Company Overview - Incitec Pivot Limited (Incitec) is an Australia-based company engaged in the manufacture, trading and distribution of fertilizers, industrial explosives and chemicals, and the provision of related services. It operates through two segments, including Fertilizers and Explosives. The Fertilizers segment includes Incitec Pivot Fertilizers (IPF), which manufactures and distributes fertilizers in Eastern Australia, and Southern Cross International, which manufactures Ammonium Phosphates, and is a distributor of its manufactured fertilizer product to wholesalers in Australia (including IPF) and the export market. The Explosives segment includes Dyno Nobel Americas (manufacture and sale of industrial explosives and related products and services to the mining, quarrying and construction industries in the Americas, and the manufacture and sale of Agricultural chemicals), and Dyno Nobel Asia Pacific, (manufacture and sale of industrial explosives and related products to the mining industry.

.png)

IPL Dividend Details

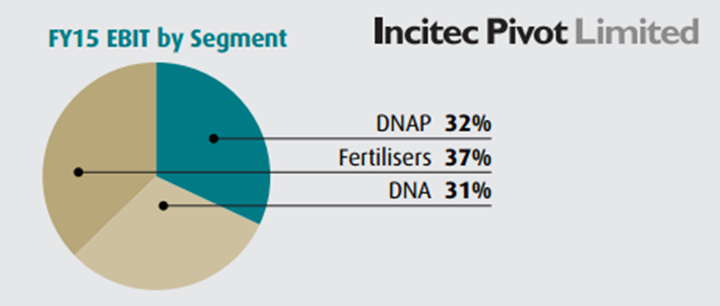

Rising Phosphate Hill production coupled with falling Australian dollar drove financial performance: Incitec Pivot Ltd (ASX: IPL) reported a 12% rise of Net Profit After Tax (without the Individually Material Items) to $398.6 million in fiscal year of 2015 as compared to $356.3 million in fiscal year of 2014, on the back of solid production from Phosphate Hill coupled with declining Australian dollar contribution. IPL generated a revenue surge of 9% year on year (yoy) to $3,643.3 million during the period boosted by the Fertilizer revenue driven by Phosphate Hill production despite the drought impact in Northern New South Wales and Queensland. The Fertilizer business EBIT surged by 22% to $224.1 million in FY15 as compared to $183.4 million in prior corresponding period (pcp) even though the Incitec Pivot Fertilizers segment EBIT declined by 51% on a yoy basis. This Fertilizer business EBIT rise was mainly due to strong Southern Cross International growth of 120% yoy during the year. But, the segment’s distribution margins were impacted by the seasonal affects, rising competition, urea purchase timing and declining production volume from the Gibson Island plant. However, Phosphate Hill delivered record production of 1,043kt of ammonium phosphates during fiscal year of 2015. As per the Explosives business performance, the EBIT rose just 1% yoy in FY15 as Dyno Nobel Asia Pacific (DNAP) EBIT fell by 5% yoy in spite of strong Dyno Nobel Americas (DNA) EBIT increase by 10% yoy. DNA explosives EBIT under Australian dollar terms increased during the period on the back of positive foreign exchange translation contribution. But, the DNA EBIT under US dollar fell during the period impacted by the falling commodity prices. On the other hand, strong production of 320kt from Moranbah had offset this impact to a certain extent.

Fiscal year of 2015 EBIT performance (Source: Company Reports)

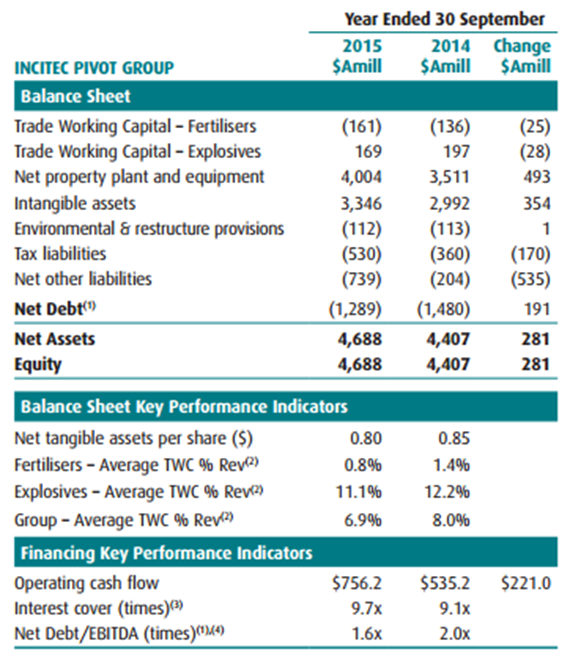

Strengthening balance sheet: Incitec Pivot’s operating cash flow surged by 41% to $756.2 million in FY15 as compared to $535.2 million in FY14 boosted by solid EBITDA increase. The operating cash flow was also driven by the decrease in Trade Working Capital (TWC) to $8 million as of September 2015 as compared to $53 million in September 2014 due to decrease in inventory levels and fertilizer imports timing.

The group decreased its net debt by 13% yoy to $1.3 billion during fiscal year of 2015 while net debt to EBITDA is 1.6 times within the group’s estimated target range despite investments at Louisiana ammonia plant (WALA). Interest cover rose to 9.7 times as of September 2015 as compared to 9.1 times in pcp. Incitec improved its dividends by 9% to 11.8 cents per share during fiscal year of 2015 against fiscal year of 2014.

