Company Overview: Horizon Oil Limited is engaged in petroleum exploration, development and production. The Company's segments include New Zealand development, New Zealand exploration, China exploration and development, PNG exploration and development, and All other segments. The New Zealand development segment produces crude oil from the Maari/Manaia fields, located offshore New Zealand. The New Zealand exploration segment is involved in the exploration and evaluation of hydrocarbons in the offshore permit area, PEP 51313. The China exploration and development segment is involved in the development and production of crude oil from the Block 22/12-WZ 6-12 and WZ 12-8W oil field development, and the exploration and evaluation of hydrocarbons within Block 22-12. The PNG exploration and development segment is involved in the Stanley condensate/gas development, and the exploration and evaluation of hydrocarbons in over five onshore permit areas, such as PRL 21, PPL 259, PPL 372, PPL 373 and PPL 430.

.jpg)

HZN Details

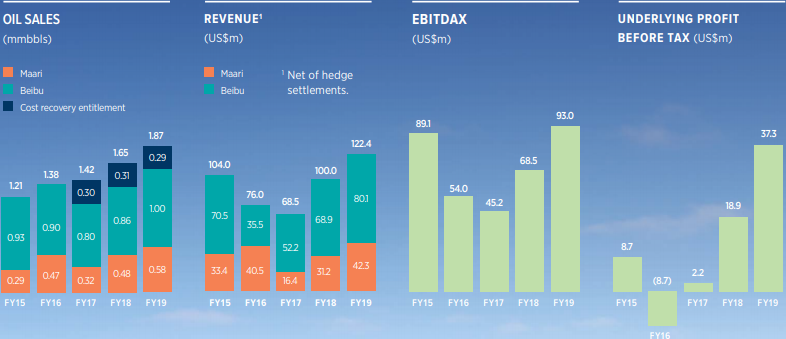

Decent Performance in FY19: Horizon Oil Limited (ASX: HZN) is in the business of petroleum exploration, development and production. The market capitalisation of the company stood at ~$182.28 million as of 1 November 2019. The company declared its 2019 annual results for the year ended 30th June 2019, in which it earned a record sales revenue of US$122 million, up by 22% on FY18, which was mainly driven by record sales volume of 1.87 mmbbls and encountered consistent growth in its sales volumes for 5 consecutive years. The company achieved a solid performance and has met and exceeded core operating, financial and HSSE objectives of 2019. During the year, the company entered into a new US$95 million senior debt facility on substantially improved terms, enabling the consolidation and reduction of debt with funding costs reduced to LIBOR +2.75%.

The company’s strong balance sheet and solid cash flow generation provide increased capacity to identify and secure appropriate expansion opportunities within the focus region to complement HZN’s existing oil production assets. It was also successful in maintaining low operating costs, which led to the record EBITDAX of US$93 million, up by 36% from the prior corresponding period. Horizon expects that they will continue to generate significant cash flow in coming years, and with a progressively improving balance sheet, Horizon Oil Limited is well-positioned for efficient growth in the focus region of Asia Pacific.

The company presented a strong operating performance with an increase of 22% in net production largely driven by active field management and the advantage of a full financial year’s production from the additional 16% interest in Maari/ Manaia, which was acquired in the second half of 2018. This additional underlying production was complemented by increased water injection rates subsequent to the successful conversion of the MR5 well to a water injector in the first half of the year, along with a series of production optimisation activities.

Looking at the past performance, the company delivered a CAGR growth of ~4.2% in revenue over the period of FY15 to FY19, while net profit posted a CAGR growth of ~18.3% during the same period. Revenue from continuing operations improved from US$103.95 Mn in FY15 to US$122.401 Mn in FY19, and net profit improved from US$18.307 Mn in FY15 to US$35.826 Mn in FY19.

The company expects to increase its production at its oil fields in China and New Zealand via optimisation activities, together with infill, appraisal and exploration opportunities conducted in-field or near-field.

