Company Overview: Incitec Pivot Limited is engaged in the manufacture and distribution of industrial explosives, industrial chemicals and fertilizers, and the provision of related services. The Company segments include Asia Pacific, Americas and Corporate. Its Asia Pacific segment includes Incitec Pivot Fertilizers (IPF), Southern Cross International (SCI) and Dyno Nobel Asia Pacific (DNAP). IPF manufactures and distributes fertilizers in Eastern Australia. SCI manufactures ammonium phosphates and is a distributor of its manufactured fertilizer product to wholesalers in Australia and the export market. DNAP manufactures and sells industrial explosives and related products and services to the mining industry in the Asia Pacific region and Turkey. Its Americas segment includes Dyno Nobel Americas (DNA), which manufactures and sells industrial explosives and related products and services to the mining, quarrying and construction industries in the Americas (the United States, Canada, Mexico and Chile).

(26).png)

IPL Details

Long-Term Growth Strategy Remains Intact: Incitec Pivot Limited (ASX: IPL) is engaged in the manufacture and distribution of industrial explosives, industrial chemicals and fertilisers and provides related services. As on December 9, 2019, the market capitalisation of IPL stood at ~A$4.99 billion. Over the last four years (FY16 to FY19), the company has registered a CAGR of 5.27% in its revenues. IPL’s gross profit has also increased by 1.52% CAGR over the same time period. The company’s operating income has witnessed a CAGR growth of 23.15% between FY16 to FY19. It can be said that IPL has decent capabilities to generate revenues, which could help it in achieving growth over the long term. Notably, the company’s net income has shown CAGR of 5.96% in the last four years between FY16 and FY19, which is, more or less, in line with its top-line growth. The company’s balance sheet is sound, which reflects the company’s ongoing commitment towards financial discipline and effective cash management. As at September 30, 2019, the company had net debt amounting to $1,691.4 million and net debt/EBITDA stood at 2.8x. Amidst the challenging environment, the company managed to declare a final dividend amounting to 3.4 cents per share (30% franked) and total dividend comes out to be 4.7 cents per share, which is equivalent to the payout ratio of 50% of NPAT.

The company experienced a challenging year due to several significant one-off weather events in Australia and the US during FY19. The results of the company were affected by an extended drought on the east coast of Australia, flood in North Queensland and flooding in mid-west USA. IPL reported a net profit after tax of $152.4 million, as compared to $208 million in FY18. The company reported earnings before interest and tax (EBIT) of $304 million, after $197 million of non-recurring items.

The company is seeking to maintain or develop competitive cost positions with respect to its chosen markets, and, at the same time, maintaining the quality product and service offerings. The focus on cost and quality places the business units to compete in medium to longer-term amidst changing and competitive environments. Also, earnings growth in explosives business, diversification of the customer base, respectable capabilities to garner revenues, decent balance sheet position are expected to act as tailwinds for long-term growth..png)

FY19 Financial Highlights (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in IPL:.png)

Overview of Key Margins: The company’s net margin stood at 3.9% in FY19, which reflects an improvement from FY18 figure of 3.0% and, therefore, it can be said that IPL has improved its capabilities to convert its top-line into the bottom-line. Notably, the company’s gross margin and EBITDA margin stood at 50.1% and 13.3%, respectively, in FY19. RoE stood at 3.2% in FY19, which is higher than the prior year figure of 2.3% and, therefore, it looks like that IPL is focused on delivering decent returns to its shareholders. The company’s percentage long-term debt to total capital stood at 19.6% in FY19, which reflects a fall from FY18 figure of 30.4% and, therefore, it can be said that the company’s exposure towards long-term debt has been reduced. This reduction might help the company in focusing on its long-term growth objectives and can place the company in a better position to deliver returns to its shareholders. There are expectations that the improvement in the capabilities to convert its top-line into the bottom-line, decent RoE and lower exposure towards long-term debt might help IPL in getting traction among market participants..png)

Key Metrics (Source: Thomson Reuters)

A Quick Look at Cash Flows: The company’s operating cash inflows decreased $247.9 million as compared to 2018, mainly due to a $245.7 million or 29 per cent decrease in EBITDA ex IMIs, mainly because of adverse impact from non-recurring items in 2019. Investing cash outflows increased $17.6 million, mainly due to lease buy-outs at term expiry in 2019, offset in part by lower sustenance spending as a result of lower major turnaround activity in 2019. Financing cash outflows decreased $288.5 million to $93.9 million mainly due to reduced spend on the repurchase of IPL shares under the $300 million share buyback program completed in 2019 and lower dividend payments in 2019 due to lower profits.

