Company Overview: iCar Asia Limited is an Australia-based company, which is engaged in the development and operation of Internet-based automotive portals in South East Asia. The Company's segments include Malaysia, Indonesia, Thailand and Corporate. It offers a Response Management System (RMS). It brands include Carlist.my and LiveLifeDrive.com in Malaysia; Mobil123.com and Otospirit, in Indonesia, and One2car.com, Autospinn.com and Thaicar.com in Thailand. Carlist.my connects car buyers and sellers to a single platform, which encompasses car classifieds and content. Mobil123.com is an online automotive classifieds Website with over 200,000 listings. Mobil123.com allows both motor vehicle dealers and private sellers to list cars for sale. Autospinn.com is an automotive content Website. The Company's subsidiaries include iCar Asia Pte Ltd, iCar Asia Management Services Sdn Bhd, Netyield Sdn Bhd, iCar Asia Sdn Bhd, PT Mobil Satu Asia, DQBP Sdn Bhd, One2Car Co., Ltd and Perfect Scenery Ventures Limited.

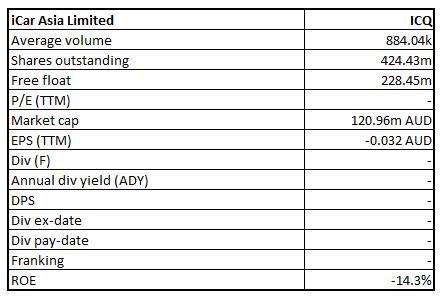

ICQ Details

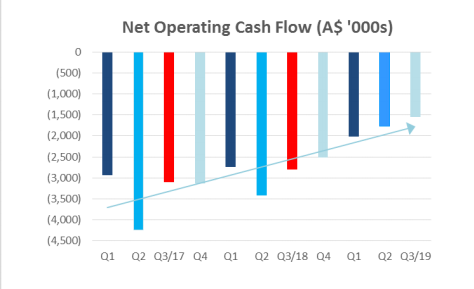

ICQ Improves Operating Cash Flow and Beats Revenue Guidance: iCar Asia Limited (ASX: ICQ) is in the business of development and operation of internet-based automotive portals in South East Asia. The market capitalisation of the company stood at ~$120.96 million as of 05 November 2019. Over the period covering FY14 to FY18, the company has seen an upward trend in the revenue wherein top-line CAGR growth over the said period stood at ~42.4% with FY14 and FY18 revenue amounting to $2.81 million and $11.56 million, respectively. Recently, the company released its Quarterly report for the quarter ended 30 September 2019, in which it marked the fifth consecutive quarter of strong cash outflow improvement. The operating cash outflows of the company improved by 45% year on year to $1.5 million and by 12% against the prior quarter. It was mainly driven by the robust cash receipt growth and lower expenditures. ICQ believes the trends to continue for the rest of 2019 as it progresses to monthly run-rate EBITDA breakeven by the end of 2019. The Group recorded an unaudited revenue of $3.9 million for the third quarter of 2019, which increased by 29% as compared to the same period last year. This result has trounced the growth guidance of 27% and accomplished through continued robust growth in its corebusinesses of used and new car.

The company stated that the cash collections rose by $0.4 million or 13% versus Q3 2018 to $3.6 million for the third quarter. This growth was propelled by strong cash collections in the entire business units involving used car and new car throughout all 3 countries, i.e., Malaysia, Thailand, and Indonesia. The top management stated that the company performed well in all the three quarters of 2019. Also, the company is also enthusiastic about the forthcoming completion of the acquisition of Carmudi Indonesia, which will set it up perfectly for additional growth in Indonesia and throughout the group. During the first half of 2019, the group reported an improvement in EBITDA by 36%, with total visitors of around 10 million per month. During the half-year, the company witnessed a decrease in operating costs from $10.1 million in 1H18 to $8.7 million in 1H19. This was mainly due to a focus on online marketing and completion of the large-scale technology transformation.

The clear synergies which have been identified in 3 core areas of operations as a result of the acquisition of Carmudi Indonesia, maintenance of corporate costs, and decent capabilities to build cash levels are expected to act as tailwinds for the long-term growth.

