Kalkine has a fully transformed New Avatar.

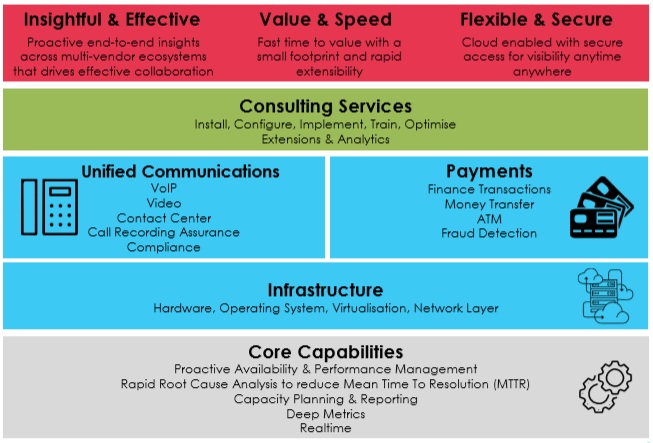

Company Overview: Integrated Research Limited is a provider of performance monitoring, diagnostics and management software solutions for business-critical computing environments. The Company's principal activities are the design, development, implementation and sale of systems and applications management computer software for business-critical computing, unified communication (UC) network and payment networks. Its geographical segments include the Americas, which operates from the United States with responsibility for the countries in North, Central and South America; Europe, which operates from the United Kingdom with responsibility for the countries in Europe; Asia Pacific, which operates from the Australia and Singapore with responsibility for the countries in the rest of the world, and Corporate Australia. It is focused on three markets: Infrastructure, which includes users of computing systems; Communications, which includes users of Internet Protocol telephony and UC applications, and Payments.

.png)

IRI Details

Unique Business Model: Integrated Research Limited (ASX: IRI) is a small- cap software and services company with the market capitalisation of circa $431.37 Mn as of 17 May 2019. It is a leading global provider of user experience and performance management solutions for Unified Communications, Payments and IT Infrastructure. The company has a proven sound business model, offering a lasting value proposition to customers who face complex problems. The income sources of the company are diversified, providing a range of products serving distinct markets, a strong innovation program, and world?class customers and partners. The group generates revenue from four main business verticals i.e., Unified Communications, Infrastructure, Payments, and Consulting which contributed around 53.6%, 21.9%, 17.9%, and 6.5%, revenue in total revenue respectively, in 1HFY19. It has key technological partnerships i.e., Cisco, Avaya and enjoys several competitive business advantages with exchange rate risks. Currently, the Company’s growth strategy focuses on the following key elements i.e., building capabilities, product developments, expanding the customer base, and regional diversification. In our view, the group is well positioned to expand its product services in a number of large corporations across the globe. Further, the group expects profit growth for FY19 in underlying operational performance, but reported financial performance will be influenced by foreign currency exchange fluctuation. Hence, we trust management's capabilities to maintain growth momentum in years to come.

.png)

Half Year Financial Metrics Trend (Source: Company Reports)

Strong Clientele Base: The company has a strong client base servicing a range of medium, large and blue-chip companies across the sectors such as Telecom/IT, Financial, Healthcare, and Non-Profit Organizations, etc. throughout the globe. The customers of IRI includes 125+ of the Fortune 500 companies. Nine out of top ten US banks are among its customer base including seven of the world’s top ten telecommunications companies and six of the top ten automotive groups globally.

Strong Customer Base (Source: Company Reports)

Key Technology Partners: The company had made a long?term partnership with Cisco, which is a global leader in UC solutions, by being selected to join its SolutionsPlus program. IRI signed a global resale arrangement with Avaya in July 2018 and is the only company to support every major Unified Communications (UC) vendor.

IRI’s Partners (Source: Company Reports)

Competitive Advantage & Key Risks: During FY18, Integrated Research made changes that will drive further growth in its largest solution area, Prognosis for Unified Communications. Prognosis provides best in class performance management across Unified Communications, Contact Centres and Payments ecosystems, cloud, hybrid or on-premises. The company enjoys a competitive advantage with Prognosis being real-time, scalable, extensible & flexible, supporting multiple platforms, vendors and applications. Further, the diversified customer base of the company with 1,200+ enterprise customers globally, along with 125+ of the Fortune 500 customers is a real strength for the business. Quality customer base is a testament to the superiority of IR’s solutions. It has a world-class R&D capability as well.

