Company Overview: iCar Asia Limited is an Australia-based company, which is engaged in the development and operation of Internet-based automotive portals in South East Asia. The Company's segments include Malaysia, Indonesia, Thailand and Corporate. It offers a Response Management System (RMS). It brands include Carlist.my and LiveLifeDrive.com in Malaysia; Mobil123.com and Otospirit, in Indonesia, and One2car.com, Autospinn.com and Thaicar.com in Thailand. Carlist.my connects car buyers and sellers to a single platform, which encompasses car classifieds and content. Mobil123.com is an online automotive classifieds Website with over 200,000 listings. Mobil123.com allows both motor vehicle dealers and private sellers to list cars for sale. Autospinn.com is an automotive content Website. The Company's subsidiaries include iCar Asia Pte Ltd, iCar Asia Management Services Sdn Bhd, Netyield Sdn Bhd, iCar Asia Sdn Bhd, PT Mobil Satu Asia, DQBP Sdn Bhd, One2Car Co., Ltd and Perfect Scenery Ventures Limited.

.png)

ICQ Details

Double-Digit Revenue Growth in FY18: iCar Asia Limited (ASX: ICQ) is engaged in the business of owning and operating ASEAN’s leading network of the automotive portals. As on May 28, 2019, the market capitalisation of ICQ stood at ~$92.27 million. The company released its full-year earnings report for the period ended 31 December 2018 wherein revenue grew by 27 percent and amounted to $11,555,944 against the prior year. It was mainly driven by Used car growth of 29% and New car growth of 23% during the same period as compared to the prior year. Resultantly, EBITDA losses narrowed by $514k or 4% and amounted to $11,312k in FY18 over the prior year. There are expectations that the company’s events and auction businesses would be contributing more significantly towards growth in 2019. In FY 2018, the company’s operating expenses witnessed the rise of 9% and stood at $22,867,719, primarily because of increased employment cost, with continuing investment towards staff to help the growth of existing and new businesses.

.png)

Operational Metrics (Source: Company Reports)

The company stated that receipts from customers during 2018 witnessed a rise of 46% and stood at $13,688,016 while in FY 2017 it was $9,394,557 and ICQ’s net cash used in operating activities got reduced by 14% and stood at $11,469,810 as compared to $13,392,450 in FY17. The company witnessed 34% YoY growth in the total audience numbers to around 12 million unique visitors per month and, at the same time, there was 12% YoY growth in the average monthly leads. As at 31 December 2018, the company had $9,531,721 in cash, cash equivalents and investments which can be considered at decent levels and can help it in making deployments towards its business activities to support its long-term growth.

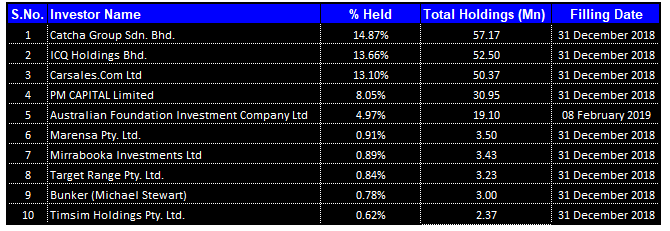

Top 10 Shareholders: The following table gives the broad overview of the top 10 shareholders of iCar Asia Limited:

Top 10 Shareholders (Source: Thomson Reuters)

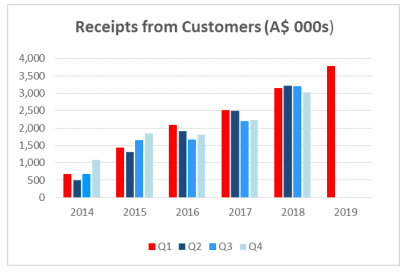

ICQ Witnessed Robust Cash Receipts in Q1 FY 2019: iCar Asia Limited had recently released the results for Q1 FY 2019 which ended in March 2019 in which its cash receipts from the customers stood at A$3.8 million which implies a rise of A$0.8 million or 25% as compared to Q4 FY 2018. This was primarily supported by the robust account renewals in Thailand as well as increased collections from Indonesia’s classified business which introduced paid subscription in September 2018.

Receipts from Customers (Source: Company Reports)

The Malaysia business witnessed a second consecutive quarter of positive EBITDA margin and cashflow while Thailand business had its first quarter of positive EBITDA margin and cashflow. With respect to the Indonesia business, the company stated that it had made further progress in its monetization strategy for Used Car. The continued take up of Used Car subscriptions had resulted in 12% more account in March 2019 as compared to December 2018. The company happens to be on track to reach EBITDA breakeven by 2019 end.

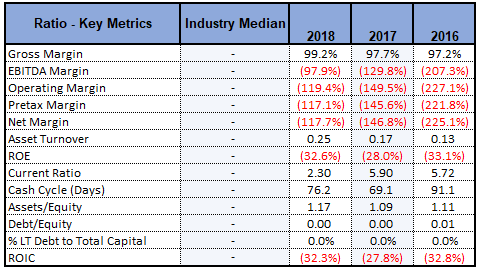

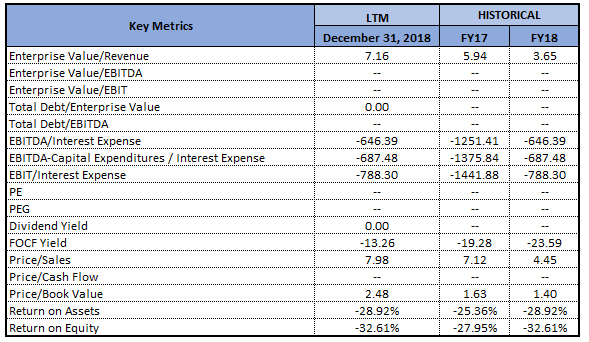

Improving Key Financial Metrics: iCar Asia Limited has witnessed significant improvement in its key financial ratios in FY 2018 on YoY basis, which further strengthens the confidence in the company’s operational activities. Its gross margin stood at 99.2% in FY 2018, reflecting an improvement of 1.5% on the YoY basis. The company’s top line has witnessed the CAGR growth of 42.42% in the time frame of the past five years (FY14-FY18), which reflects the strength in its revenue-generation capabilities. Additionally, there has been decent CAGR growth of 47.3% in the company’s cash receipts during the same period, which might help it in gaining traction among the market players. Moreover, the asset turnover ratio of 0.25x was also above prior year of 0.17x, showing that the company is utilizing its assets in a better way to generate revenue.

