Company Overview - Insurance Australia Group Limited is an Australia-based company engaged in underwriting of general insurance and related corporate services and investing activities. The Company operates in six segments: Australia direct insurance, Australia intermediated insurance, New Zealand insurance, Asia insurance, and corporate and other. Australia direct insurance consists of insurance products distributed through a network of branches, franchises and country service centers. Australia intermediated insurance consists of insurance products sold under the CGU and swan insurance brands through brokers and distribution partners. New Zealand insurance consists of general insurance business underwritten through subsidiaries in New Zealand. Asia insurance consists of intermediate and direct insurance business underwritten through subsidiaries in Thailand. Others include Corporate services and financial activities.

Analysis - Insurance Australia Group Ltd (ASX: IAG) Gross written premium (GWP) rose by 17.1% on year over year basis to $5.6 billion during the first half of 2015, as previous Wesfarmers business was included for the first time. Volume growth was mainly driven by the Personal Insurance business (represents 50% of IAG’s GWP), while all the other segments were on track. The group’s underlying insurance margin performance decreased to 13.3% during the period, as compared to 13.7% in first half of 2014, due to lower run rate coming from the Wesfarmers business. Moreover, the integration or restructuring benefits were not realized much to date.

Gross written premium and Underlying insurance margin performance (Source: Company Reports)

The Net natural peril claim costs reached $421 million, surpassing the half year allowance by $71 million, as it contained November Brisbane storm event impact of $165 million. The Prior period reserve releases decreased by 4.3% as compared to first half of 2014, reaching over $92 million, which is 1.8% of net earned premium. However, this is on line with the guidance of 2%. The impact from the narrowing of credit spreads slightly increased to $40 million, against the $39 million in prior corresponding period.

As per the divisional highlights, the Personal Insurance business GWP improved by 4.3% yoy to $2.8 billion in the first half of fiscal 2015, driven by the contribution from Wesfarmers personal insurance volumes along with the division’s organic growth. The underlying margin decreased to 14% against 14.5% in pcp due to lower reserve releases of 2.7% of NEP. The Commercial Insurance business GWP surged 43.9% yoy to $1.5 billion, which was also supported by the Wesfarmers business although like-for-like GWP growth declined due to softer commercial cycle. However, the reported margin fell to 6.6% in 1H15, from 18.5% in 1H14, on the back of lower reserve releases and adverse peril experience during the period.

New Zealand business GWP soared 26.2% yoy to $1.1 billion, contributed from the Lumley insurance. Meanwhile, the Organic GWP growth was driven by home and motor portfolios. The reported margin increased to 19.2% against 12.4% in 1H14, driven by natural perils experience. The Asian business witnessed strong GWP growth of around 4.8%, supported by India and Thailand growth. The total Asia’s earnings contribution soared to $17 million in 1H15, against just $7 million in pcp, as the Thailand and Malaysia business returned to growth.

IAG has a total investment portfolio of $15.2 billion. The group’s Investment income on shareholders’ funds decreased over 40% yoy to $137 million due to challenging equity market performance while the net profit after tax fell approximately 10% yoy to $579 million.

.png)

Investment Portfolio (Source: Company Reports)

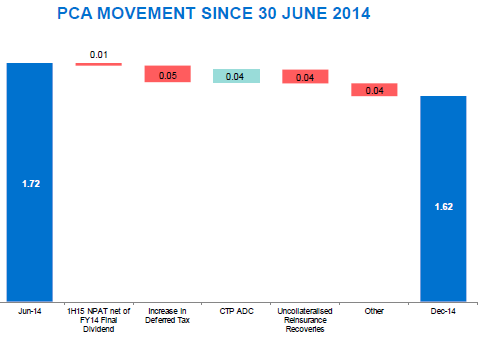

On the other hand, the company improved its capital position at 1.62 times the Prescribed Capital Amount (PCA) as of 31 December 2014, higher than the estimated range of 1.4-1.6 times the PCA. Moreover, the Common Equity Tier 1 (CET1) ratio was 1.04 in line with the forecasted target range of 0.9-1.1. IAG’s debt to total tangible capitalization ratio was 35.6%, also in line with the expected range of 30-40%.

Capital position (Source: Company Reports)

IAG declared a fully franked interim dividend of 13 cents per share, in line with last year’s corresponding period. Accordingly the cash payout ratio stood at 46.6%. The group intends to deliver full year payout policy in the range of 50% to 70% of the cash earnings.