Segmental Performance: Dyno Nobel Americas reported FY19 earnings of US$164 million down from US$212 million in the pcp. These earnings include US$8 million of one-off profit on the sale of excess land in the US. After excluding the net impact from non-recurring items of US$36 million in FY19, EBIT stood at US$200 million. Dyno Nobel Americas business comprises three businesses: Explosives, Waggaman Operations, and Agriculture & Industrial Chemicals. Explosive business performance was decent underpinned by growth in earnings, volumes and margins during the year and delivered cumulative annual growth of 12.5% in the time span between 2016 and 2019. Despite prolongedwet weather conditions, flooding in the US mid-west, and impact from the coal industry declines, the earnings from the explosives business increased US$5.9 million, or 5 per cent as compared to 2018. The increase in earnings was mainly due to higher sales volumes, underpinned by growth in customer demand and delivery of operational costs savings and supply chain efficiency gains during the year.

Waggaman reported earnings of US$19.2 million for 2019, which decreased from US$76.2 million in 2018. The decrease was mainly due to the impact of manufacturing outages and lower ammonia prices compared to 2018. Agriculture and Industrial Chemicals reported earnings of US$0.2 million decreased from US$5.2 million in 2018. The decrease was largely due to the adverse US$12.0 million impact from a gas market disruption in 2019.

Overview of Fertilisers Asia Pacific Business: Fertilisers Asia Pacific reported an EBIT loss of $80 million, compared to a profit of $105 million in the pcp. After excluding the impact of $148 million from non-recurring items, EBIT was $68 million for the year. Overall, Fertilisers Asia Pacific sales volumes were 9 per cent down in 2019 at 2,752k mt, mainly as a result of lower customer demand due to drought conditions in Northern Victoria, New South Wales and Southern Queensland..png)

Fertilisers Asia Pacific EBIT Movements (Source: Company Reports)

The company added that fertilisers earnings would continue to be dependent on the global fertilisers prices, A$:US$ exchange rate, and weather conditions. Also, the Phosphate Hill plant is anticipated to deliver improved production of around 975k metric tonnes of the ammonium phosphates in 2020, with no planned turnarounds and all the known material production issues have now been resolved. The business is also anticipating additional benefits of around $8 million in 2020, which represents full-year impact of the lower gas supply cost to Phosphate Hill under Power and Water Corporation contract, which started in the month of January 2019.

Outlook for FY20: The outlook provided by the company assumes that the non-recurring items which were encountered in FY19 that amounted to $197 million, do not repeat in FY20. The explosives business is expected to continue delivering earnings growth in FY20, underpinned by stronger volumes and efficiencies. Waggaman plant is expected to deliver improved production compared to FY19 at slightly below nameplate capacity, with no planned outages scheduled for FY20. Agriculture & Industrial Chemicals operational earnings are expected to improve. The earnings from this business remain subject to movements in global fertilisers prices, particularly urea, and urea ammonium nitrate.

Fertilisers earnings will continue to be dependent on the A$: US$ exchange rate, global fertilisers prices and weather conditions. However, drought conditions in Queensland and New South Wales could continue to impact irrigation water availability in the key summer crop markets in FY20. Demand for ammonium nitrate in Australia is expected to remain strong in 2020. In line with business strategy, sales volumes relating to Moranbah in Australia are expected to be lower in 2020 following contract renewals.

The net borrowing costs are expected to be lower at roughly $140 million due to lower average cost of funding after the completion of the company’s debt refinancing in 2019 and lower anticipated debt levels through FY20. The company’s corporate costs are expected to be approximately $30 million in FY20, and it excludes any costs in relation to the Fertilisers strategic review..png)

Key Valuation Metrics (Source: Thomson Reuters)

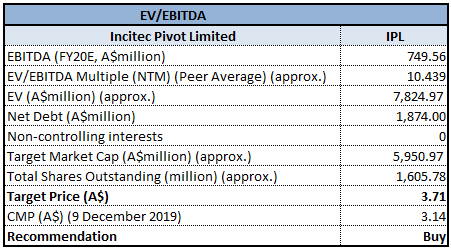

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Multiple Approach (Source: Thomson Reuters), NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The company’s stock has witnessed a fall of 13.37% in the span of the previous one month, while, in the time frame of the previous three months, the stock fell 5.18%. As per ASX, the stock is trading below the average of 52-week high and low levels of $3.910 and $2.740, respectively, indicating a decent opportunity for accumulation. The company is attempting to diversify the customer base in order to reduce any potential impact of the loss of any single customer. Based on the foregoing, we have valued the stock by using a relative valuation method, i.e., EV/EBITDA multiple, and arrived at a target price of lower double-digit growth (in percentage terms). Hence, we give a “Buy” rating on the stock at the current market price of A$3.140 per share (up 0.965% on 9 December 2019).

IPL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...