Company Overview - Incitec Pivot Limited (Incitec) is an Australia-based company engaged in the manufacture, trading and distribution of fertilizers, industrial explosives and chemicals, and the provision of related services. The Company operates through two segments: Fertilisers and Explosives. The Fertilisers segment includes Incitec Pivot Fertilizers (IPF), which manufactures and distributes fertilizers in Eastern Australia, and Southern Cross International, which manufactures Ammonium Phosphates and is a distributor of its manufactured fertilizer product to wholesalers in Australia (including IPF) and the export market. The Explosives segment includes Dyno Nobel Americas, which manufactures and sells industrial explosives and related products and services to the mining, quarrying and construction industries in the Americas, and manufactures and sells agricultural chemicals, and Dyno Nobel Asia Pacific, which manufactures and sells industrial explosives and related products to the mining industry.

.png)

IPL Details

Half yearly performance:Incitec Pivot Ltd (ASX: IPL) reported a 4.4% decline in revenues to $1.5 billion for the half year of FY16 while the group witnessed $20 million impact to EBIT from derailment. The Group EBIT ex IMIs was down 8.5% over corresponding period while NPAT excluding impairments was down by 6.4% to $137.1 million. With impairment charge, the group’s net profit after tax reached $31.5 million, which comprises over $105.6 million non-cash impairment to the asset value of the Gibson Island fertilizer manufacturing plant. The weak half yearly performance was also on the back of 28% decline in Middle East Granular Urea prices, 26% decline in US Gulf Urea prices and 18% declin

e in DAP Tampa prices. The company has declared interim dividend of 4.1 cents. Incitec Pivot delivered a production of 501,000 tonnes of ammonium phosphates at Phosphate Hill including three record production months and even reported a strong Moranbah production of 174,288 tonnes of ammonium nitrate equivalent along with the plant’s one-million tonne manufactured during the half year of fiscal 2016.

.png)

Six months ended on March 2016 financial performance (Source: Company reports)

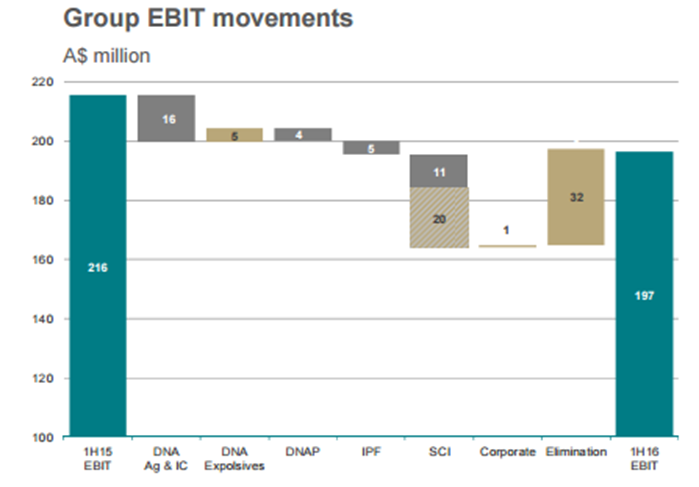

Segment Performance: As per theDyno Nobel Americas business segment performance, the explosives EBIT margin expanded 1.9% as compared to the same period of last year (even though tough market conditions prevailed in North America coal industry) on the back of better customer mix and BEx efficiencies. This along with 10.5% Q&C rise has partly offset challenging coal volumes. On an overall note, Explosives EBIT fell by 3.8% against prior corresponding period. Ag & IC EBIT have contracted 77.3% from US$17.6 million to US$4.0 million on a period over period basis due to declining global fertilizer prices and the St. Helens turnaround. DNA’s EBIT lost from US$61.8 million to US$46.5 million during the period.

With regards to the Dyno Nobel Asia Pacific (DNAP) segment, the revenue surged 4.4% as compared to the same period of last year on the back of rising customers ANE volumes to lower mine costs. But, EBIT fell 4.8% on a year over year basis on the back of unfavorable product mix, decrease in services contribution and mine closures in the Hard Rock & Underground segment. For Incitec Pivot Fertilizers, the volumes fell over 24.6% in the first half due to dry conditions in Northern Victoria, South Australia and Queensland, as well as deferring purchases from buyers due to falling fertilizer prices and rising competition. As a result, the revenues and EBIT excluding impairments fell over 21% and 23.7%, respectively, during the period.

Group EBIT movements (Source: Company Reports)

Controlling cost of production: First production from the new plant is due in the second half of this year. This coincides at a time where gas prices, which account for 75% of the cost of producing ammonia, are at all time lows.

The continuing depreciation of the Australian dollar against the US dollar also means earnings from this project are likely to receive a translational benefit making Incitec’s investment decision into Louisiana well timed. Going forward, to mitigate the impact of gas price fluctuations, Incitec has entered into QGC contract to reduce cost by over $20 million per year from 2017 and also PWC contract to reduce gas costs by further $35 million per year from 2019. The Phosphate Hill production would benefit from these two contracts.

Management’s effective steps during mining slowdown: The management has already taken positive steps to support for a mining slowdown. Incitec has invested heavily in its fertilizer business by constructing a state-of-the-art ammonia production facility in Louisiana, U.S.Total project costs was USD $850 million and company has spent over US$712 million till March 2016. The project is 97% complete and management expects that the production would commence in third quarter of fiscal year of 2016.

