Kalkine has a fully transformed New Avatar.

Company overview - Infomedia Ltd is a technology company. The principal activities of the Company are development and supply of Software as a Service (SaaS) offerings, including electronic parts catalogues and service quoting software systems, for the parts and service sectors of the global automotive industry, and information management, analysis and data creation for the domestic automotive and oil industries. The Company's segments are Asia Pacific; Europe, Middle East and Africa (EMEA); and Americas, which represents the combined North America and Latin & South America segments. The Company offers various solutions, such as Parts and Service, Data Management and Future Motors. The Company's Parts and Service solutions include Microcat, Superservice Menus, Superservice Triage, Superservice Insight, Superservice Connect, Superservice Register, Auto PartsBridge and Microcat MARKET. Its Data Management solutions include Lubricants Recommendation, Lubrication and Tune-up Guide and Data Consulting.

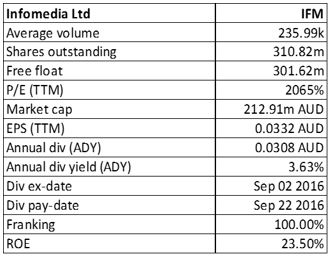

IFM Details

Transitional Year 2016: Infomedia Limited (ASX: IFM) reported that 2016 has been a year of transition for the company, and a major change in the second half of FY16 from January to the end of June 2016 was witnessed. The company took necessary strategies to deliver growth for the near term based on the five key areas of improvement. These areas include simplifying the business, accelerating the sales, prioritizing delivery to the customers and offering greater transparency to the employees, and to customers and the shareholders. Moreover, IFM took initiatives that include product enhancements and platform integration in the Superservice product. The company is focusing on their Superservice as their earlier system did not perform well. Superservice has better service process and management says that this is 30%-45% of recommended service. IFM also improved their parts sales by over 20%. This indicates the loyalty for clients and accordingly the company is focusing on customer satisfaction and service experience to derive more benefits. The company has also simplified structures to create a scalable structure to support future profitable growth. Additionally, to drive sales performance, IFM has renewed a number of existing contracts with global Automakers and is making strides in leveraging the opportunities with the Automaker relationships across all regions. In addition, IFM has finished the integration with Dealer management system or DMS provider Reynolds, integrated with a number of DMS providers across Europe though keeping in mind the US and Europe to operate quite differently. The company sees the level of DMS integration across all three regions as a competitive advantage. IFM has also entered into partnerships with Pentana and Autoloop who resell IFM’s products and offer IFM a greater global reach. In addition, IFM has introduced offshoring of some of the technology initiatives, enabling the company to scale up or down to meet demand. However, the core development of the software remains with the IFM’s in house technology team. Overall, given all the initiatives, there is a strong pipeline and new opportunities are emerging for the company.

FY16 Highlights (Source: Company Reports)

Strengthened core team in 2016: Jonathan Rubinsztein started the role of Managing Director and Chief Executive Officer (CEO) in March 2016. He had the experience of an entrepreneur and later as a corporate executive in the technology sector. Richard Leon got appointed as Chief Financial Officer (CFO) in April 2016. He was previously been the CFO of Altium Limited. Jonathan, Richard and the management team have taken substantial steps in driving IFM towards its future growth as a software as a service or SaaS company. Moreover, recently Paul Brandling joined the Board. He is the former CEO of Hewlett Packard in Australia and South Pacific, and has a great track record and reputation in the IT and software industry. Paul is also on the board of Integrated Research, which is another listed Australian software company. In addition, Bart Vogel has joined as the Chairman in October 2016. On the other hand, IFM made the long overdue move and shifted to the new development campus and headquarters in Belrose, North of Sydney in July 2016.

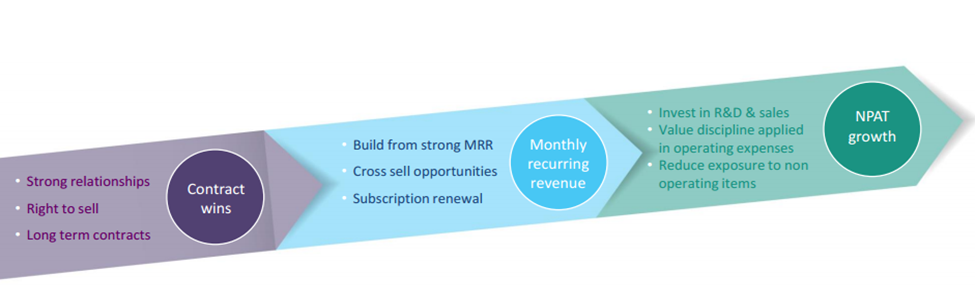

Positioning for future growth (Source: Company Reports)