Key Metrics (Source: Thomson Reuters)

Malaysia Business Profitable Since September 2018: In the month of September 2018, ICQ’s Malaysia business became EBITDA and cashflow positive, and this trend continued in the December 2018 quarter. The full year EBITDA loss for the Malaysia business witnessed a fall of 77% and stood at $305,780 while in 2017 it was $1,310,773. It was primarily driven by the robust growth in revenues that rose 17% on YoY basis to $5,340,716 in FY18. Besides this, the Used Car-Classified and New Car - Media activities were the primary contributors, and these were complemented by the new revenue streams with respect to Used Car- Auction and New Car – New Car Dealers. The average monthly audience witnessed a rise of 49% on the YoY basis in 2018, which helped in the 41% leads growth as the car buyers were moving online. There are expectations that the robust operational metrics would be helping the growth in the future throughout all the businesses in Malaysia in 2019. As per the May 2019 investor presentation, the Malaysia business witnessed audience growth of 25% on the YoY basis as at March 2019.

.png)

Malaysia Business (Source: Company Reports)

Thailand Audience Grew 27% YoY: The Thailand business witnessed an important financial milestone in 2018 as it became EBITDA and cashflow positive in December 2018. The EBITDA loss for the full year was significantly decreased by 50% and stood at $572,073 from $1,133,116 in 2017. The revenue for year witnessed a rise from $3,818,442 in 2017 to $5,069,584, which reflects 33% YoY growth.

Thailand Business (Source: Company Reports)

The average monthly audience encountered the growth of 27% on YoY basis in 2018. There was continued adoption of the digital channels by the car dealers in 2018 and the number of dealer accounts rose by 20% YoY and the listings growth was 8% YoY. As per May 2019 investor presentation, as at March 2019, the audience decreased by 41% on the YoY basis while, during the same period, the leads fell by 27% YoY.

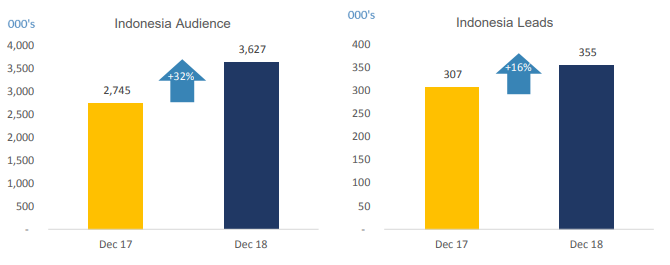

Overview of Indonesia Business: The revenue of Indonesia business witnessed a growth of 58% on the YoY basis and stood at $1,145,644 in FY 2018. During the same period, the average monthly audience and lead volumes witnessed a rise of 32% and 16% on the YoY basis, respectively. In May 2019 investor presentation, it was mentioned that Indonesia business has been ramping up monetization.

Indonesia Business (Source: Company Reports)

What To Expect from ICQ Moving Forward: In Q1 FY 2019, the corporate costs of iCar Asia Limited were flat and were in line with the guidance. The company’s management had reflected favorable views with regards to the performance in Q1 FY 2019, and they also added that it creates a robust base for the company to continue the growth momentum into remainder of the year. In 2019, the company had anticipated to continue to grow core business of the used cars and advertising solutions and also plans to leverage the market leadership positions to further scale up the auction and new car businesses. The company is well-positioned to tap the returns as ASEAN region has been moving on the road of digital transformation.

At the end of Q1 2019, the company had cash and cash equivalents of A$7.3 million, and it also has conditional access to the additional funds of up to A$16.5 million. As per May 2019 investor presentation, the company happens to be on track to positive monthly EBITDA by the end of 2019, and it is expected to be cashflow positive in early 2020.

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: As per May 2019 investor presentation, with respect to used car, there would be a roll out of WeChat Mini Program. Considering the need of the digital channels to grow the business, it can be assumed that this roll out might help the company moving forward. Meanwhile, in the span of previous three months, the company’s stock has delivered an impressive return of 118.18% and, in the span of previous one month, the stock’s return stood at 14.29% which might attract the attention of the market players. Fundamentally, the company seems to be poised for respectable growth in the forthcoming years at the back of improving financials, increasing audience numbers, secured strategic partnerships with dealers, and capital market support and exposure. Talking about Q1 FY 2019, the cash receipts growth and stable expenditure had led to the decline in the net operating cash outflow in the quarter of 20% to A$2.0 million as compared to the previous quarter. The first quarter of FY19 represents the fourth consecutive quarter that witnessed net cash outflow improvements. However, the company is exposed to some of the financial risks like market risk, liquidity and credit risk. Based on aforesaid facts and expectations, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.225 per share (down 6.25% on 28 May 2019 post a rise on 27 May 2019) and expect a double-digit growth in the next one to two years backed by long-term strategic fit and operational initiatives which are underway.

ICQ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...