5-Year Financial Metric (Source: Company Reports)

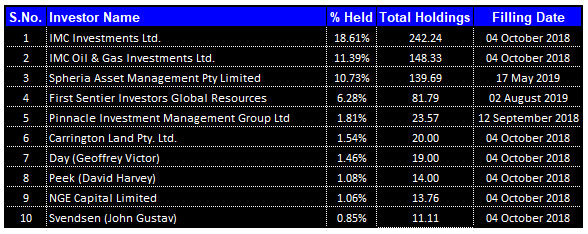

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Horizon Oil Limited:

Top 10 Shareholders (Source: Thomson Reuters)

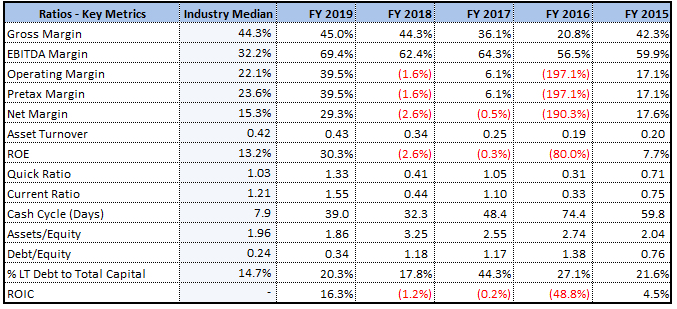

Key Metrics: The company’s key margins for FY19 are higher than the industry median and, therefore, it can be said that it is possessing decent financials. Its net margin stood at 29.3% as compared to the industry median of 15.3% and, therefore, it can be said that HZN is possessing better capabilities to convert its top-line into the bottom-line. Notably, its EBITDA margin stood at 69.4% in FY19 as compared to the industry median of 32.2%. The company’s current ratio stood at 1.55x in FY19, while in FY18, the figure was 0.44x and, thus, it looks like HZN’s ability to meet its short-term obligations have improved. Additionally, the respectable levels of liquidity reflect that it could make deployments towards strategic growth objectives. In FY19, debt/equity ratio came in at 0.34x, which is lower than the prior year D/E of 1.18x, and, therefore, it can be said that HZN has been focusing on deleveraging its balance sheet. Generally, the lower debt on the balance sheet reflects stability and might help a particular company to focus on long-term growth objectives.

Key Metrics (Source: Thomson Reuters)

Quarterly Financial performance: Horizon Oil Limited has had a great start to the 2020 financial year with production for the quarter of 0.4 million barrels, resulting in revenue, inclusive of the hedge settlements, in excess of US$27 million for the quarter. The continued optimisation of producing assets has resulted in the production of 1.2 million barrels for 2019 calendar year to date, an increase of 3.6% on 2018 comparative period. The continued robust cash generation resulted in the reduction in net debt to approximately US$20 million at the end of the quarter. The Group continued to utilize excess cash reserves against the Senior Debt Facility with an additional US$10.0 million voluntary advance payment made during the quarter. The Company is in a good place to achieve its targeted net cash position by mid calendar 2020 subject to the current production and oil prices prevail. Horizon Oil Limited will continue to decrease its debt during the 2020 financial year.

Analysis of 4 Year Gross Profit: The gross profit of the company demonstrated a consistent rise from US$15.7 million in FY16 to US$55.04 million in FY19 and witnessed a CAGR of ~51.68% during the same time span. It looks like the reduction in the cost of sales as a percentage of revenue over the years from 79.23% in FY16 to 55.03% in FY19 has helped the growth in gross profit. The reduction indicates the efficient processes of the company and its ability to expand its business. The following picture can be considered in this regard:

Gross Profit (Source: Company Reports)

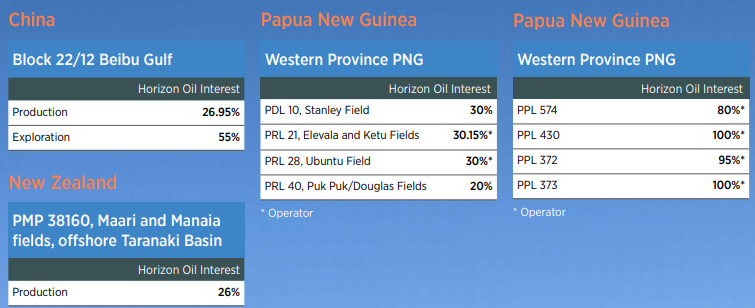

Performance In China, New Zealand and Papua New Guinea: In China, an increase of 10% to 1,290,632 barrels was observed in the group’s crude oil sales from the Beibu Gulf fields at an average price of US$66.31/bbl, exclusive of executed hedging. During the year, there was a 10% increase in oil sales to 1.3 mmbo with a rise in the underlying production by 16%. The operating costs of Beibu Gulf remained below US$10/bbl.