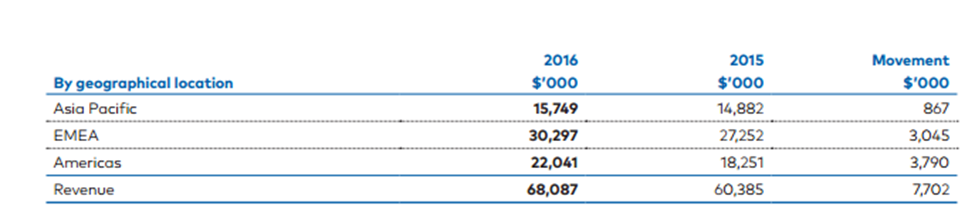

Secured Significant Contract from Nissan Europe: IFM got a major contract with Nissan Europe to deliver the world-leading Superservice product suite across their European dealership network. This would lead to the growth in the revenue and the productivity. On the other side, the company reported a 13% growth in the revenue to $68 million for fiscal year of 2016. The company has over 80% revenue outside of Australia while over 90% of revenue is represented by recurring revenue. IFM has accelerated investment in sales capacity and product delivery during FY16 and has set up the starting expense run-rate heading into FY17. However, net profit after tax (NPAT) fell 22% to $10.3 million due to the investments and forex losses. Moreover, the net current assets also fell to $13.2 million as of June 2016 as compared to $13.9 million in the same period of last year. Even, cash and cash equivalents reached $14.7 million as of FY16 ending as compared to $16.1 million in the same period of last year. However, the company has no debt as of FY16 balance sheet.

Fiscal year of 2016 (Source: Company Reports)

Future Outlook: IFM is expecting to deliver strong underlying revenue growth in the high single digits, which is in line with the industry growth rates. IFM’s focus continues for the improvement in the five key areas. The company reported that in the first quarter of 2017, the monthly recurring revenue (MRR) growth is expected to be modest. The revenue will gain momentum in the second quarter. Margin improvement is expected to be through disciplined cost control. Meanwhile, the company has net current assets of $13.2 million at June 2016 and after including cash and equivalents, the total is around $14.7 million to smoothly run day to day operations. The company has no debt. Moreover, since 2016 was the transitional year, the revenue growth is expected to maintain current momentum as the benefits of the company’s investment and structural efforts would start in the coming years. IFM is seeing continued top line growth in every region, and importantly, in every product line. Additionally, IFM has a strong pipeline of opportunities across the globe and is making progress in each of the product segments.

Media Reports of a takeover offer: IFM stock surged over 5% in last five days (as at January 30, 2017) driven by some reports from the media that a private equity operator is weighing up on IFM’s business and might consider making a bid to take ownership. For IFM, to secure the growth in the core business, the company needs to invest in the product development and in the execution capability. Since IFM’s business has organic growth potential, the board is considerate towards suitable M&A opportunities. However, the company at the moment has not indicated for any such move.

Stock Performance: IFM stock fell 3.95% in the last three months (as at January 30, 2017), impacted by the weak bottom line during fiscal year of 2016. Moreover, Jaguar Land Rover (JLR) decided that they are not extending their contract for EPC beyond December 2017. The company’s NPAT fall in fiscal year of 2016 was as expected by IFM in May 2016. Moreover, the restructuring costs for medium term growth also led to a weak bottom line. IFM is now investing in product development and sales capacity and pursuing several growth options in a number of near adjacency areas, from the new geographies, to new products, new global Automaker (OEM) customers, and new channels to market. The most powerful path to growth for the company remains in executing on the core promise to the existing loyal customers. IFM is also investing on Superservice Menus and Superservice Triage which is gaining traction. The company reported a final dividend of 2.65 cents per share for fiscal year of 2016 maintaining their intended dividend payout range of 75%-85% of NPAT. For FY17, the company forecasts a high single digit growth, and after FY17, they are focusing on organic growth and expects to achieve a growth rate better than the industry growth rate. IFM expects modest margin improvement in FY17 with costs expected to be contained to the FY16 run-rate. Meanwhile, IFM has a decent dividend yield and available at reasonable valuations. We give a “Buy” recommendation on the stock at the current price of – $ 0.72

.png)

IFM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...