Kalkine has a fully transformed New Avatar.

Company Overview - iCar Asia Limited is an Australia-based company engaged in the development and operation of Internet-based automotive portals, and the advertising, publication and distribution of automotive magazines in South East Asia. The Company operates in the advertising segment. The Company has operations in Malaysia, Thailand and Indonesia. The Company's classified sites include carlist.my, one2Car.com andmobil123.com. The Company's combined audience for its sites includes approximately 5,123,000. The Company also offers a Response Management System (RMS). Carlist.my and mobil123.com offers mobile applications for both iPhone Operating System (iOS) and Android. The Company's subsidiaries include iCar Asia Pte Ltd, Netyield Sdn Bhd, iCar Asia Sdn Bhd, PT Mobil Satu Asia, iCar Asia (Thailand) Limited, DQBP Sdn Bhd, O2C Holdings (Thailand) Co. Ltd, Perfect Scenery Ventures Limited and One2Car Co., Ltd

.JPG)

ICQ Details

Speculation on Carsales.com Ltd.’s consideration of iCar Asia’s takeover bid or stake sell down, being addressed: iCar Asia Ltd (ASX: ICQ) has been confirmed by Carsales.com Ltd that it is not currently considering either a takeover bid or a sell down of its stake in iCar Asia Ltd. Carsales owned 16.5% of ICQ. After this confirmation by Carsales.com Ltd, the speculation from the media is put to an end. Additionally, the speculation had increased more when both directors, Mr Cameron McIntyre and Mr Ajay Bhatia, who were also representatives from Carsales resigned from the board. Mr McIntyre was appointed to the Board of ICQ in April 2013 and Mr Bhatia in November 2014. The speculation has led to heavy selling of the ICQ stock, so after this announcement there has been some sense of relief. ICQ has always been viewed as a logical takeover target for Carsales amid low growth opportunities in its core domestic market.

Third Quarter 2016 Operating Performance: ICQ has been delivering a solid performance and has reported a 15% growth in listings of total vehicles for sale to 53,000 since January 2016 due to the success of the regional expansion strategies in all the markets. There is a 22% growth of audience year on year in Malaysia and 19% growth in Thailand. Moreover, the bump volumes continued to increase month on month due to 260% growth in Indonesia and 14% growth in Thailand since January 2016. Additionally, ICQ in the third quarter 2016 reported a 29% growth of year to date 2016 cash collections to A$5.63m on the prior year. At the end of 30th September, 2016, ICQ had cash and cash equivalents of A$25.90m, including the receipt of A$17.50m raised (pre-fees) from a placement during the period. Another A$5.50 million in connection with the placement was said to be received by the company.

Year to date collections (A$ 000s) (Source: Company Reports)

Raising Capital to strengthen balance sheet: ICQ has successfully raised over $17.5 million via the issue of over 54,687,500 ordinary shares at an issue price of 32 cents per share, which represents an 11.1% discount to the last closing price of ICQ shares on 30th August 2016. The group intends to use these proceeds for organic growth like investing in innovative new product and technology, to increase marketing, to enhance the employee capability and for geographical expansion to accelerate the ICQ’s revenue and future profitability. Moreover, the major shareholder Catcha Group Pte Ltd (which beneficially holds 28.55% of the shares in ICQ) committed $5 million within over two months, on the same price and terms as the placement and subject to shareholder approval at a general meeting of ICQ. Catcha Group will not be entitled to vote on this resolution at the meeting. In addition, non-executive director Syed Khalil Syed Ibrahim has proposed to subscribe for shares in ICQ to the value of $500,000 on the same price and terms as the placement and subject to shareholder approval at the general meeting. Therefore, if the shareholder approval is received, ICQ will able to raise a total of $23 million through the placements.

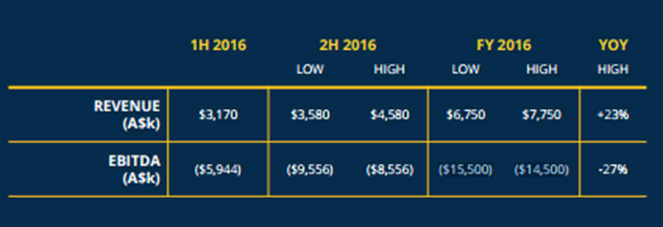

Financial Performance for First half of FY 16: ICQ in the first half of 2016 reported a 20% growth in the revenue mainly through the Media and Classifieds in Malaysia and Thailand. However, the revenues were impacted by economic conditions, reduced car sales volumes and horizontal classified competition. Moreover, the EBITDA enhanced year over year in all the markets. Additionally, ICQ expects the revenue in FY 16 to be in the range of A$6.75m to A$7.75m which is an increase of 23% on a year over year basis. But the group forecasted an EBITDA loss in the range of A$14.50m to A$15.50m. This guidance is manly on the back of the group’s heavy investments in consolidating their target market position, while volatile macro conditions in Malaysia, Thailand and Indonesia have hurt the regional performances. Currency fluctuations also hurt volumes of used car imports. Therefore, ICQ invested in digital marketing across all platforms and in their private seller experience on desktop and mobile. The group also enhanced Consumer App for boosting their position in each market.

