Company Overview - IOOF Holdings Ltd is an Australia-based financial services company. The Company provides a range of products, which include financial advice, platform management and administration, investment management and trustee services. Its investment products include IOOF WealthBuilder, which minimizes the tax pay on savings; IOOF Pursuit Select Investment Service, which offers investment management and administration services; The Portfolio Service, which is a product it has designed to meet the needs of its financial advisers. Its Australian Executor Trustees (AET’s) Portfolio Management Service (PMS) provides the advisers with administration, reporting and record-keeping facilities. Its investment funds include IOOF MultiMix Trusts, which provide access to a team of investment professionals who identify, blend and monitor investment managers; Perennial, which offers investment products across a range of asset classes, and Resolution Capital, which manages real estate securities.

Analysis - The financial services provider was recently in the news when Fairfax Media made several revelations about instances of serious misconduct by the company. Some of these revelations relate to fraud, forgery, cover-ups by management, front-running by employees and insider trading in addition to a number of other serious charges. The articles seem to suggest that the company was overly focused on the bottom line to the detriment of its customers and clients and with little regard to the rules and regulations.

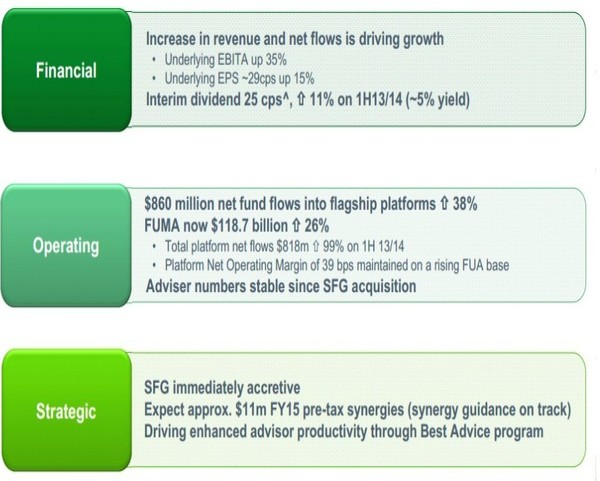

Interim Highlights (Source - Company Reports)

The company responded with a statement that it was taking seriously any suggestions that its high standards are not being followed by its various businesses and noted its strong record of compliance.

Interim Highlights (Source - Company Reports)

The company responded with a statement that it was taking seriously any suggestions that its high standards are not being followed by its various businesses and noted its strong record of compliance. It said that it would at all times act in the best interests of customers and clients and that, to the best of its knowledge, none of the issues raised in the articles will cause any loss to any of them, past or present. It believes that many of these claims have been promoted by a former employee who is in a legal dispute with the company and they are historic in nature.

All the issues raised, historic or recent, have been dealt with as appropriate and the result has been the enhancement of processes and procedures which have sought to improve the customer experience.

Platform Flows (Source - Company Reports)

Platform Flows (Source - Company Reports)

The company says that there are a number of misleading statements that needs to be addressed. One article regarding the Risk Register and systems and services gives the impression that the company does not regard its products and services as being competitive in the market.

This statement was extracted from an internal document maintained for the purpose of effectively managing risk and reporting to the Board Risk and Compliance committee. The registers are provided regularly to the APRA and the key controls and action plans are clear from the document, the company regards the statement is misleading. Another statement regarding a Platinum unit pricing error relates to an external manager Platinum Asset Manager and was not an internal company error. It is the case that the company identified a Questor Cash Management unit pricing error which was reported to the ASIC in January 2013. A remediation plan was recently resolved and the compensation, independently verified, is close to $ 3 million of which only a part may be funded by the company and the amount is considered immaterial. The company concludes by saying that some of the claims relate to legal matters and cannot be publicly discussed at this time and cannot therefore be commented on.

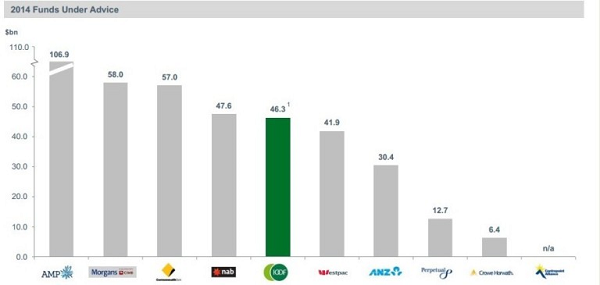

Funds Under Advice (Source - Company Reports)

In accordance with its stated approach, the company has engaged PwC to immediately commence an independent review of the group regulatory breach reporting policy and procedures and the control environment within its Research division.

