Kalkine has a fully transformed New Avatar.

Company Overview: HUB24 Limited is a financial services company. The Company is engaged in providing investment and superannuation portfolio administration services, and licensee services. It operates the HUB24 investment and superannuation platform. Its segments include Platform, Licensee and Corporate. The Platform segment is engaged in the development and provision of investment and superannuation platform services to financial advisors, stockbrokers, accountants and their clients. The Licensee Services segment provides financial advice to clients through financial advisors. The Licensee Services segment provides compliance, software, education and business support to advisor practices enabling advisors to provide clients with financial advice over a range of products. The Corporate segment provides corporate services to other segments. Its platform offers a range of investment options for various types of investors, such as individuals, companies, trusts, associations or self-managed super funds.

.png)

HUB Details

Double Digit Growth in Top-line and Bottom-line in 1H FY19: HUB24 Limited (ASX: HUB) is an ASX-listed company which is involved in connecting advisers and their clients via innovative solutions that create opportunities. As on July 16, 2019, the market capitalisation of HUB24 Limited stood at ~$704.32 million. The company released its results for six months ended December 2018 (1H FY19) in which it reported an underlying net profit after tax (or NPAT) amounting to $3.1 million, which reflects a rise of 46% on a Year-on-Year (or YoY) basis, from underlying EBITDA of $6.5 million. The other highlights for 1H FY19 were platform segment revenue which rose 35% on the YoY basis to $25.4 million and platform segment underlying EBITDA which rose 60% on 1H FY18 to $8.0 million. In 1H FY19, the company’s statutory NPAT stood at $3.2 million, which reflects a rise of 39% on a YoY basis. Over the past few years, the company continued to do strategic investment in the business in order to support its growth objective of a targeted figure of $19-23 Bn in terms of funds under administration (or FUA) by 2021. In 1HFY19, the company wrapped up the largest FUA transition, from the leading licensee group to HUB24 platform, which provides evidence of the company’s technology capability as well as expertise in managing the large and complex transitions without disrupting the overall business.

The company stated that its focus revolves around delivering the shareholder returns, improved financial performance as well as superior client outcomes. Additionally, the company added that industry dynamics have been presenting a decent opportunity for HUB24. Post the release of the final recommendations of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, the company is well-positioned to enhance its further growth opportunities.The company inked new agreements with two large national advice groups i.e. Madison Financial Group and Centrepoint Alliance. Moving forward, there are expectations that lower dependency on debt and industry dynamics might support the company’s long-term growth prospects.

.png)

1HFY19 Financial Highlights (Source: Company Reports)

Top 10 Shareholders: The following table gives a broader overview of the top 10 shareholders in HUB24 Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

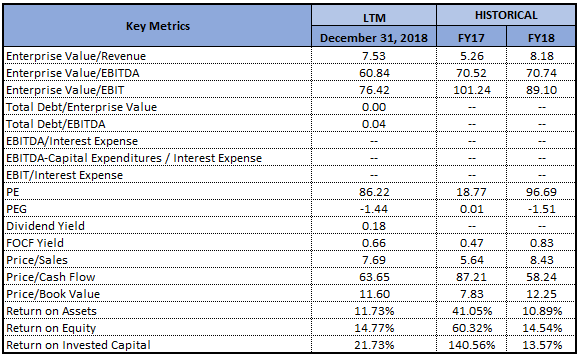

Decent Margins’ Position Strengthens Confidence in Future Prospects: The company had a respectable position with respect to its key margins, which further strengthens the confidence in its expected performance. In 1H FY19, the company’s net margin stood at 6.7%, which implies a rise of 1.1% on a YoY basis, reflecting its improved capability to convert top-line into the bottom line. Additionally, the company’s EBITDA margin in 1H FY19 stood at 11.4%, implying an increase of 1.7% on a YoY basis. Additionally, the company is having respectable liquidity levels as it is evident from the current ratio of 2.76x in 1H FY19, which is comfortably higher than the industry median of 1.50x and, thus, it looks like that the company would be able to meet its short-term obligations. The company’s long-term debt as a percentage to total capital stood at 0.2% which is significantly lower than the industry median of 12% and, therefore, it can be said that the company’s reliance on long-term debt is less as compared to the broader industry. The lower debt on the balance sheet of the company might prove beneficial in the long-term. RoE stood at 5.4% in 1HFY19, which is higher than the industry median of 2.5%.

.png)

Key Metrics (Source: Thomson Reuters)

Addition to S&P/ASX 200 Index: S&P Dow Jones Indices announced the changes with regards to S&P/ASX indices, which became effective at the open of trading on March 18, 2019. In the release, it was mentioned that HUB24 Limited has been added to S&P/ASX 200 Index.

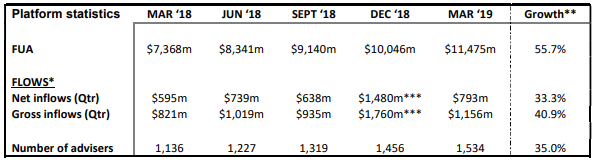

HUB’s March Quarter Witnessed $1.2 billion of Gross Inflows: In the quarter ended March 2019, the company witnessed net inflows amounting to $793 million, which reflects a rise of 33.3% on pcp basis while, during the same period, its gross inflows amounted to $1.2 billion. The company’s funds under administration (or FUA) stood at $11.5 billion as at March 31, 2019, which reflects a rise of 55.7% as compared to March 2018.