However, the consolidated entity’s activities expose it primarily to the financial risks of changes in foreign currency exchange rates and cash flow interest rate risks. It uses derivative financial instruments to hedge its exposure to foreign exchange risks arising from operational activities. The forward exchange contracts of the company have maturities of less than two years after the year end date. However, the credit risk on liquid funds and derivative financial instruments is limited because the counterparties of the company are banks with high credit ratings assigned by international credit?rating agencies.

Global Footprints (Source: Company Reports)

Operational Highlights: The company delivered on strategies to build capability, product development and expand global customer base. The payments' growth was up by 144%, driven by strong licence growth through renewal and capacity expansion. The Europe growth was up by 14.0%, on the back of re-organised approach and successful large deal closure. The company generated new revenue from SaaS development as well.

The value proposition for Integrated Research is underpinned by the Prognosis, providing end to end Unified Communications, having Payments and Infrastructure experience management and testing services which optimizes operations of critical systems through insight into real time and historical events. Moreover, it has intelligent analytics to establish patterns and root causes speeding troubleshooting and problem resolution. Evolving prediction capabilities, automation and self-healing help Prognosis optimize operations and prevent issues occurring at all.

\

\

Prognosis Solution Components (Source: Company Reports)

Key Performance Metrics: The company exhibited robust key performance metrics during 1HFY19 with 87% of the revenue remained recurring. Twenty new customers were added in the first half to the base - exhibiting strong customer foothold. The opening pipeline was higher than the prior corresponding period and the company continued a strong annual maintenance retention rate of 95%.

Along with maintaining high quality revenues and retention, the company was able to establish significant deals during 1HFY19 which included Barclaycard, CenturyLink and Conduent. It made contracts with multiyear duration and the top ten customers accounting for one-third of the total revenue.

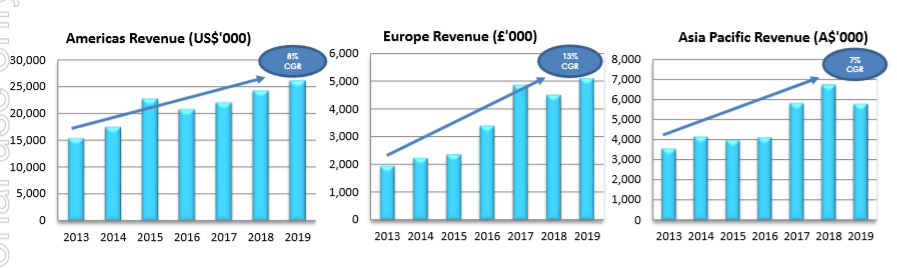

Revenue Trend- Geography wise (Source: Company Reports)

The company maintained consistent growth in revenues from the Americas with CGR growth of 8.0% from 2013 to 2019. Moreover, growth in revenue from Europe segment was returned on the back of strong Payments, exhibiting 13.0% CGR growth over the period of 2013 to 2019.

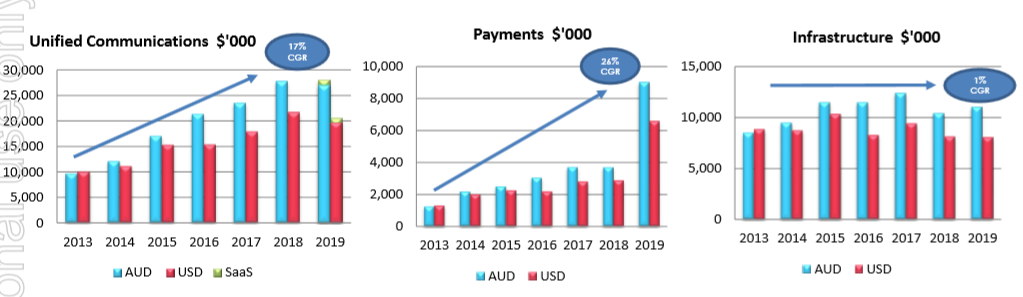

Revenue Analysis- Product Wise (Source: Company Reports)

On the product-wise revenue analysis front, the Cisco growth was offset by a decline in Avaya, with more than $1 million in SaaS bookings for future growth. The Unified Communications exhibited CGR growth of 17.0% over the period of 2013 to 2019. The company attained 26.0% CGR growth on the Payments platform from 2013 to 2019, driven by strong global contribution, strong relationship with ACI and multiyear account renewals and extensions. The infrastructure segment, however, witnessed a marginal CGR growth of 1.0% during 2013-2019 with consistent revenues, high margin product line and a sticky customer base.