Funds Under Advice (Source - Company Reports)

In accordance with its stated approach, the company has engaged PwC to immediately commence an independent review of the group regulatory breach reporting policy and procedures and the control environment within its Research division. This will be a thorough review and the outcome will be reported to ASIC and APRA. Despite the company believing that the issues are historic and have been addressed where relevant, the company has decided to appoint PwC so that clients and other stakeholders are fully convinced of the integrity of the company's controls in the Research division and the group regulatory breach reporting systems. The company will also keep the market fully informed of any outcomes from the review process.

Financial Highlights (Source - Company Reports)

Interim results 31 December 2014

Financial Highlights (Source - Company Reports)

Interim results 31 December 2014

The company believes in a strategy that will create value. The strategy includes organic growth and the net fund flow to the flagship platform was $ 860 million during this half year compared to $ 622 millioiIn the same period of the previous year. Productivity has been enhanced by advisers led activity and cost management continues to be a notable feature. The policy of accretive acquisitions means that the acquisition of SFG Australia will be immediately accretive and $ 3.5 million in pre-tax synergies have been realised. The focus on shareholder value continues and is evidenced by the TSR for the 12 months to 23 February 2015 and the fully franked interim dividend of $ .25 per share which represents a dividend yield of approximately 5%. The UNPAT of $ 80.6 million represents a growth of 39%.

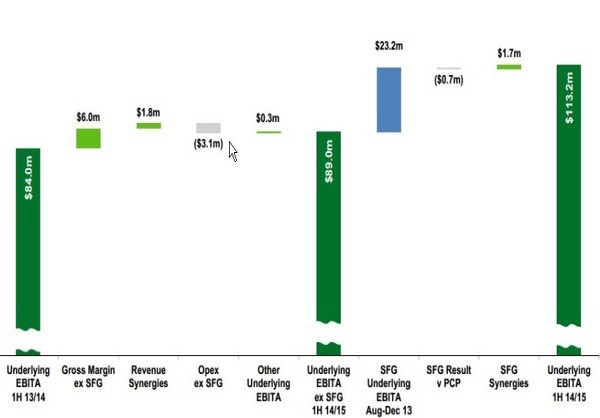

EBITA (Source -Company Reports)

EBITA (Source -Company Reports)

Financial growth is being driven by increases in revenues and net flows and the underlying EBITA at $ 113.2 million was up by 35% while the statutory statutory NPAT is up 37% to $ 66 million and the underlying NPAT by 39% to $ 80.6 million. Gross margin is up 38% to $ 267.9 million and underlying EPS is 15% to 28.7 cents per share.

The company concentrates on business that is advice driven and focused on scale. In financial advice and distribution, UNPAT was up 22% at $ 11.1 million. The average FUA was up 7% by $ 2.1 billion to $ 33.2 billion and the business benefited from the increased scale. SFG reported an increase of 8% to UNPAT of $ 17.2 million in the five months post acquisition. FUMA was 5% up over the previous year by $ 0.8 billion to $ 19.6 billion and the new acquisition was immediately accretive. Platinum management and administration reported growth in UNPAT of 9% to $ 43 million reflecting the strong performance in a corb business. Average FUA grew by 10% or $ 2.9 billion to $ 32.8 billion. Investment management reported a growth in UNPAT of 8% to $ 17.3 million and average FUM grew by 3% or $ 0.9 million to $ 31.5 billion. The restructuring to the core strengths of Perennial will result in benefits which will show up in 2015. Finally, trustee services reported a 12% growth in UNPAT to $ 3.2 million and the average FUS declined by 18% to $ 25.7 billion reflecting conditions returning to normal after a strong previous year. Organic growth continued its momentum and closing FUMA was up 26% to $ 118.7 billion ($ 94.08 billion in the previous year) which the average figure up 22% to $ 111.5 billion compared to $ 91.64 billion in the previous year. Total platform net flows of $ 818 million which was 99% up on the first of of the previous year was all organic and funds under administration of $ 33.6 billion were up $ 1.7 billion since June 2014. This makes eight consecutive quarters of of total positive platform net flows.

