Company Overview - Iluka Resources Limited is an Australia-based mineral sands exploration, project development, operations and marketing company. It is the producer of zircon and titanium dioxide products of rutile and synthetic rutile, with operations in Australia and Virginia. It operates through the following segments: Australia (AUS), United States (US) and Mining Area C (MAC). The AUS segment comprises the integrated mineral sands mining and processing operations in Victoria, Western Australia and South Australia. The US segment comprises the integrated mineral sands mining and processing operations in Virginia and rehabilitation obligations in Florida. The MAC segment comprises a deferred consideration iron ore royalty interest over certain mining tenements in Australia operated by BHP Billiton Iron Ore.

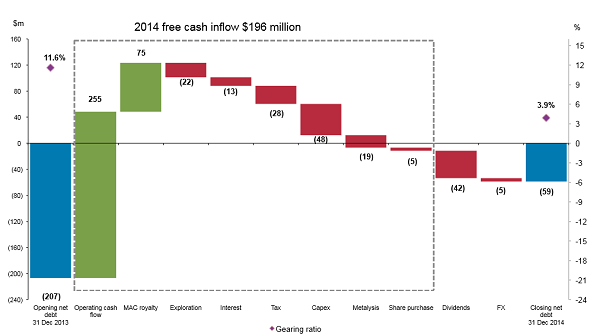

Analysis - In this report, we cover Iluka Resources (ILU) which recently reported a full-year loss. The Company is still witnessing rise in share price given the signs of recovery in mineral sands market. The full year results to 31 December 2014 entailed a loss after tax of $62.5 million (net profit after tax of $18.5 million in 2013). This included a non-cash impairment charge of $86.5 million after tax. The results also got affected by lower prices for ILU’s zircon and titanium dioxide products, and reduced iron ore royalties. Nonetheless, ILU demonstrated robust financial position with free cash flow of $196.3 million versus a free cash outflow of $27.5 million in 2013. A low net debt with gearing 3.9% was conveyed. Specifically, the net debt was $59.0 million as at 31 December 2014, which indicates a drop of $147.6 million compared with the previous corresponding period. The undrawn facilities and cash at bank as at 31 December 2014 amounts to $809.1 million.

Net Debt Movement 2014 (Source – Company Reports)

Cash costs of production increased marginally by 1.5% to $381.9 million. The Company reported for lesser unit cash costs of production with a Group EBITDA margin of 32.5%. The unit cost of goods sold (cash and non-cash cost) was lower year-on-year at $862/tonne of Z/R/SR in comparison to $890/tonne of Z/R/SR in 2013. The full year operating cash flow of $254.8 million was reported to be higher than $124.0 million of 2013. This was primarily owing to earlier cash realisations from sales. Mining Area C (MAC) cash flows of $75.2 million are lower than 2013 ($82.7 million) due to lower MAC royalty income. The tax payments in the year of $27.5 million were noted to be lower than $140.1 million of 2013. Further, capital expenditure was $66.9 million as opposed to $52.5 million in 2013. This included $18.6 million associated with acquisition of an 18.3% equity investment in the UK metal powder technology company, named Metalysis Limited. ILU also reported about its continued discussions and evaluation with regards to the mineral sands miner Kenmare Resources for which updates will be provided by the Company as and when applicable.

The full year dividend of 19.0 cents per share fully franked (representing a dividend yield of 2.6 per cent) was paid. This primarily represented a 40% payout of free cash flow in 2014. ILU has now determined a fully franked dividend of 13.0 cents per share payable on 31 March 2015 in view of the robust free cash flow.

The Company also conveyed its efforts with regards to continued investment in various growth options. The result affected by the impairment of US operations kind of indicates industry’s cyclical low, but at the same time, other attributes such as free cash flow etc. divulge an optimistic market sentiment going forward. ILU’s management is thus poised to expect topline growth, margin expansion, inventory monetisation and another low capex year in 2015.