Targeting further efficiency through Business Excellence program: The group’s Business Excellence program helped them to derive a net EBIT benefits of $41 million during fiscal year of 2015. Management reported that they were able to generate such strong benefits mainly from the contribution of their employees who used the group’s Business Excellence (BEx) system for enhancing productivity coupled with decreasing waste. IPL intends to further improve its manufacturing and supply chain performance in the coming periods. The group was even able to improve its core Ammonium Phosphate Value Chain through the Business Excellence program. The Phosphate Hill fertilizer plant being the major manufacturing unit among the group’s global operations was able to deliver a record production increase by 35% to 1,043,000 tonnes of ammonium phosphate fertilizers during fiscal year of 2015. This is the first time for the plant to cross one million tonnes in its history (IPL acquired Phosphate Hill fertilizer plant in 2006).

Moreover, Phosphate Hill EBIT surged $105 million to $142 million despite rising input costs (especially gas). This strong performance in the plant indicates the ability of the group to use its Business Excellence process for achieving better production. Recently, Northern Territory Government approved building a new gas pipeline from Tennant Creek to Mt Isa as part of a coordinated project with the Queensland Government. The group is among the initial customer of this new pipeline which would offer conventional gas to its Phosphate Hill plant in North West Queensland for over 10 years from 2018. As a result, the group forecast to further decrease its gas costs by over $55 million as compared to its present cost.

Financial position as of FY15 (Source: Company Reports)

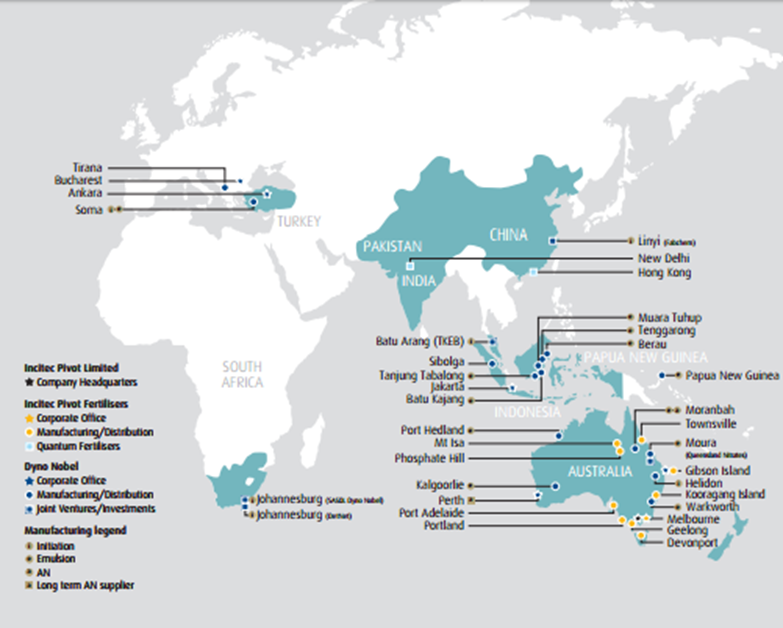

Growth Strategy: Incitec Pivot is developing a $1 billion Moranbah ammonium nitrate plant to position itself for addressing the long term demand of resources coming from the Asian regions especially from China as well as from America. However, due to the declining demand of resources since the last few periods, IPL have decided to decrease the production from its Moranbah during this present cycle. But, the group’s Dyno Nobel Asia Pacific business impact (given the tough mining conditions at Australia, Indonesia and Turkey) during fiscal year of 2015 was slightly offset by the better performance of the Moranbah plant which produced 320,000 tons of ammonium nitrate and delivered a total earnings of $131 million. Meanwhile, IPL is also investing on WALA, which is the group’s new ammonia plant in Louisiana to leverage the long term potential boom of the shale gas in the United States.

IPL has invested over $256.4 million in WALA during 2015. This plant is currently under construction while IPL estimates this plant to begin by the next year ending. Once the plant goes live, the group expects a significant improvement in its Dyno Nobel Americas business, which would lead to strong cash flows and consequently boost the group’s balance sheet. Meanwhile, IPL incurred a sustenance capital of $100 million during fiscal year of 2015, which includes the St Helens upgrading activities, new Phosphate Hill gypsum cell completion and ground work for the 2016 Gibson Island turnaround.

Incitec footprint across the globe (Source: Company Reports)

Stock Performance: Incitec Pivot Ltd (ASX: IPL) stock plunged over 19.10% during this year to date (as of March 11, 2016) as the group estimated an adverse one-off impact from its train derailment during December 2015. IPL forecasts this impact to be around $14 million on its fiscal year of 2016 Net Profit after Tax. However, Queensland Rail is currently building access roads to start construction of a rail deviation around the derailment site despite the wet weather conditions impact. The rail services connecting Incitec Pivot's Mt Isa and Phosphate Hill facilities are ongoing. Meanwhile, IPL reported that they will be able to maintain their Phosphate Hill plant production of over 950,000 tonnes of fertilizer for fiscal year of 2016. Moreover, IPL has a strong balance sheet and its Business excellence program would continue to improve its efficiency for the coming periods. As a result, we believe that the recent correction in the stock offers an attractive investment opportunity for long term investors who are adding bargain stocks in their portfolio.

IPL is also positioning itself to address the long term demand from Asia and America though its investments in Moranbah ammonium nitrate plant and WALA. Moreover, the recent decline in the stock placed IPL stock at attractive valuations, which is trading at a relatively cheaper P/E as compared to its peers. IPL offers a decent dividend yield. The stock recovered by 12.2% in the last four weeks (as of March 11, 2016) and we believe that this positive momentum in the stock would continue in the coming months. Based on the foregoing, we give a “BUY” recommendation on this stock at the current price of $3.23

IPL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...