With respect to New Zealand, it was mentioned that the group’s working interest share of production from Maari and Manaia fields was 602,400 barrels of oil. The crude oil sales stood at 575,949 barrels involving an average effective price of US$71.48/bbl, exclusive of executed hedging. This region of the group saw an increase of 33% in production, and cost savings were also implemented, and the improvements in production resulted in lowered production costs to <US$25/bbl. In Papua New Guinea, Horizon Oil Limited progressed planning for the commercialisation of gross appraised resource of 2,200 PJ of sales gas and 64 million barrels of associated condensate in the four petroleum licenses in the foreland basin of Western province.

Region-wise Performance (Source: Company Reports)

Recent Key Updates:

Horizon Advises Spud of WZ 6 12 M1 Exploration Well in China: The company advised that WZ 6?12 M1 exploration well is located in between the Weizhou 6-12 North and South Fields and is targeting the T40-T42 stacked reservoirs. The well objective is to evaluate the structure, sand and oil column thickness in the undeveloped WZ 6?12 Mid Prospect.

Notice Of AGM: 2019 Annual general meeting of Horizon Oil Limited is to be held on November 22nd, 2019 in order to discuss the financial and other reports.

Outlook: The strong production and cash flow in the current year provide a pathway to growth, which might help the overall company in gaining traction among the market participants. The company stated that it would continue to enhance the levels of production at its oil fields in China and New Zealand through the optimisation activities, along with infill, appraisal and exploration opportunities conducted in-field or near-field. These activities would serve to mitigate the natural reservoir decline. There are expectations that the average operating costs might remain below US$20/bbl in the near term, and it would continue the disciplined approach towards capital expenditure.

The company is optimistic about the improved and sustained performance at Maari/ Manaia. The condensate and gas interests in PNG provide an opportunity for the company, and there are expectations that significant developments would take place moving forward around PNG asset base. The company expects that the composition of joint ventures would change in the near future. The company’s strengthened balance sheet and robust cashflow generation provides increasing capacity to identify and secure appropriate growth opportunities within the focus region to complement the existing oil production assets. It was also added that the company would be disciplined in its assessment of opportunities and the execution of any associated transaction.

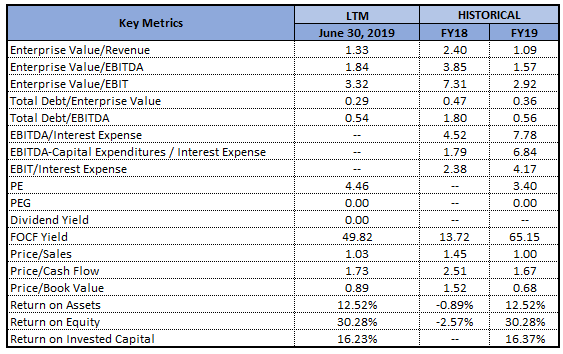

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: The company’s cash receipts have witnessed a CAGR growth of 5.79% in the time span of FY15- FY19 and, therefore, it can be said that HZN is possessing respectable capabilities to build cash levels. During the same time span, HZN’s cash from operating activities saw a CAGR growth of 5.47%, reflecting respectable operational capabilities. There are expectations that its capabilities to carry out operations and build cash levels help in charting out long-term growth. The company is mainly focusing on optimising production performance from the Beibu and Maari/Manaia fields through various production, enhancing well intervention activities in the short-term. In the upcoming AGM, the company might discuss its latest financial performance and give some updates on its recent activities. Currently, the stock is trading slightly above the average of 52-week high and low levels of $0.150 and $0.096, respectively, with a reasonable PE multiple of 2.81x. Hence, in view of aforesaid facts coupled with decent growth potential and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.140 on 1 November 2019.

HZN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...