Company Overview - Iluka Resources Limited is the producer of zircon globally and producer of the titanium dioxide products of rutile and synthetic rutile, with operations in Australia and Virginia, United States. It operates in five segments: Eucla/Perth Basin, which consist of integrated mineral sands mining and processing operations in Western Australia and South Australia; Murray Basin, which consist of integrated mineral sands mining and processing operations in Victoria; Australia, which consist of mineral sands operations in Australia; United States, which consist of integrated mineral sands mining and processing operations in Virginia, and Mining Area C, which consists of a deferred consideration iron ore royalty interest over certain mining tenements in Australia. In April 2014, Iluka Resources Ltd announced that National Australia Bank Limited and its associated ceased to be a substantial share holder of the Company.

Analysis - Iluka Resources (ILU) in its 2014 half year results highlighted healthy performance with asset operation in line with market demand and continued market development. The Company indicated maintaining a strong balance sheet while having good growth opportunities and its aim to focus on shareholder returns through the cycle.

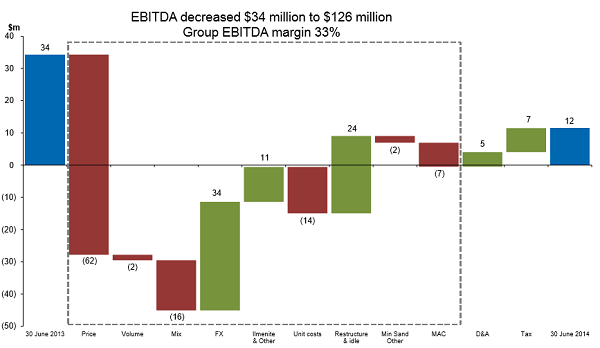

Net Profit after Tax and EBITDA (Source – Company Reports)

Net Profit after Tax and EBITDA (Source – Company Reports)

The Company reported for a free cash flow of $63.9 million and 6 cents dividend per share fully franked. The gearing ratio reduced to 9.2%. The cash costs of production was $200.7 million which was below FY guidance (~$430 million). The unit cash costs/tonne of zircon, rutile and synthetic rutile (Z/R/SR) produced $796 and Z/R/SR revenue/tonne was $1,015. Another highlight was the SA Premier’s Award for Environmental Excellence.

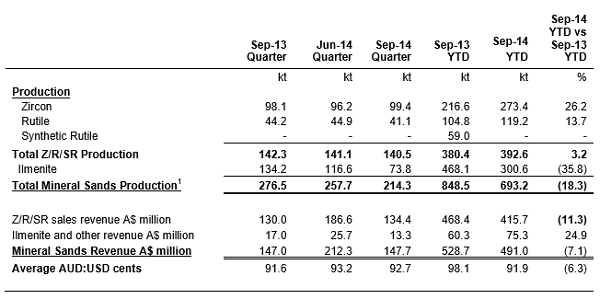

Summary of Physical and Financial Data (Source – Company Reports)

Summary of Physical and Financial Data (Source – Company Reports)

As per the quarterly production report dated 30 September 2014, ILU’s combined production of Z/R/SR in the September quarter was 140.5 thousand tonnes (same as that in September 2013 and June 2014 quarters). The combined Z/R/SR production on a year-to-date basis was 392.6 thousand tonnes which is 3.2% higher than the 380.4 thousand tonnes recorded for corresponding period in 2013. Mineral sands revenue for the three months to 30 September 2014 was $147.7 million which was also similar to the September quarter 2013 result. Revenue on a year-to-date basis was $491.0 million, resulting in a 7.1% dip as compared to the same period in 2013. This indicated a mix variance of product sales year-to-date and lower received prices period on period. The sales revenue also decreased in the September quarter compared with the June quarter owing to the timing of bulk titanium dioxide shipments to customers and seasonally lower iron oxide by-product sales and lower received prices for ilmenite product to China. Zircon revenues in the third quarter were on trend with the previous quarter.

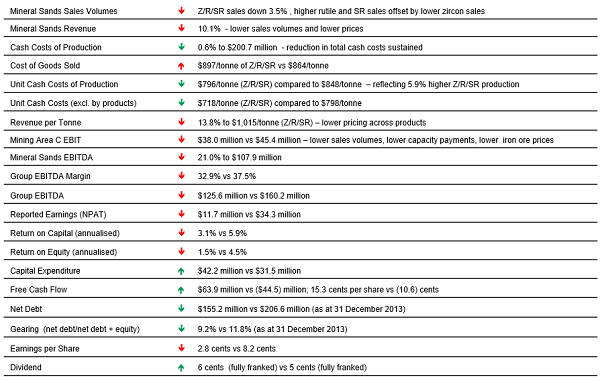

Main Features of 1H 2014 versus 1H 2013 (Source – Company Reports)

Main Features of 1H 2014 versus 1H 2013 (Source – Company Reports)

The quarterly updates also directed that there has been no material change in the revenue per tonne of Z/R/SR sold ($1,015 as reported at 30 June) on a year-to-date basis. This is indicative of the continuation of relatively stable weighted average prices received for zircon and high grade titanium dioxide products. The Company reported that there are no changes to any of its market guidance parameters (as per Feb 2014 ASX Release) and associated commentary about the sales profile for zircon and rutile is unchanged.

