Kalkine has a fully transformed New Avatar.

Company Overview - iCar Asia Limited is an Australia-based company, which is engaged in the development and operation of Internet-based automotive portals in South East Asia. The Company's segments include Malaysia, Indonesia, Thailand and Corporate. It offers a Response Management System (RMS). It brands include Carlist.my and LiveLifeDrive.com in Malaysia; Mobil123.com and Otospirit, in Indonesia, and One2car.com, Autospinn.com and Thaicar.com in Thailand. Carlist.my connects car buyers and sellers to a single platform, which encompasses car classifieds and content. Mobil123.com is an online automotive classifieds Website with over 200,000 listings. Mobil123.com allows both motor vehicle dealers and private sellers to list cars for sale. Autospinn.com is an automotive content Website. The Company's subsidiaries include iCar Asia Pte Ltd, iCar Asia Management Services Sdn Bhd, Netyield Sdn Bhd, iCar Asia Sdn Bhd, PT Mobil Satu Asia, DQBP Sdn Bhd, One2Car Co., Ltd and Perfect Scenery Ventures Limited.

.PNG)

ICQ Details

Growth in top line for 2016 financial performance: iCar Asia Ltd (ASX: ICQ) has reported 6% growth in the revenue year on year (excluding FOREX and passing of Thai King – estimated growth of 12%) in the full year 2016 ended December 31, 2016 but reported NPAT and EBITDA loss. The revenues were impacted by the economic conditions, reduced car sales volumes and horizontal Classified competition. The company costs rose with more people (expansion of Product & Technology and Sales teams) and rise in marketing spend in the second half. On the other hand, ICQ showed positive signs in revenue accelerating into Q4 2016 across all the markets. Additionally, during 2016 the Company had expanded its technology teams in order to put the infrastructure in place to deliver rapid improvement of the user experience for buyers and sellers. The development of a Dealer Mobile App in the fourth quarter of 2017 is expected to enable car dealers to be more engaged with ICQ’s platforms by managing their business and customers using the company’s tools. At the center of this application is a messaging platform that will allow the car buyers and car dealers to connect seamlessly in a WhatsApp-like messaging experience. This would enhance the conversion and the volume of leads, reinforcing the value in the marketplace to car dealers. In addition, in the fourth quarter, the work was also finished in order to bring all countries onto a single technology platform. The technology developments can be more easily and quickly replicated across countries as a single investment can now benefit all markets. The first benefits of this would be seen with product enhancements such as the Dealer Application, Messaging and a re-imagined New Car buying experience able to be rolled out in all markets in rapid succession.

.png)

Financial Performance in fiscal year of 2016 (Source: Company Reports)

Volumes growth: The group reported a 50% year on year (yoy) growth in lead volumes during December 2016 in Indonesia driven by audience engagement rising as their product enhancements have paid off. Moreover, the group’s dealers paying in month to promote their listings also enhanced by 44% in December 2016 as compared to the same period of last year. As a result, their revenues rose 152% on a yoy basis as the market moved into the next phase of monetization. Meanwhile, classified revenues surged 52% in the fourth quarter as compared to the third quarter of 2016 indicating a positive start in 2017 year. As per the Thailand performance, Audience and leads volumes surged 22% and 17%, respectively during December 2016 on a yoy basis. Rising adoption of digital channels drove listings to 11% in December 2016 against pcp. As a result, the revenue rose 12% on a yoy basis, but the group witnessed a better growth in the fourth quarter of 2016 and generated a 22% growth as compared to the third quarter of 2016. With regards to the group’s Malaysia performance, theAudience enhanced 90% on a year on year in December 2016 driven by the ongoing car buyers moving to online, wherein the leads surged 14%. The group’s efforts paid off as the business enhanced 35% on a year on year listings growth while delivered a 26% account growth in December 2016. Meanwhile, the group reported a local currency revenue growth of 2% in 2016, however, they witnessed a better growth in the fourth quarter of 2016 generating a 22% rise as compared to the third quarter of 2016. .png)

Malaysia Performance (Source: Company Reports)

Fund raising and strong cash position: In 2016, ICQ was in a strong cash position. The 2016 cash receipts had improved 20% on the prior year to A$7.45m as collections were tightened and customers bought more prepaid credits to purchase online ‘depth’ products. Moreover, ICQ had also raised capital in the second half of 2016 from an institutional placement. The A$23.00m raised (pre-fees) meant that the company finished the 2016 year with A$27.08m in cash, cash equivalents and term deposits. This will provide ICQ with sufficient resources to execute its expansion plans in 2017. Additionally, ICQ is fully funded and is in an excellent position to capture the enormous opportunity that awaits the largest and most trusted digital automotive marketplace in ASEAN.

