Kalkine has a fully transformed New Avatar.

Company Overview: Integral Diagnostics Limited (ASX: IDX) is an Australian healthcare services company, which is engaged in providing Diagnostic Imaging Services to general practitioners, patients, medical specialists and allied health professionals. The business operates across Australia, New Zealand, Victoria and Queensland. As at January 2020, total number of employees stands at around 1,326 with 64 sites (including hospital sites) and 105 employed radiologists. The company employs few of the top Australia’s leading radiologists and nuclear medicine specialists to ensure quality patient care, service and access.

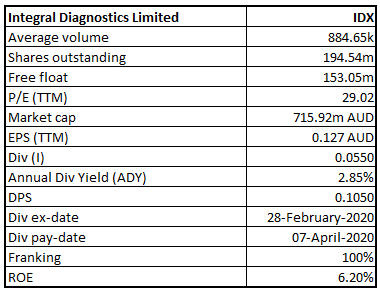

IDX Details

Growth Across All Business Units & Synergies from Acquisitions are Key Catalysts: Integral Diagnostics Limited (ASX: IDX) is engaged in providing medical imaging services across Australia, New Zealand, Victoria and Queensland. IDX offers state of the art diagnostic services to patients and their referrers at approximately 64 radiology clinics, which includes 20 hospital sites. The company offers necessary flexible, dependable and focused service, which is required to meet the growing demands of customers. The company’s integrated network offers effective and precise communication, permitting physicians to gain access to images at any point of time from any location.

For the half year ended 31 December 2019, the company’s operating revenue increased approximately 15.3% year over year and stood at $131.8 million. Operating EBITDA for the period increased ~29.6% year over year, resulting from the implementation of AASB 16. The results were positively impacted on the back of organic growth across all its business segments along with synergies from acquisitions. The ramp up phase of North Melbourne Specialist and Research Centre was another key positive during the period. During the period, the company has also undertaken major refurbishments at John Flynn Hospital on the Gold Coast and St John of God Hospital in Ballarat.

Going forward, IDX continues to focus on cost control, while investing to support its growth outlook. Notably, the company remains invested in people, technology and the future of its community to ensure continuous progress and best practice. The company took initiatives to commence an environmental program to assess its carbon footprint and other sustainability improvement schemes. Higher investments in scientific research and new technologies including cyber security and the privacy of patient data help the company to deliver improved patient experience.

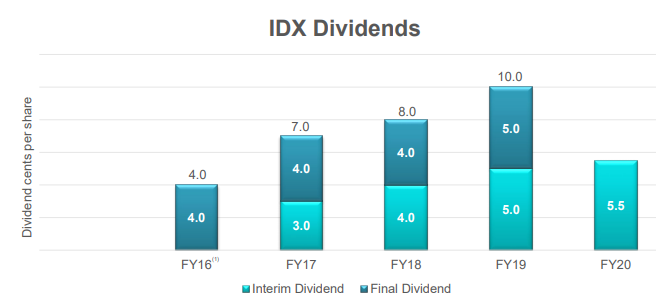

Growth bolstered as the company is developing its international revenue, on the heels of organic activities and acquisition synergies in international markets. Additionally, the company’s solid growth in new sites, investment in new equipment and two months’ contribution from Imaging Queensland were key catalysts. The board declared a fully franked interim dividend of 5.5 cents per share, up 10% year over year, payable on 7 April 2020. The below picture depicts the dividend performance over the period covering FY16 – 1HFY20.

Dividend (Source: Company Reports)