The demand for zircon has been stable in 3Q of 2014. ILU reported that an absence of government stimulus measures for the property sector in China during the quarter weighed on sentiment in the ceramics sector as the quarter progressed, with some customers electing to defer September volume into the fourth quarter. The most recent government actions to relax access to mortgages and a lower mortgage rate may have improved housing affordability in China and may help build customer confidence. The expanding zirconium chemicals industry is experiencing a recovery in demand with many Chinese producers operating at capacity and benefiting sales of Iluka’s standard grade zircon. The Asian markets witnessed variable demand patterns with strong zircon sales into Japan following an extended period of low demand. Demand has been robust in the North American market, and is recovering in Europe since the latter part of the June quarter.

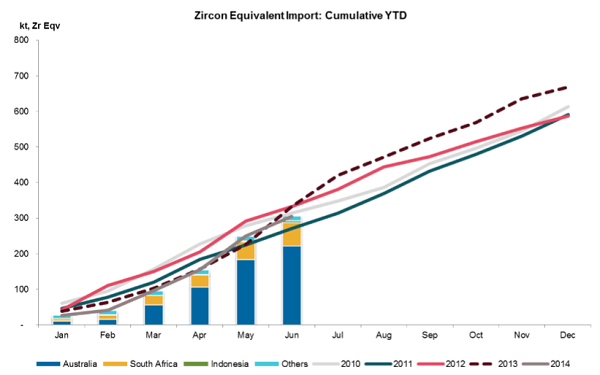

Zircon Imports (Source – Company Reports)

Zircon Imports (Source – Company Reports)

For TIO

2, the conditions for demand recovery in high grade feedstock markets remained the same particularly in the chloride pigment sector. Further, the Company’s high grade ore sales were consistent with expectations while high grade feedstock prices remaining stable throughout the quarter. Although European pigment demand underwent a dip owing to economic slow-down in Germany and the rest of Europe, Iluka’s sales to this market remain unaffected. There has been improvement in the demand for titanium feedstocks to the welding industry, particularly Japan and Korea. ILU’s production settings entailed lower mineral separation plant utilisation than normal to reduce transport and operating costs with progressive drawdown of finished goods inventory.

Mining operations at Jacinth-Ambrosia in South Australia and Woornack, Rownack and Pirro (WRP) in Victoria continued at full utilisation rates. The operations facilitated optimum unit cash cost outcomes for the production of heavy mineral concentrate (HMC). This is planned to entail a build of HMC levels over 2014 and into 2015 to be drawn down following the completion of planned mining in 1H of 2015 and before the commencement of mining at the next planned mine development, for WRP. Mining operation in Western Australia, Tutunup South, remained idled in view of idling of all synthetic rutile kilns in the State, as earlier stated by the Company. The Company is preparing for a possible restart of mining at Tutunup South in January 2015 to produce and stockpile ilmenite in advance of a kiln restart. Mining continued at Brink and mining at Concord is idled as planned. As per the mineral sands production update, processing of final product occurs in Australia at one of two mineral separation plants at Hamilton, Victoria and Narngulu, Western Australia.

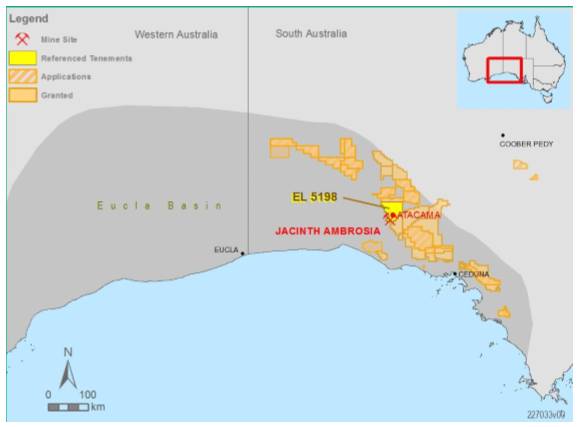

Jacinth-Ambrosia Ore Reserves (Source – Company Reports)

Jacinth-Ambrosia Ore Reserves (Source – Company Reports)

Under the planned new production, Balranald and Nepean were identified as two rutile-rich mineral sands deposits in the northern Murray Basin, New South Wales. Once approved, the Balranald development has been expected to provide the potential for about eight years of rutile, zircon and associated ilmenite products. Work for definitive feasibility study and regulatory approvals is underway with environmental approvals work currently planned for early 2015. In Sri Lanka, the focus was on gaining clarity with the Government in relation to the legal and investment terms for the development of the Puttalam project. Overall, five internal mineral sands projects were reported to be at advanced evaluation stage and two at earlier stage evaluation (Tapira, Sri Lanka).