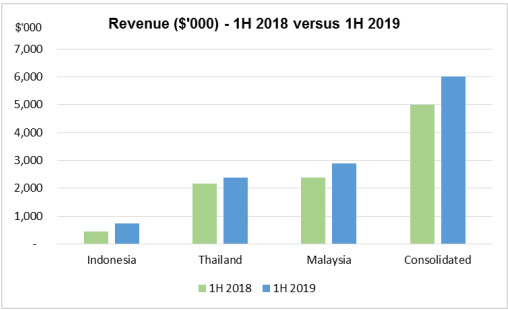

Financial Performance (Source: Company Reports)

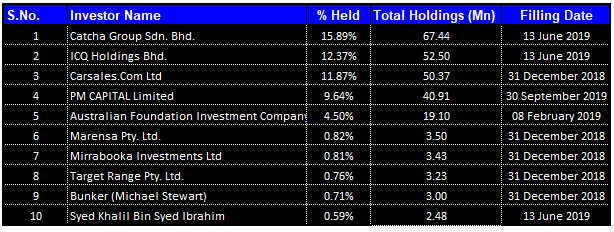

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in iCar Asia Limited:

Top 10 Shareholders (Source: Thomson Reuters)

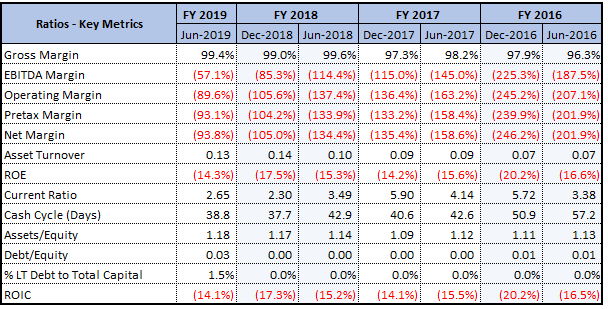

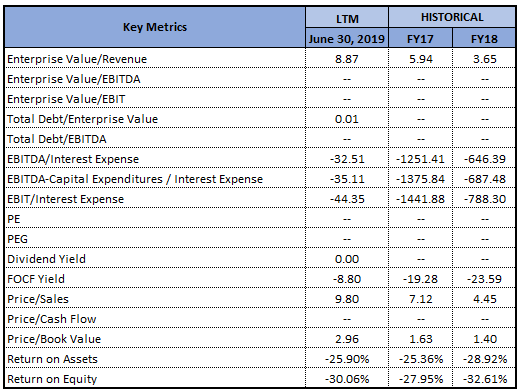

Key Metrics: The company’s key margins have witnessed an improvement in the half-year ended June 2019 on a YoY basis. Notably, the company’s gross margin stood at 99.4%. The company’s current ratio stood at 2.65x, which is higher than the prior corresponding period current ratio of 2.30x, and, therefore, it can be said that ICQ has improved its capabilities to meet its short-term obligations. Also, an improvement in the liquidity levels reflects that it could make deployments towards strategic business activities, which can act as long-term growth drivers. Over the past five years, cash conversion cycle of the company has improved and stood at 37.7 days in 1HFY19, which is lower than the industry median of 38.8 days.

.

Key Metrics (Source: Thomson Reuters)

Acquisition of Carmudi Indonesia: The company announced that it has entered into a binding agreement to acquire Carmudi Indonesia for USD 3 million, which will be paid from cash reserves in two payments, USD 2.0m on completion and USD 1.0m on 15 October 2020. This acquisition will give the company an opportunity to grow its market-leading used car business with Indonesia’s number 2 vertical automotive site (Carmudi.co.id). The combined Indonesian business is anticipated to more than double iCar Asia Indonesian businesses’ revenues as well as increase the growth rates. The synergies are expected to result in combined businesses breaking even in 2020. However, it was stated that the group is on track for EBITDA break-even by the end of 2019.

Decent 1H2019 Results: During the first half of 2019, the group generated revenues of $6.01 million as compared to the revenue of $5.01 million in 1H18, representing a year on year growth of 20%.The balance sheet of the company also improved as a result of the receipt of $7.67 Mn in funds from the exercising of options. The company has access to additional funds in the form of a $5.0 Mn debt facility, which continued to remain undrawn.