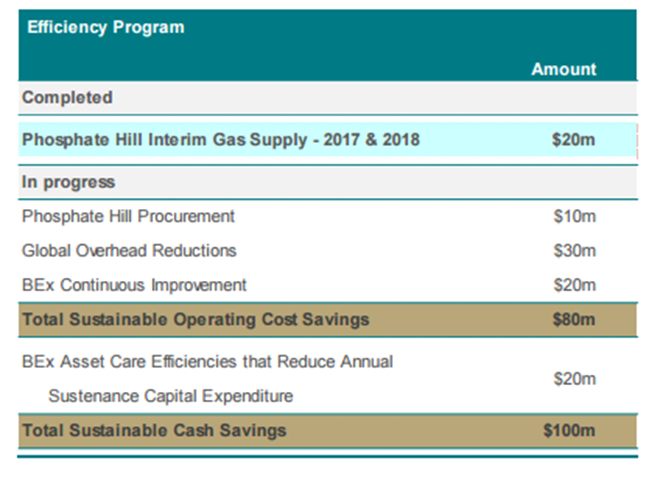

The Group announced an accelerated timeline to deliver $100 million in sustainable operating cost and cash savings by 2017.The group has 5-year plan set in 2012 to reduce TRIFR (Total recordable injury frequency rate) to less than 1 by 2016, till date and even achieved 52% reduction and TRIFR for 12-month rolling as of 31 March 2016 is at 0.66. The Group already delivered productivity benefits of $22.5 million as of first half of 2016 as a part of its BEx (Business Excellence) efforts.

Business Excellence efforts outcome (Source: Company Reports)

Production loss due to train derailment: On 27 December 2015, Aurizon’s supply train derailed near Julia Creek in Queensland. It was carrying 200,000 liters of a key ingredient for making fertilizer use at Incitec’s flagship Phosphate Hill production facility.

The incident is expected to wipe a one-off $14 million from full year net profit after tax (NPAT), equating to 3.5% of 2015 full year NPAT. Incitec’s management has opted to bring forward maintenance to offset any loss in production of phosphate fertilizer. The management reiterates that the Group is still on the track to reach its 950,000 tonne production target at Phosphate Hill, despite the derailment.

.png)

Train derailment impact (Source: Company Reports)

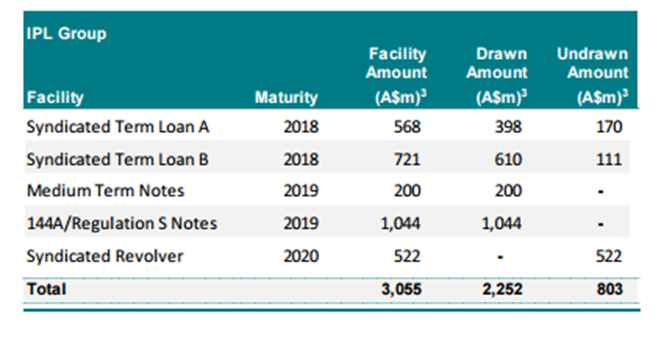

Strong balance sheet: Incitec Pivothas a debt facility of $3.05 billion as of half year ended on March 31, 2016 of which $803 million are undrawn amount even though the group spent over $129 million on Louisiana project.

The interest cover is at 9.5x while net debt/ EBITDA is 2:1x. The group has over $803 million of headroom. IPL’s Investment Grade credit ratings are also steady and the company intends to maintain a 50% of net profit after tax payout ratio, excluding IMIs.

Debt facilities (Source: Company Reports)

Guidance: The group estimates challenging market conditions given the over supplied commodity markets and global economic uncertainty due to volatile China’s economy transitions and accordingly expects a resilience in its business.

The group forecasts a flat earnings after adjusting for impact of the December train derailment and impairment to Gibson Island. On the other hand, the group’s manufacturing performance at Phosphate Hill and Moranbah is solid while Louisiana project is 97% finished. Management reported that they are on track for a “beneficial production” in Louisiana for the third quarter of 2016. The group’s ongoing US Q&C growth is underpinned by US$305 billion highway spending bill. IPL is also undertaking “Transformative step” to build a better Australian fertilizer cooperative to global diversified industrial chemicals business.

Stock Performance: The shares of IPL have fallen over 13.6% (as of June 03, 2016) in the last one year on the back of slowdown in the mining and pressure in commodity prices. However, Incitec Pivot has the right formula to make for an explosive comeback when the commodity cycle turns. Moreover, the recent recovery in the commodity prices have driven the IPL prices by 12.3% (as of June 03, 2016) in the last three months alone. The cost reduction steps would further enhance the profitability going forward. In addition, the group intends to leverage the shale gas revolution in the US by developing world-scale ammonia plant in Louisiana and reported that they maintain their decision even though the US gas prices are around US$2.00/MMBTU (as of first half of 2016 company reports).

Going forward, we believe that the company would benefit from improving gas prices and demand coupled with its better production outcome. IPL also demonstrates effective capital discipline and is capable of exhibiting higher asset turns and ROEs with surge in operating free cashflow expected from 2017 given the US$850m Louisiana ammonia plant’s progress. Capex is expected to moderate from next year given the availability of some free cashflow for activities including capital management. Based on the foregoing, we give a “Buy” on this dividend yield stock at the current price of $3.37

IPL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...