Financial Performance for FY 16 (Source: Company Reports)

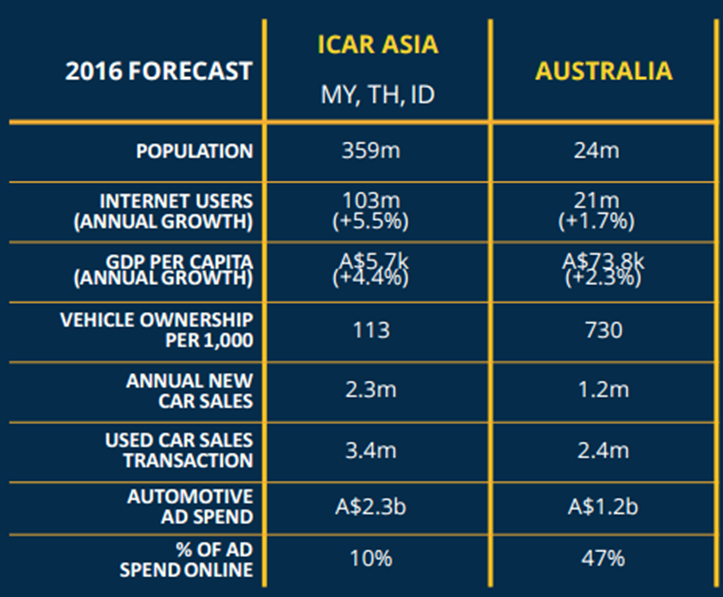

Market Opportunity with rising demand: ICQ is now targeting the developing markets with large populations and high GDP growth. The vehicle ownership is expected to accelerate as consumer purchasing power is growing (tipping point: US$5,000 GDP per capita). Moreover, the new car sales volumes have already exceeded the established markets such as Australia. From Malaysia, Thailand and Indonesia, ICQ gets over 1 million car transactions per year per country. Therefore, ICQ’s markets offer huge potential for long-term growth in car transactions and as a result revenue for the technology providers like ICQ would further facilitate buyer/seller interactions. Additionally, ICQ intends to strengthen its position by increasing its investment in the second half of 2016 in marketing, product, technology and front-line sales staff. ICQ would use the investment to grow regionally outside the capital cities and expand the base of car dealer customers. In addition, ICQ’s strategic product developments in the private seller and new car markets space would lead to new revenue streams and growth drivers. ICQ’s dealer application, the revamped consumer mobile experience and messaging functionality are expected to post further improvements in engagement between the customers, and result in more cars being successfully traded through ICQ’s platforms. Meanwhile, management of iCar Asia reiterated their confidence on building customers in the region wherein their marketing efforts are delivering a more engaged car buying audience. The product optimizations enhanced conversion in the third quarter across the group’s major customer flows.

Market opportunity (Source: Company Reports)

Growing online market: The online market is still in the nascent phase and as the markets of the internet market will mature, the new car online advertising share of marketing spend is forecasted to increase from 10% to 28% by 2021 (Australia is currently 47% and UK at 52%). This is expected to generate an addressable online market of circa more than $900m. Carsales.com currently has 18% of the new car online advertising market. Moreover, the used car market will conservatively generate a margin of $3.7b by 2021 as the used car markets will continue to grow through the online marketing channels. At present Carsales.com has approximately 10% of the used car dealer margin.

Stock Performance: iCar Asia stock fell over 72.67% in the last six months (as of November 21, 2016). Speculation from the media have been revolving around the stock regarding for a possible takeover or stake sell from Carsales.com. The group’s EBITDA loss guidance for fiscal year of 2016 also led to the stock pressure. On the other hand, ICQ is readying itself for a more engaged car buying audience, while the product optimizations in the third quarter 2016 and the continued improvements on the product in fourth quarter 2016 across all markets will help build on this momentum going into 2017. The group’s expanding market opportunity in its target markets coupled with rising online audience would drive the performance in the coming months. We believe investors can leverage the heavy correction in the stock given growth prospects. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of – $ 0.23

ICQ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...