HUB24 business development activity secured the new relationships in the quarter ended March 2019 and strength of the pipeline reflects further growth opportunities. During the quarter, the company signed 19 new agreements which include new arrangements for the two significant nation-wide licensees. The company added that the platform investment menu has been expanding with the addition of 17 new managed portfolios during March 2019 quarter including the both diversified as well as Australian equity portfolios.

Platform Statistics (Source: Company Reports)

Comments on Article Published by Australian Financial Review: In the release dated July 3, 2019, HUB24 Limited commented on the article which was published in Australian Financial Review which had numerous statements regarding HUB24 that were incorrect and need to be clarified, as per HUB. The company added that it maintains the flexible fee arrangements with licensees for their clients. The fee example which has been referenced in the article is not representative of administration fees paid as well as interest rates received for the majority of the clients.

The company’s cash account happens to be a working transaction account, which facilitates comprehensive capabilities that support the range of services which are provided to the clients of the platform, such as portfolio rebalancing, investment trading, and pension payments.

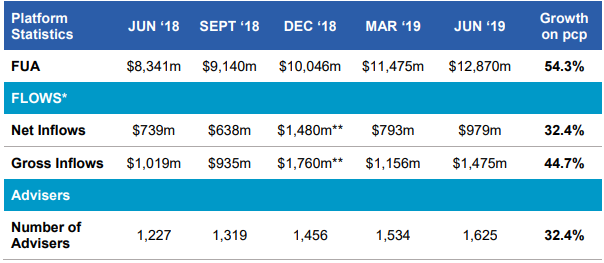

Recorded $12.9 Bn FUA as on June 2019: In the quarter ended June 2019, HUB24 witnessed net inflows amounting to $979 million and also wrapped up the financial year with the annual net inflows of $3.9 billion. Over the twelve months to March 31, 2019, the company increased its platform market share from 0.9% to 1.3%. Besides, the company’s Funds under Administration (FUA) were $12.9 billion as of June 30th, 2019, up 54.3% as compared to June 2018.

During the quarter ended June 2019, 91 new advisers started using HUB24 platform and 24 new licensee agreements got signed. In June, the company wrapped up the development of foreign currency capability for the managed portfolios. This indicates the significant enhancement to the company’s market-leading functionality and the investment managers can now improve the portfolio performance by the reduction in foreign exchange costs at the time of transacting international assets in their managed portfolios. Additionally, the interment managers are better able to manage currency risks by holding foreign currency in their portfolio. The company added that advisers using HUB24 platform rose to 1,625 at June 30, 2019, which reflects a rise of 32.4% on pcp basis. The company’s robust business development pipeline might support the future adviser and FUA growth.

Quarterly Statistics (Unaudited) (Source: Company Reports)

What To Expect From HUB: There are expectations that the industry dynamics might support HUB24 moving forward. It was added that demand for the Managed Account solutions is increasing and the company happens to be a market leader. In the analyst pack for half-year ended December 2018, the company stated that it continues to deploy towards business to support the growth ambitions of targeted $19 billion–23 billion FUAby June 2021. The company has been deploying in order to tap the opportunities and build foundations for the future. The additional expenses have been incurred throughout governance, distribution, infrastructure, and service & innovation. It was mentioned that HUB24 platform has been growing at the fastest rate in the industry and it was ranked at 2nd place for quarterly and annual net inflows in the latest available Strategic Insights data.

The company also stated that it is well placed to leverage the enhanced opportunities in a post Royal Commission world, and it can also lead change with the productand service innovation. Additionally, there are expectations that the company might be supported by its respectable liquidity position as well as lesser dependency on debt component.

Key Valuation Metrics (Source: Thomson Reuters)

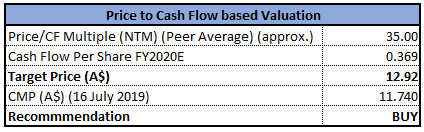

Valuation Methodology: Price to Cash Flow Based Valuation

Price to Cash Flow Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation: HUB24 Limited witnessed a robust CAGR growth in its top line of 42.40% in the time frame from FY15- FY18 which implies that the company is possessing strong capabilities to generate revenues which can act as a growth catalyst for the company moving forward. Additionally, its cash receipts have witnessed the CAGR growth of 44.53% between FY15- FY18 that reflects its strong ability to convert cash. As a result, it can be assumed that the company would be able to maintain respectable liquidity levels moving forward which could further improve its position to make deployments towards the strategic business objectives.

The stock of HUB24 Limited witnessed a fall of 22.44% in the span of the previous three months, while in the time span of the previous one month, the stock fell 14.72%. As per ASX, the stock price of the company is marginally lower than the average of 52-week high and low of $12.70, indicating a decent opportunity for accumulation. Based on the foregoing, we have valued the stock using the relative valuation method, Price/Cash flow multiple, and arrived at the target price of $12.92 (high-single digit upside (%)). Hence, considering the aforesaid facts and current trading level, we give a “Buy” recommendation on the stock at the current market price of A$11.740 per share (up 3.894% on 16 July 2019).

HUB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...