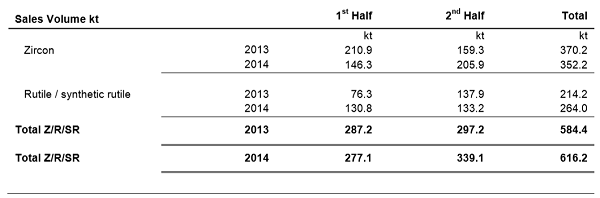

Sales Trends for Iluka’s Main Products (Source – Company Reports)

The mineral sands revenue of $724.9 million was 5.0% lower than 2013, while 5.4% higher sales volumes of the main products of zircon, rutile and synthetic rutile (Z/R/SR) was reported. This was equipoised by lower weighted average received prices. The outcomes for the weighted average price in 2014 were accompanied by lowering of high grade titanium dioxide prices in the first part of 2014 and steady zircon prices. The minerals sands EBITDA margin was 32.9% as opposed to 32.6% in 2013. MAC iron ore royalty earnings got lowered by 24.5% to $66.4 million (2013 - $87.9 million) indicative of a 23.2% decrease in the average AUD iron ore price upon which the royalty is paid. 2014 earnings include a $1.0 million capacity payment. The increase in pigment plant utilisation is expected to translate into higher grade feedstocks.

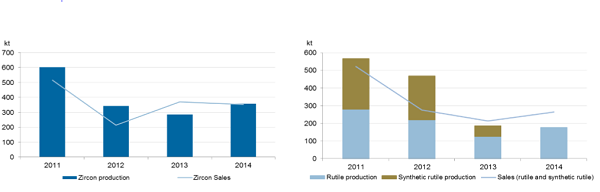

Production Reflects Market Conditions (Source – Company Reports)

The increase in zircon sales volumes continued in December 2014. Further, ILU’s zircon sales volumes sustained to be higher in the December 2014 quarter. There was an increase in shipments by more than 40% in the second half of CY2014 while the effect on the zircon price was low. There is a possibility to have an upsurge in demand. Higher sales are also expected to further demand growth which can in turn result in an upswing in prices. It is also noted that there was a soft demand in Europe, Middle East and India, while North America and China were the most robust markets. A recovery in demand with regards to the zirconium chemical sector has been witnessed in the second half. The key features of the high grade titanium dioxide market entailed higher sales volumes of high grade feedstocks (R/SR) and substantive progress on commercial arrangements for a restart of ILU’s largest synthetic rutile kiln in 2015.

Global TiO2 Operating Rates (Source – Company Reports)

All-in-all, the Company is found to be having a good financial strength with strong statistics on free cash flow, low gearing, funding headroom, increased dividend and so forth, while the profit was noted to be below par.

Tapira, Brazil (Source – Company Reports)

Efforts with regards to advancement of mineral sands project, expansion of exploration efforts, activities such as technical evaluation of a new high grade sulphate feedstock and new mineral sands mining techniques for development of non-traditional mineral sands deposits, technical evaluation and market studies for Tapira mineralisation in Brazil, etc. indicate great potential. For instance, evaluation at Balranald and Cataby reflects financial returns to be higher than risk weighted hurdle rates. Other developments such as three new points of global marketing representation, eight new products, and plans for the opening of a China Technical Centre in 2015 focusing on chloride and sulphate pigment feedstock opportunities in China have been noted. The announcement indicating ILU’s plans to close Virginia operations in 2015 although comes with a disappointment.

Iluka Daily Chart (Source - Thomson Reuters)

From ILU’s standpoint, 2015 may witness Z/R production higher than 2014 with sales exceeding 2015 production and 2014 Z/R sales; and potential synthetic rutile kiln 2 (SR 2) production and sales. A further reduction in unit cash costs of production with inventory draw down, free cash flow generation weighted in second half are also anticipated. Thus, a slight miss to guidance on CY14 production does not look to be an issue to ponder over in view of many other positives with regards to balance sheet, existing stockpiles, expected upsurge for zircon sales, recovery in titanium dioxide prices, strong 4Q14 production and sales results indicative of future prospects, which look good enough for steering the growth in share price in near future.

Accordingly, we reiterate a BUY recommendation for the stock at the current price of $7.70.

Please wait processing your request...

Please wait processing your request...