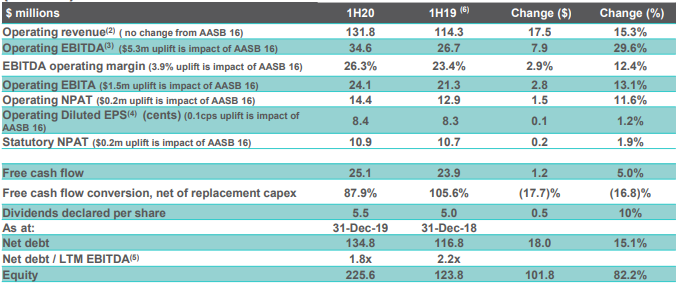

1HFY20 Financial Performance: During the period, revenue came in at $131.8 million, increasing 15.3% year over year. Operating EBITDA, including the impact of AASB 16, stood at $34.6 million, increasing ~29.6% year over year. Operating EBITDA margin for the period stood at 26.3%, as compared to 23.4% reported in the prior corresponding period. Operating NPAT increased 11.6% year over year and came in at $14.4 million. The company declared an interim dividend of 5.5 cents per share as compared to 5 cents in 1HFY19. Notably, in 1HFY20, organic Australian revenue came in at $109 million as compared to $102.1 million reported in 1HFY19. Contribution of revenue from New Zealand was $13.1 million in 1HFY20. The company witnessed growth across all business units. Average fee per exam (excluding reporting contracts and Imaging Queensland) increased by 1.3% during the period. In 1HFY20, employee costs rose by 1.3% as a percentage of revenue, driven by higher wages and higher investment in Radiologists remuneration structures.

1HFY20 Results (Source: Company Reports)

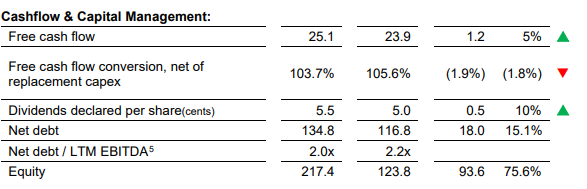

Balance Sheet & Cash Flow Position: At the end of the period, the company reported a cash balance of $26.8 million. The company’s net debt at the end of 1HFY20 came in at $134.8 million, up from $116.8 million at the end of 1HFY19. The weighted average cost of capital persists to decrease and net debt/EBITDA ratio as at 31 December 2019 stood at 2.0x, as compared to 2.2x in 1HFY20. Borrowings stood at $13.9 million at the end of the period, as compared to $9 million as at 30 June 2019. Net asset sat the end of the period stood at $225.6 million as compared to $127.2 million as at 30 June 2019. Free cash in 1HFY20 came in at $25.1 million as compared to $23.9 million in 1HFY19.

Capital Structure (Source: Company Reports)

Key Growth Strategies: The company witnessed increasing positive momentum throughout 1HFY20. IDX completed refurbishment of John Flynn Hospital on the Gold Coast, which included privately installed Digital PET scan along with a Cardiac CT. The company also completed renovation of St John of God Hospital in Ballarat creating a MRI supersite and installed new Cardiac CTs at Pindara Hospital and St John of God Hospital in Geelong. The company remains on track to invest in Radiologists and is focused on its social and governance program to confirm continuous progress and best practice. The company also took initiatives to implement FDA/TGA approved and successfully tested selective artificial intelligence software to aid workflow and focus on patient care. With the above scenario in place, the company is confident about retaining its existing customer base and expects to maintain a dominant growth momentum in FY20.

Recent Updates:

(a) Recently, the company stated that Integral Diagnostics Limited, a substantial holder of the company, has decreased its voting power from 15.82% to 13.82%.

(b) In another update, the company announced that 138,861 fully paid ordinary shares, which are presently held under voluntary escrow will be released on 5 March 2020.

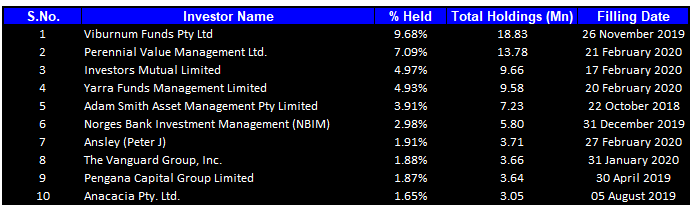

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 40.87% of the total shareholding. Viburnum Funds Pty Ltd is the entity holding maximum shares in the company at 9.68%. Perennial Value Management Ltd. is the second-largest shareholder, with a holding of 7.09%.