The Cataby mineral sands deposit, located north of Perth, is expected to produce ilmenite suitable for sale, or as a feed source for synthetic rutile production, and material volumes of zircon and rutile. Scoping study on the Sonoran, Atacama and Typhoon satellite deposits in proximity to the Jacinth-Ambrosia operation in the Eucla Basin is underway with pre-feasibility study scheduled for completion in 2016. The Company announced lately about its decision of not proceeding with the Hickory or Aurelian Springs development projects. The projects were scheduled to extend mining operations beyond the Brink and Concord deposits. The operations will be curtailed by the end of 2015. Though, what is to be thought is about any plans to purchase concentrate from elsewhere to feed ILU’s Stony Creek MSP or to shut-down the plant.

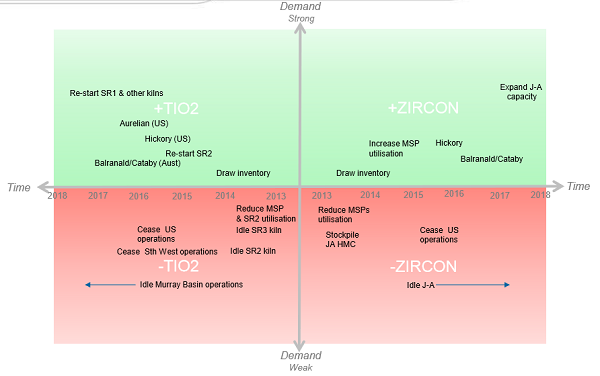

Operations – Options Flexibility (Source – Company Reports)

Operations – Options Flexibility (Source – Company Reports)

The announcement in June 2014 about ILU making a non-binding and conditional share-based proposal to Kenmare for a potential combination of the two companies, is followed by various rounds of discussions and is pending to have a conclusion.

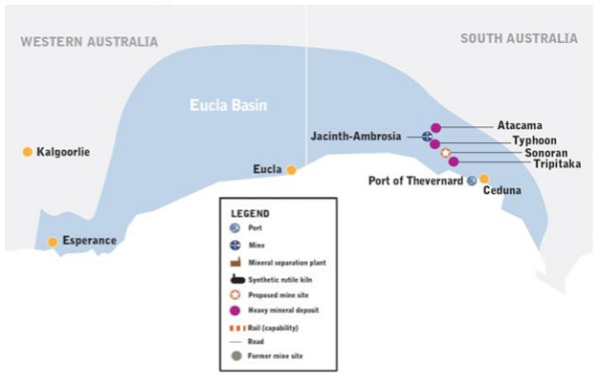

Eucla Basin Tenements and Atacama Drilling (Source – Company Reports)

Eucla Basin Tenements and Atacama Drilling (Source – Company Reports)

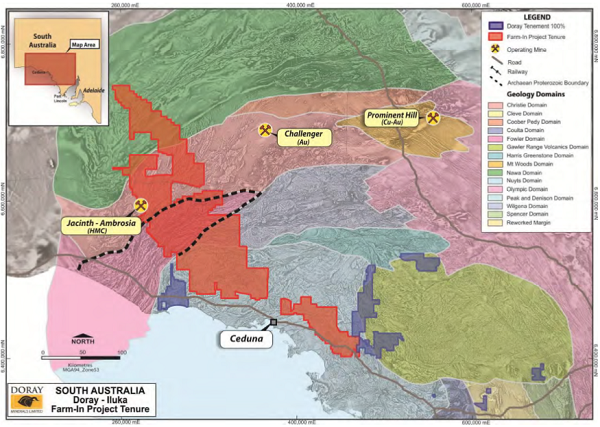

Then, recently Doray signed a gold exploration Farm-in Agreement with Iluka in South Australia. This will allow Doray to have the right to earn up to 80% of any “Gold Resources” discovered within the project area with Iluka retaining rights to discoveries of other commodities made by the Company. The agreement is conditional on the Consent of the South Australian Minister for Mineral Resources and Energy. The Company also has a royalty over iron ore sales revenues from specific tenements of BHP Billiton's Mining Area C (MAC) province in the north west of Western Australia.

Iluka Farm-In Project Area and Existing Doray Tenements in South Australia (Source – Company Reports)

Iluka Farm-In Project Area and Existing Doray Tenements in South Australia (Source – Company Reports)

The tough aspects may entail continued challenges to mineral sands sector flooding into 2015 with soft European pigment demand and increased Chinese pigment exports. Nonetheless, internal efforts including the decision to end US operations by late 2015, DuPont to be the main buyer of ilmenite from Iluka’s US operation, a possible TiO

2 sales volume recovery, and so forth may pay off in the longer run.

ILU Daily Chart (Source - Thomson Reuters)

ILU Daily Chart (Source - Thomson Reuters)

The overall play still looks interesting, and accordingly, we reinstate a

BUY recommendation for this stock at the current price of $5.94.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...