Key Financial Highlights: The company exhibited a record first half performance in FY2019 with the profit after tax increasing by 26% to $11.7 million in 1HFY19 as compared to the prior corresponding period. The strong growth in net profit was primarily on the back of revenue generated from license fees which increased by 22% to $31.3 million and thus, total revenue increased by 10% to $50.3 million in 1HFY19.

The company achieved an improvement in profit margins for the first half of FY2019. The EBITDA margin was 41.3% compared to the equivalent prior period of 40%. The NPAT margin at 23.3% also improved as compared to~ 20% for the previous corresponding period. New licence sales would have increased by 17%, revenue by 5%, and profit after tax by 15% when growth was adjusted to constant currency in 1H FY19.

.png)

Key Ratios (Source: Thomson Reuters)

The cashflow from operations increased by 19% to $9.6 million during 1HFY19 on the back of increase in cash receipts from customers. The cashflow supports the on-going investment into research and development of the company with the gross spending on research & development activities, representing 18% of the revenue leading to a higher operating cost for the first half of FY19.

The company maintains a strong financial position and remains at debt-free level with a total cash position of $9.6 million at 31 December 2018, unchanged from 31 December 2017. The company declared a fully franked interim dividend of 3.5 cents per share.

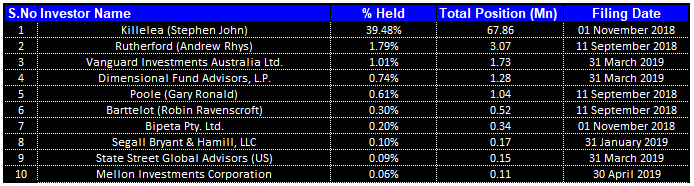

Top 10 Shareholders: Top ten shareholders form around 44.38% of the total shareholding as highlighted in the below table. Killelea (Stephen John) holds maximum interest in the company with a stake of 39.48% followed by Rutherford (Andrew Rhys) and Vanguard Investments Australia Ltd with a stake of 1.79% and 1.01%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

Outlook Going Forward: The company expects the profit growth for FY19 in underlying operational performance, but the reported financial performance will be influenced by fluctuations in currency exchange rates. The company has a well?crafted, multi?pronged strategy to grow through developing products in adjacent markets. It will be releasing new products for Payments, UC and real?time compliance monitoring. The company is in the progress of developing several artificial intelligence?based applications for its current markets.

The foundations of the business model are extremely strong with 88% of the revenue currently recurring as multi?year deals, and retention rates across the portfolio being greater than 90%. The compounding impact of recurring term renewals coupled with the expansion of the share of customer wallet, contributes significantly to strong future earnings.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

Method 1- EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 2- Price to Cash Flow multiple Approach (NTM):

P/CF Based Valuation (Source: Thomson Reuters)

Stock Recommendation: From the technical standpoints, the stock is currently trending upwards, taking support from its trendline. As witnessed earlier, the stock has bounced off from the trendline quite a few times which has increased the reliability of the trendline support. On the upside, the stock has potential till the nearest resistance of A$2.9. Fundamentally, IRI looks resilient with its robust top-line coupled with a strong balance sheet and other improved key performance indicators. The company performed well on the financial front during 1HFY19, continuing its decent performance over the years. IRI is poised for value creation through its efficient business model along with several key competitive advantages along with a diversified client base. However, financial risks in the form of foreign currency exchange rates and cash flow interest rate remain a key concern. Hence, we recommend a “Speculative Buy” rating on the stock at the current price of $2.490 (down 0.797% on 17 May 2019).

.png)

IRI Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...