Top Ten Shareholders (Source: Thomson Reuters)

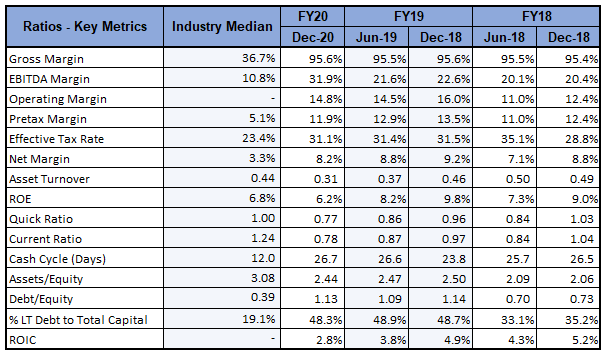

Key Metrics: In 1HFY20, the company had a gross margin and EBITDA margin of 95.6% and 31.9%, which is higher than the industry median of 36.7% and 10.8%, respectively, representing decent fundamentals. Net margins for 1HFY20 stood at 8.2%, higher than the industry median of 3.3%. Operating margin for the period came in at 14.8%, higher than 12.4% reported in 2HFY19.

Key Metrics (Source: Thomson Reuters)

Outlook: The company remains on track to expand its existing business, margins, sales team along with its Australia & New Zealand team with a full suite of products and strategic acquisitions. Further, the company is driving its organic growth, business integration and achieving further productivity gains by leveraging hub & spoke model along with optimising technology know-how. The company is focusing to integrate Imaging Queensland into the IDX Group in order to drive operating efficiencies across the entire business unit and open a new call centre in Victoria. The company is also working towards restraining costs and optimizing work, with the integration of Imaging Queensland. The company’s effort for R&D and product improvement will continue to innovate its product suite and will improve efficiency and aid diagnosis and early detection of diseases. It also remains on track to deliver on its environmental, social and governance agenda to apply best practice and is focused on improvement through application of right supply chains, responsible consumption and carbon footprint. The company’s balanced approach with respect to growth coupled with expansion of its existing portfolio reflects its progress towards sustainable future growth.

The healthcare companies are engaged in improving future approaches by executing digitalisation of their organisation. Furthermore, the increasing aged demographics has played a significant role in improving the spending of the healthcare industry. IDX stands to benefit from its planned approaches, considering numerous growth opportunities in a very active healthcare sector.

Artificial intelligence or AI has also been a thriving achievement in healthcare. With the support of AI, hospitals will accomplish better results, while patients will receive more effective, personalised, high quality and differentiated care. The company is leveraging the consolidated reporting platform to build sub speciality workflows for complicated clinical cases to provide the best in class comprehensive reports to patients. IDX’s strategy to expand its product portfolio and improve its AI execution through the latest technology advancement can additionally improve and enhance patient outcomes on a global basis.

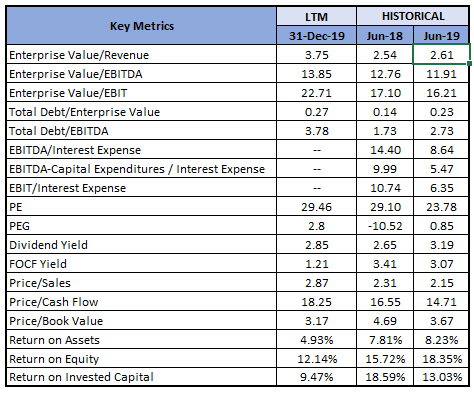

Key Valuation Metrics (Source: Thomson Reuters)

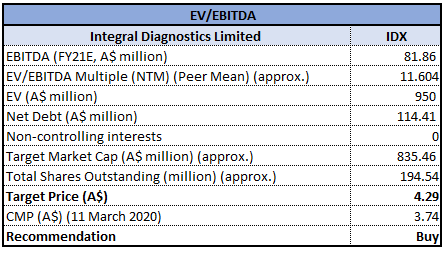

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation

EV/EBITDA Multiple Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company is currently trading above the average of its 52-week trading range of $2.328 - $4.390. The stock has a market cap of ~$715.92 million. In 1HFY20, the company delivered a stellar result, driven by increased investment in new technology as well as growth in itsbusiness segments along with synergies from acquisitions. Considering the above factors, we have valued the stock using EV/EBITDA multiple based relative valuation method and have arrived at a target price of lower double-digit growth (in percentage terms). For this purpose, we have considered the peers as Capitol Health Ltd (ASX: CAJ), Ramsay Health Care Ltd (ASX: RHC), Sonic Healthcare Ltd (ASX: SHL), and Healius Ltd (ASX: HLS), which comes under Healthcare Facilities & Services segment. Hence, we recommend a “Buy” rating on the stock at the current market price of $3.74, up 1.63% on 11 March 2020.

.png)

IDX Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...