Kalkine has a fully transformed New Avatar.

Company Overview: Incitec Pivot Limited is engaged in the manufacture and distribution of industrial explosives, industrial chemicals and fertilizers, and the provision of related services. The Company segments include Asia Pacific, Americas and Corporate. Its Asia Pacific segment includes Incitec Pivot Fertilizers (IPF), Southern Cross International (SCI) and Dyno Nobel Asia Pacific (DNAP). IPF manufactures and distributes fertilizers in Eastern Australia. SCI manufactures ammonium phosphates and is a distributor of its manufactured fertilizer product to wholesalers in Australia and the export market. DNAP manufactures and sells industrial explosives and related products and services to the mining industry in the Asia Pacific region and Turkey. Its Americas segment includes Dyno Nobel Americas (DNA), which manufactures and sells industrial explosives and related products and services to the mining, quarrying and construction industries in the Americas (the United States, Canada, Mexico and Chile).

.png)

IPL Details

Robust Balance Sheet with Strong Fundamentals: Incitec Pivot Limited (ASX: IPL) is engaged in the manufacture and distribution of industrial explosives, industrial chemicals and fertilisers, and the provision of related services. As on 17 February 2020, the market capitalisation of the company stood at ~$4.99 billion. In the recently held Annual General Meeting, the management of the company stated that the company has strong fundamentals and is progressing towards fulfilling its strategic agenda. During FY19, the company reported higher growth in the US Explosives market and recontracting, resulting in a strong underlying DNAP (Dyno Nobel in the Asia Pacific) business. In the same time span, revenue of the company witnessed an increase of 2% over the previous year and stood at $3.91 billion, up from $3.85 billion in FY18. During FY19, EBIT (Earnings before Interest and Taxes) of the company was $304 million and statutory NPAT (Net Profit After Tax) stood at $152 million. Despite the extreme weather conditions and impact of non-recurring items, the company completed the buyback of $300 million shares and declared a final, partially franked (30%) dividend of 3.4 cents per share. This brings the total dividend for fiscal Year 2019 to 4.7 cents per share, representing a payout ratio of 50% of Net Profit After Tax. The fundamentals underpinning the Australian explosives market remain strong, and the company reported a sound and robust balance sheet reflecting the Group’s ongoing commitment to financial discipline and effective cash management. As at 30 September 2019, IPL had a Net Debt of $1,691.4 million and net debt/EBITDA multiple of 2.8x.

The company’s ground-breaking technology program is offering its customers with safe and productive solutions for their mining and agricultural challenges and is focusing on reducing the environmental impact from operations. IPL is also aiming to increase productivity and efficiency in the customers’ operations in ways that help them achieve their productivity and efficiency goals. The company is also emphasising on the importance of Zero Harm and is setting a goal to achieve a 30% reduction in Total Recordable Injury Frequency Rate by next year. The manufacturing excellence, along with accelerating adoption of electronics and delivery systems by the mining industry, resulted in the growth in premium technology.

Stronger volumes and efficiencies in the explosive business are likely to deliver earnings growth in FY20 while the Waggaman plant is expected to deliver improved production as compared to 2019. The company also expects earnings growth in Agriculture & Industrial Chemicals. Incitec Pivot Limited also anticipates earnings upside in the medium term from the re-based business and is on track to deliver an increase of $40 to $50 million in earnings by FY22. .png)

FY19 Financial Highlights (Source: Company Reports)

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Incitec Pivot Limited. Harris Associates L.P. is the largest shareholder in the company, with a percentage holding of 8.47%..png)

Top 10 Shareholders (Source: Thomson Reuters)

Cost Management and Increasing Return to Shareholders: During FY19, gross margin of the company stood at 50.1% and EBITDA margin was 13.3%. In the same time span, net margin of the company witnessed a slight increase over the previous year and stood at 3.9%, up from 3% in FY18. This indicates that the company is managing its costs well and is capable of converting its revenue into profits. During FY19, Return on Equity stood at 3.2%, representing an increase from 2.3% in FY18. This implies that the company is well deploying the capital of its shareholders and is able to generate profits internally..png)

Key Margins (Source: Thomson Reuters)

Operational Performance of the Segments: The company has its assets in the leading mining markets, the US and Australia. The Dyno Nobel Americas (DNA) segment manufactures and sells industrial explosives and related products and also sells industrial chemicals to the agriculture and specialist industries. This segment contributes around 39% in group revenue. The 2019 earnings for Dyno Nobel Americas went down by US$48.1 to US$163.5 million. This was mainly due to the impact of non-recurring items which, however, was partially offset by the one-off profit from the sale of excess land in the US. Through another segment, Dyno Nobel Asia Pacific, IPL provides ammonium nitrate-based industrial explosives, initiating systems and services to the Coal and Base & Precious Metals sectors in several countries including Australia and Turkey, and contributes around 25% in group revenue. Dyno Nobel Asia Pacific earnings went down by 12.8% to $179.2 million. This was mainly due to a decline in joint venture earnings, contract re-basing and equipment repair costs incurred at the Moranbah plant. During FY19, explosive business performance remained strong with growing earnings, volumes and margins for a 3rd consecutive year, delivering a cumulative growth of 12.5% from FY16 to FY19.

