conference and highlighted about FY19 activity and opportunity in China. As per the presentation, the company has a significant opportunity in China. With respect to the China IP landscape, it was mentioned that, in 1H FY19, the number of foreign invention patent applications in China reached 78,000, which implies a rise of 8.6%, and the number of foreign trade mark applications in China stood at 127,000, up 15.4%. IPH is well-placed to seize the opportunities in China, which might help it in achieving overall growth.

Announcement About Sale of Shares: IPH Limited has recently advised that MD and CEO named Dr Andrew Blattman, has sold 300,000 shares in IPH for the personal reasons, that includes satisfying the personal tax obligations. Post-sale, Dr Blattman possesses a significant relevant interest in IPH and remains one of the largest private individual shareholders. He has a holding of 2,206,166 shares (representing around 1.03% of the issued capital) and 355,456 performance rights that are subject to the meeting of specific vesting conditions.

Overview of Market Conditions: In FY19, IPH has maintained leading market share positions in ANZ and Singapore. In Singapore, the patent filings of IPH group for a calendar year to June 30, 2019, were in line with market growth of 4.7% and continue to maintain No. 1 patent market share of 24% for the calendar year ended June 30, 2019. The filing activity of IPH group increased throughout most of the Asian jurisdictions, primarily in Thailand, Indonesia, Malaysia, The Philippines and Vietnam. It was further added that total patent filing growth throughout key Asian jurisdictions, excluding Singapore, stood at 22.7% for the year.

The overall trade mark market in Australia witnessed a fall of 8.2% for the year and IPH trade mark filings also witnessed a fall, which happens to be consistent with the overall market. However, IPH group has been holding the number one trade mark market position in Australia, and it has a 14.2% share of filings from the top 50 agents.

Growth Via Acquisition: The company started the process of acquiring Xenith IP Group during FY19, which represents the largest acquisition in the history of IPH. After successful scheme implementation on August 15, 2019, combined group have a broadened Australian business and can utilise IPH’s significant experience and geographic reach in Asia region with combined business operating 8 leading IP services firms and IP adjacent businesses, having over 1000 staff throughout 27 offices in 8 jurisdictions in the Asia-Pacific.

What to Expect from IPH Moving Forward: The strategic priorities of IPH consist of maintaining the leading positions in ANZ and Singapore, as well as seeking to expand in other jurisdictions having higher growth. The company has started its work to identify and leverage the cost synergies and revenue opportunities arising as a result of Xenith transaction to deliver further improvement in margin throughout the combined business over the span of the next 3 years. IPH expects to give an update on the activities at AGM, which is expected to take place on November 21, 2019.

IPH would continue to leverage the Asian network in order to expand the organic revenue opportunities and the market share in high growth markets throughout the region. In ANZ, the group’s strategy includes continuing to focus on the expansion of service provision with the existing foreign associate firms, as well as attracting new corporate clients.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

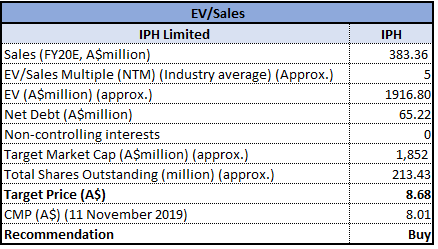

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The stock price of IPH has witnessed an increase of 14.61% in the time span of the previous six months and, on a YTD basis, the stock has increased by 47.60%. The company plans to increase the market share and sales in WiseTime product and prudent investment on digital platform development. Also, it has been evaluating potential international acquisition opportunities in the core secondary IP markets. Talking about the financial performance, the revenue rose 15%, and the figure stood at $259.5 million because of the impact of organic growth, acquisitions, sale of Practice Insight businesses as well as an impact of the weaker AUD as compared to the previous year. Notably, the statutory EBITDA rose 23%, and the figure was $85.9 million. In the time span of FY 2015- FY19, the company has witnessed a CAGR growth of 24.6% in total revenues and, thus, it can be said that it is possessing respectable capabilities to generate revenues. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple, and arrived at a target price of high single-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$8.010 per share (up 0.125% on 11 November 2019).

IPH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...