Clearly defined strategic priorities: ICQ has clearly defined strategic priorities. Factors such as consumer audience and lead growth through TV marketing to drive App and messaging adoption, used Car Dealer App and pricing restructuring, launch of a revised New Car Dealer and OEM proposition, audience segmentation, and so forth, are expected to drive media sales and revenue growth and expansion into commercial vehicles, motorbikes and parts & accessories.

.png)

Effects owing to Digital Transformation on Auto Industry in next Five Years (Source: Company Reports)

Outlook for the first quarter 2017: In the first quarter of 2017 there would be a number of major product launches. The New Apps will deliver messaging and set the local businesses up for strong growth in leads. There will also be changes to the New Car product in all markets and new technologies will be introduced to make it easier for advertisers to connect to premium segmented audiences on iCar Asia’s sites. Moreover, the first quarter 2017 will also see the launch of the first major Group TV advertising campaigns across all markets which will be part of a fully integrated marketing strategy tailored to each country. This will drive brand awareness, and audience and leads growth in the lead up to the key local automotive buying periods in each geography. Additionally, there will be revamp of Media offering with improved audience segmentation. ICQ will expand proposition into finance, insurance, parts and accessories. The outcome from the quarter will be audience and lead growth, and messaging adoption.

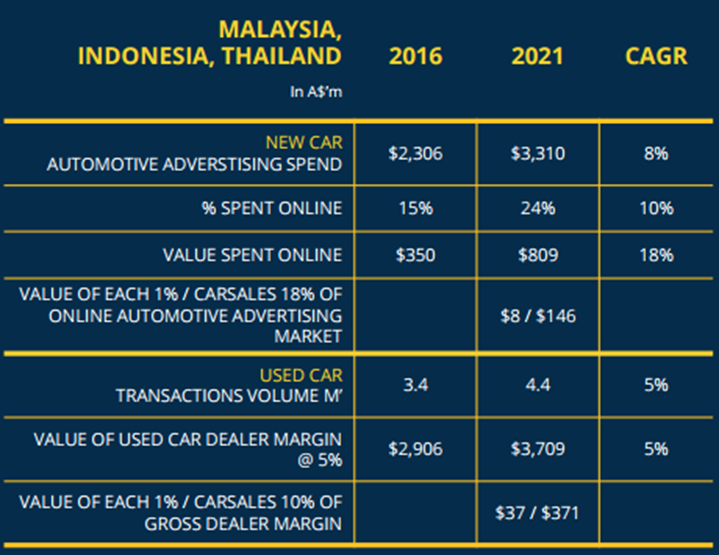

More room for growth in Asia: There are three largest car markets in ASEAN, which are Indonesia, Thailand and Malaysia, that collectively have 359m population, 195m internet users and A$ 2.3 billion addressable new car AD market. The car transactions per annum in these three countries are 2.3 million for the new cars and 3.4 million for the used cars. Moreover, in the new car market, the online share of New Car advertising spend is predicted to increase from 15% to 24% by 2021 (Australia is currently 49% and UK at 52%) as the markets mature. This is expected to generate an addressable online market of circa more than $800m. The Carsales.com.au currently captures 18% of the new car online advertising market. Additionally, the used car market will conservatively generate a margin of $3.7b by 2021. The used car markets will continue to embrace the online marketing channels and the Carsales.com.au currently captures approximately 10% of the used car dealer margin.

Future Potential (Source: Company Reports)

Stock Performance: ICQ stock fell over 15% in the last six months (as of April 03, 2017) given the volatile conditions in the ASEAN Region for Automotive Industry during 2016. The stock also got removed from All Ordinaries Index effective March 20, 2017. The group witnessed a lower than estimated new car sales growth in Malaysia and Thailand while reported a weak overall Indonesia growth. On the other hand, the stock has risen over 10.9% in the last four weeks and this momentum is expected to continue in the coming months (as of April 03, 2017) while there can be short term volatility. The group’s positive fourth quarter of 2016 indicates a potential positive performance in 2017. Moreover, the digital transformation of the automotive industry is growing given the consumer behavior shifting to online channels for the buying and selling of cars. We give a “Buy” recommendation on the stock at the current price of – $ 0.24.png)

ICQ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...