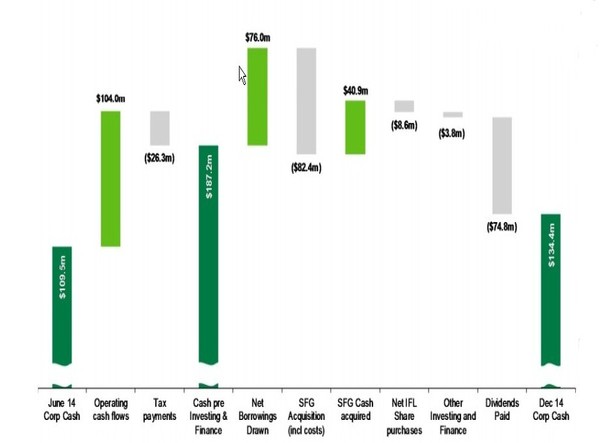

Strong Cash Flows (Source - Company Reports)

Strong Cash Flows (Source - Company Reports)

In respect of the SFG integration, side by side with the process, strong operating results were reported with stable advisor numbers. Head office rationalisation is continuing along with the unification and renegotiation of agreements with major suppliers. In the first half of 2015, realised pre-tax synergies total $ 3.5 million. The future agenda includes leveraging the Best Advice program, maximising opportunities from the position of being the fifth largest distributor in Australia,and consolidating the property footprint. By FY 2016, the company is confident of achieving pre-tax recurring annual synergies of $ 20 million.

Segment Performance (Source - Company Reports)

Segment Performance (Source - Company Reports)

The debt position and the ratios show an 88% increase in gross borrowing to $ 208.3 million and a net debt of $ 73.9 million compared to $ 1.6 million in the previous year. Debt to equity is up 1.2% from 12.1% to 13.3% and net debt to underlying EBITDA is up 0.1 times from 0.2 to 0.3. The return on equity is down 1% from 13.8% to 12.8%. The increase in borrowing was due to the funding of the SFG acquisition and the impact on the return on equity will improve because of growth and the realisation of additional synergies. The company continues to have a surplus borrowing facility with plenty of headroom in the covenants and the continued strength provides security and the ability to cash in on new opportunities.

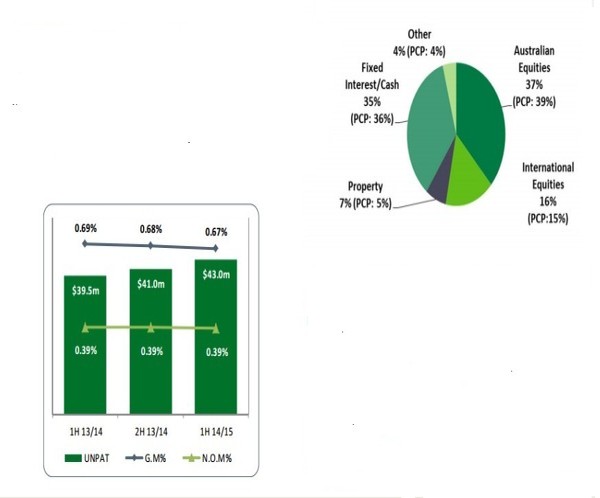

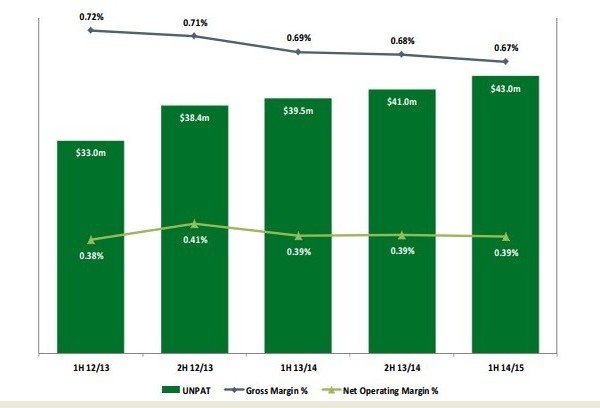

Net Operating Margin (Source - Company Reports)

Outlook

Net Operating Margin (Source - Company Reports)

Outlook

The company will continue to rely on service as a differentiator by providing service in the top quartile with relevant functionality and ease of use and believes that price is going to become less relevant. Customer experience will continue to be a critical factor with reducing importance for price and product differentiation and a defined focus will result in quicker and more comprehensive responses to the needs of customers. The successful integration of SFG which is well on track will continue to remain a major priority. Disciplined strategy execution and focus on productivity and infrastructure will facilitate organic growth. The outlook for regulatory intervention remains stable and the company is in a strong financial position to fund future acquisitions and other growth initiatives.

IFL Daily Chart (Source - Company Reports)

IFL Daily Chart (Source - Company Reports)

The immediate outcome of the Fairfax revelations was a sharp drop in the price as investors rushed to sell first and ask questions later. We believe that this drop has created a window of opportunity for investors to buy the stock. We are of the opinion that the company will navigate the crisis successfully and, at worst, may have to pay a few million dollars in compensation which it can easily afford. The stock looks cheap at the current price and we would rate it as a Buy at the current price of $8.96.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...