The remaining 36% of revenue comes from the Fertilisers business in Australia which consists of Incitec Pivot Fertilisers and Southern Cross International. During FY19, fertiliser sales volumes were down by 9% mainly due to lower customer demand because of drought conditions in key planting areas.

Revenue Contribution (Source: Company Reports)

Strategic Review of Incitec Pivot Fertilisers: The company has informed the market about the strategic review of its Fertilisers Asia Pacific business segment, i.e., Incitec Pivot Fertilisers, which will help IPL to assess various options including a potential sale of the business, a demerger or retaining the business and continuing to invest for growth. This strategic review is expected to progress over the course of FY20. It stated that Incitec Pivot Fertilisers had made good progress on several strategic milestones including the rationalisation of Single Super Phosphates (SSP) manufacturing operations at Geelong. The company also negotiated various gas supply and other arrangements which allowed a continuation of manufacturing operations at Gibson Island.

Gibson Island Manufacturing to continue through 2022: The company will continue the manufacturing operations at its Gibson Island plant through to 31 December 2022 following the successful negotiation of multiple arrangements affecting operations. This will provide certainty to IPL’s customers and its valued employees. One of these arrangements was the gas supply from Australia Pacific LNG. As a result of continued operation of the plant, the company expects an increase in Earnings Before Interest and Tax by approximately $5 million in FY20. To deliver on the above expectation, a major turnaround is required to be undertaken to enable the operation of the plant to December 2022, which is likely to cost around $60 million.

Growth Opportunities and Future Expectations: Despite the challenging conditions in FY19, the company is optimistic for the future and remains confident in its strategy. It also expects to deliver sustainable returns for its shareholders. The excellence in its manufacturing performance is expected to deliver a significant increase in earnings by $40 to $50 million by fiscal year 2022. The company is also focusing on long-term opportunities and is prioritising year on year improvement across its zero-harm balanced scorecard.

The company expects continued growth in earnings of Dyno Nobel Americas and anticipates an increase in premium technology sales in Dyno Nobel Asia Pacific. The company has given guidance for its corporate and borrowing costs for FY20 and expects it to be around $30 million and $140 million, respectively. IPL also stated that production at the Gibson Island is likely to improve in comparison to FY19 and is expecting an earnings benefit of $5 million from new gas supply in FY20. It is prioritising to invest in technology to meet the expected growth in demand. FY20 sustenance capital expenditure, including turnarounds, is expected to range in between $260 million to $280 million. The company also expects an improvement in its free cash flows and has placed a clear focus on improving Return on Invested Capital.

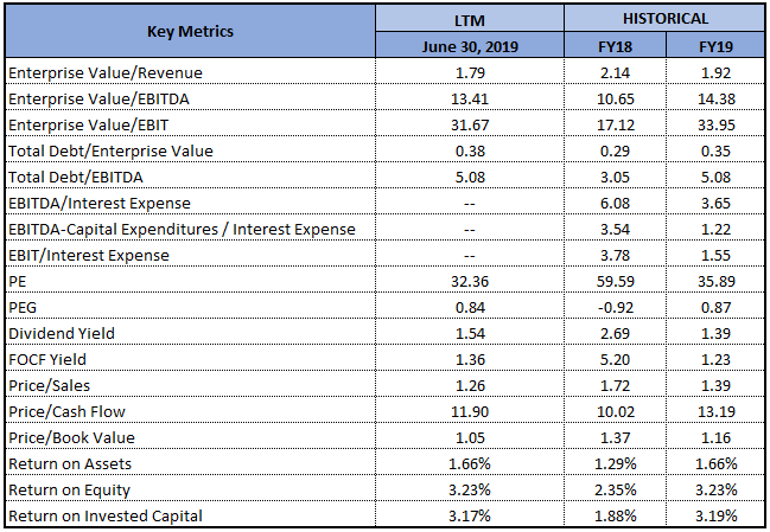

Key Valuation Metrics (Source: Thomson Reuters)

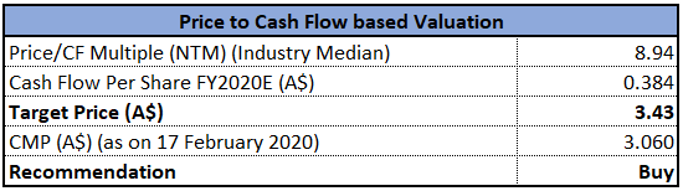

Valuation Methodology: Price to Cash Flow Multiple Approach

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.

Stock Recommendation: As per ASX, the stock of IPL is inclined towards its 52-weeks’ low level of $2.740, proffering a decent opportunity for accumulation. The company is expected to announce its half-yearly results in May 2020. Over the span of 3 years from FY16 to FY19, the company witnessed a CAGR of 5.27% in revenue and a CAGR of 1.52% in gross profit. While FY19 was a challenging year for the company, the Board is optimistic for the future and states that IPL is well-positioned to deliver significantly improved performance in the upcoming years. Considering the trading levels, CAGR in revenue, improvement in margins and growth opportunities, we have valued the stock using price to cash flow based relative valuation method and have arrived at a target price of lower double-digit growth (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $3.06, down by 0.971% on 17 February 2020.

IPL Daily Technical chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...