The group was also undergoing significant management changes during this year. Quite recently, IAG has appointed Peter Harmer as Chief Executive IAG Labs to drive digital and innovation across IAG and its brands.

Strategic Alliance with Berkshire Hathaway

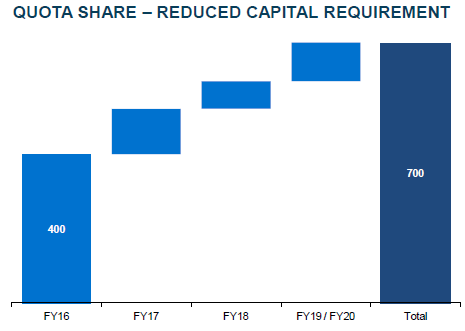

IAG formed strategic relationship with Berkshire Hathaway, entering into 20% quota share agreement across the group’s insurance business to decrease its earnings volatility and capital requirements for the next ten years. IAG intends to maintain its 15% return on equity with this move. The group forecasts the quota share arrangement to decrease its capital requirement of over $700 million for the next five years, while $400 million of that benefit is estimated to be realized by FY16. Meanwhile, the group has option to implement an extra 5% of IAG’s extended issued capital to Berkshire Hathaway in 24 months. However, Berkshire Hathaway is not eligible to increase its shareholding in the company above 14.9% under the partnership agreement. IAG already has reinsurance relationship since 2000 with Berkshire Hathaway, and took this relationship to the next level to leverage Berkshire Hathaway’s expertise.

Quota Share of IAG and Berkshire Hathaway (Source: Company Reports)

Berkshire Hathaway bought around 3.7% stake in Insurance Australia Groupthrough $500 million placement. Insurance Australia Group believes this agreement would give it the space to focus on growth opportunities in Asia Pacific and manage capital. Moreover, the company would purchase Berkshire Hathaway’s local personal and SME business lines, while Berkshire Hathaway would get the renewal rights to IAG’s large-corporate property and liability insurance business in Australia in return.

.png)

Capital Position after the agreement (Source: Company Reports)

Outlook

Insurance Australia Group continues to focus on Asian growth opportunities across India, Thailand, Malaysia, China, Vietnam and Indonesia. IAG intends to raise its stake in SBI General, the general insurance joint venture with State Bank of India, to 49% from 24% subsequent to the legislative changes on foreign ownership by the end of 2015 fiscal year. By acquiring PT Asuransi Parolamas, a small general insurance company, the group got insurance license in Indonesia. The group recently launched InsureLite, a new solution for families seeking for home insurance affordability stress in Queensland. Meanwhile, Insurance Australia Group got over 30,000 claims, as of 28 April due to major storms at New South Wales (NSW).

Division across Australia, New Zealand and Asia (Source: Company Reports)

The group forecasts its insurance margin to be in the range of 10.5% to 12.5% while the net losses from natural perils is estimated to reach $1 billion. Prior period reserve releases is expected to be over 2% of net earned premium. The GWP growth is estimated to be at the lower end of the 17-20% range. Meanwhile, the major component of the fiscal year 2015 is catastrophe reinsurance program which offers $450 million of protection in extra of $375 million.

IAG expects its FY16 reported insurance margin to be in the range of 14-16%. This estimate includes further realization of benefits from the Wesfarmers integration as well as the new Australian operating model, in addition to the impact from the Berkshire Hathaway quota share arrangement. Moreover, the underlying assumptions for this guidance included a net losses from natural perils estimate allowance of $600 million (after allowance for the quota share effect) and Prior period reserve releases to be at least 1% of NEP. Berkshire Hathaway impact is expected to enhance the reported insurance margin by approximately 200 basis points. IAG’s expectations for FY16 GWP growth are in the range of 0-3%.

IAG Daily Chart (Source - Thomson Reuters)

IAG Daily Chart (Source - Thomson Reuters)

The shares of Insurance Australia Group have been under pressure on the back of lower than expected first half of 2015 fiscal year results, with the stock posting a negative year to date returns of around 5.8%. However, the stock had been consolidating over the last three months delivering around 2.43% and has delivered a decent performance of 3.5% growth in the last four weeks, partly driven by the Berkshire Hathaway agreement. IAG is also trading at attractive valuations, with a P/E of 12.15x and has a dividend yield of 6.6%. We believe that the Berkshire Hathaway agreement impact and the growth from the Asian business could support the Insurance Australia Group stock further.

Based on the foregoing, we give a “BUY” recommendation to the stock at the current levels of $5.89.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...