Region-Wise Performance: The company has overshadowed the online automotive marketplace in each of its markets in spite of business disturbances triggered by general elections in Thailand and Indonesia. The company stated that Malaysia has been EBITDA and cashflow positive in 1H FY19. The plan to concentrate on listing quality where low quality or sold listings are eliminated from the marketplace resulted in a 16% decline in year on year in listings for June 2019, although the total leads generated remained steady. Thailand too, remained to be EBITDA and cashflow positive in the 1H FY19. Listings showed a rise of 18%, but the account volumes remained at the same levels as the Q4 of 2018. Indonesia has further progressed its monetization in the used car segment, assisting to cut its EBITDA loss by more than half. Listings shrunk by 6% year on year in line with expectations as free listings continue to be constricted. During the first half, revenue showed a decent growth across New and Used Car businesses.

Financial Performance (Source: Company Reports)

Effective Cost Management Might Help in Improving Margins: The company’s operating expenses (excluding depreciation and amortisation) witnessed a fall of 10% in 1H FY 2019 to $9.70 million as compared to 1H FY 2018 figure of $10.74 million. This was witnessed with the help of effective cost management via optimisation of marketing expenses, lower employment and administrative expenses as well as reclassification of lease rental amounting to $0.3 million to depreciation and amortisation expenses following adoption of the new accounting standard AASB 16 Leases.

Used Car-Scaling Up Transactional Auction: Dealerships product was introduced and is to be launched as a part of iCar suite in Q4 as agnostic dealer management system, allowing faster listing, credit purchase and product usage. Agnostic tool will allow listings to be published on several platforms, including dealer websites, Facebook pages, and other marketplaces. Business model of Auction fees are charged to the buyer of the car in the range of 1% to 2.5% of the value of the car of about $200. Malaysia is expanding well, and it is expected that it will continue to increase supply through new inspection centres whereas Thailand and Indonesia are progressing a little slower with a rise projected in 2020.

What to Expect from ICQ Moving Forward: The company is anticipating a surge in the business in the second half of 2019 across both the areas of new car and used car. With one-off factors of the elections and coronations completed, there are anticipations that there would be rise in the new and used car sales and activity in 2H FY19. It believes that the revenue from the new car business will increase owing to increased media activity from new car launches, a ramping up of the new car dealer product and with an additional driver of growth coming from scheduled car events across each of the markets.

The company’s key personnel stated that considering the robust performances throughout all the three markets and flat corporate cost, ICQ has been carrying great momentum into 2H FY19. In the same period, the company is expected to strengthen leadership positions throughout the largest automotive markets in ASEAN Region. The company’s top line has witnessed a CAGR growth of 42.42% in the time span of FY 2014- FY 2018 and, therefore, it can be said that it is possessing respectable capabilities to garner revenues. During the same time span, its gross profit has encountered a CAGR growth of 46.50%.

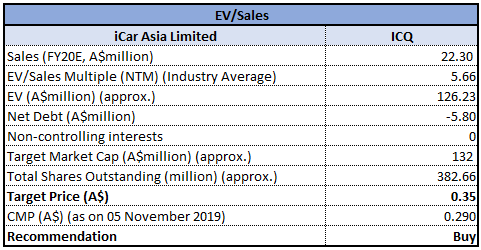

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The company’s stock has witnessed an increase of 42.50% in the time span of the previous three months while, during the span of the previous six months, the stock has increased 23.91%. The operational plans for the company to integrate Carmudi into Indonesian operations have been taking shape, and clear synergies have been identified in 3 core areas of operations. Firstly, new car media and lead generation are anticipated to benefit from the increased audience and data of combined platforms. Secondly, Carmudi’s 5 physical car sales centres, termed as “Carsentros”, would be facilitating a move into transactions and finance commissions that could be leveraged throughout whole iCar Asia Indonesia network. Finally, combined platforms of number 1 and number 2 vertical automotive sites for car dealers in Indonesia would be creating opportunities to cross-promote products, and with roll out iCar Suite this would be the single system for the car dealers to manage listings, leads and credit spend throughout iCar Asia’s multiple platforms. Considering decent capabilities to garner revenues, respectable liquidity levels, and tight cost control, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple, and arrived at a target price of lower double-digit growth (in % term). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.290 per share, up 1.754% as on November 05, 2019.

.png)

ICQ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...