Company Overview - Horizon Oil Limited is engaged in petroleum exploration, development and production. The Company operates through five segments. The New Zealand development segment is engaged in producing crude oil from the Maari/Manaia fields, located offshore New Zealand. The New Zealand exploration segment is involved in the exploration and evaluation of hydrocarbons in two offshore permit areas: PEP 51313 and PMP 38160 Maari/Manaia. The China exploration and development segment is involved in developing and producing of crude oil from the Block 22/12-WZ 6-12 and WZ 12-8W oil field development, and in the exploration and evaluation of hydrocarbons within Block 22/12. The PNG exploration and development segment is involved in the Stanley condensate/gas development, and the exploration and evaluation of hydrocarbons in five onshore permit areas: PRL 21, PPL 259, PPL 372, PPL 373 and PPL 430. The Company produces over 4,000 barrels of oil per day net from its fields in New Zealand and China.

.png)

HZN Details

Focusing on production to offset ongoing performance pressure: Horizon Oil Ltd (ASX: HZN) reported a revenue decline by 17% yoy to US$20.8 million during first quarter of 2016, as compared to US$25.08 million in fourth quarter of 2015, impacted by ongoing commodity prices pressure coupled with lower production revenue from Block 22/12 (Beibu Gulf) at China. Block 22/12 (Beibu Gulf) Crude oil production and Crude oil sales fell over 12.7% respectively during the first quarter of 2016 against Q415, resulting in a revenue decline of 34% as compared to earlier quarter. Accordingly, Cash as at September ending decreased to US$44.0 million from US$61.3 million in the prior quarter. The group sold oil at an average realized price (including hedging gains) of US$64.70/bbl during the September quarter. On the other hand, Horizon Oil is improving its PMP 38160 (Maari and Manaia), offshore New Zealand production to offset the falling prices pressure to a certain extent. Accordingly, the group delivered a 354,063 bbls production during the quarter, with Crude oil production from PMP 38160 (Maari and Manaia) improving by 15.9% in 1Q16, as compared to the previous quarter. HZN finished Maari growth projects drilling program, and the final well enhanced field production to over 16,000 bopd after starting production on July 2015. Through Horizon Oil’s cost recovery oil entitlement for Block 22/12 China, the group raised over US$97.3 million as at September 2015, with which it is enhancing its production entitlement from the field from 26.95% to over 35% in 2016. Horizon Oil is also boosting its balance sheet by purchasing and cancellation of US$21.2 million of 5.5% convertible bonds which are maturing in mid- 2016. This would decrease the group’s outstanding bonds to US$58.8 million of initial $80 million. Maari mooring and swivel repair insurance claim proceeds from 2013 would generate aggregate net recoveries of US$7.4 million wherein US$4.0 million was to be received in Q2 and Q3 2015 while the rest of the US$3.4 million amount is expected to be received during December quarter.

.png)

First quarter production highlights (Source: Company Reports)

Recent well spud at Weizhou: Horizon Oil recently reported that its WZ 12-8W-A6P1 appraisal well at Beibu Gulf, at China had spudded. The well is situated at the Weizhou 12-8 Fields Area 1.5 km east of the WZ 12-10-2 discovery well that was drilled during 2014 and oil was seen near the T42 sandstone. Meanwhile, the well was drilled to evaluate the structure, sand and oil column thickness in the southeast part of the WZ 12-10-2 structure. The group intends to drill the sidetrack near original discovery location of WZ 12-10-2, based on the results, to offer a horizontal producer that would be able to contribute to the near term incremental production into the present WZ 6-12/12-8W utility platform. HZN is focusing on production and reservoir performance from the WZ 12- 10-2 T42 main sand oil pool before the full-scale field development, which is planned for 2016.

.png)

Block 22/12, Beibu Gulf (Source: Company Reports)

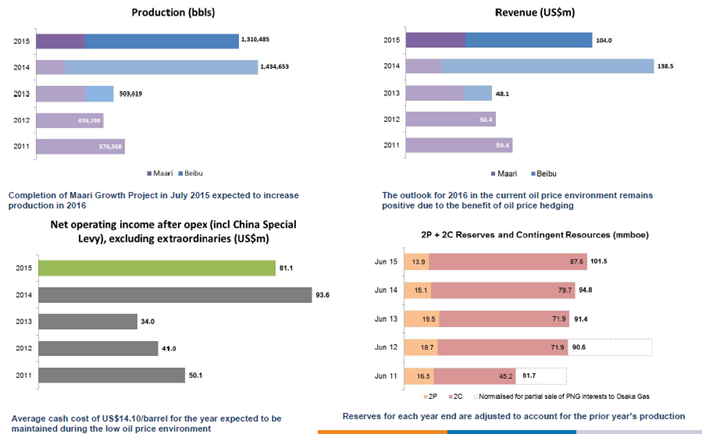

Track record of building solid assets portfolio:Horizon Oil was just an exploration firm with 2 potential development projects around ten years ago. These projects were Maari in New Zealand and Block 22/12 offshore China. The group transformed these assets into production, and enhanced the production and reserves as well as contingent resources for both of these assets by over 120% during the last decade. Accordingly, the group enhanced its revenue by over 75% while net operating income improved by over 60% for both the assets, even though the Brent oil price fell by 50% during that period. The group built a long life of reserves and contingent resources with 101.5 mmboe (liquids 34% / gas 66%), and forecasts a production period for the 30 years. The Reserves and Contingent Resources position is 6.7 mmboe better in FY15 as compared to fiscal year of 2014, on the back of reserves addition in China as well as resource contribution from PNG and China.

Financial performance over the last five years (Source: Company Reports)

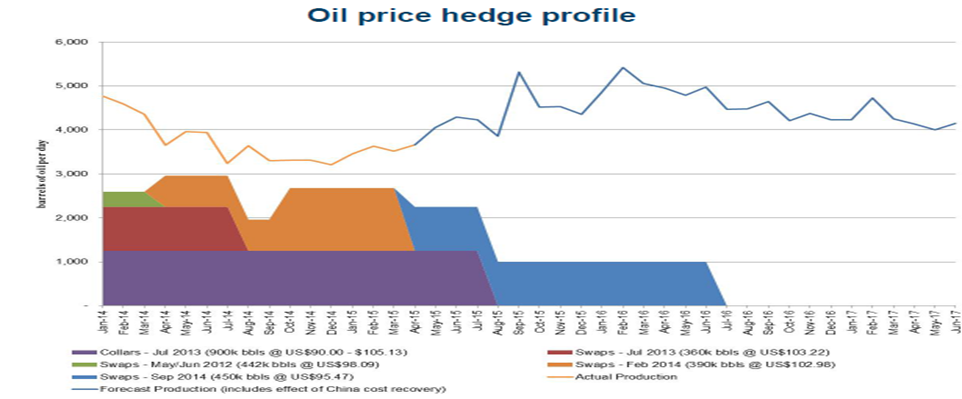

Focusing on operational efficiency: The group is focusing on operational efficiency to partially offset the falling oil prices pressure and accordingly cut its Opex by over 20% during this year to date at Block 22/12. HZN is also decreasing its Capex to less than US$50 million during FY16 (Estimated capex + net G&A). The group is leveraging the cost deflation while developing its new field activities (PDL 10 (Stanley) and PRL 21 (Elevala/Ketu) at PNG and WZ 12-8E and WZ 12-10 Beibu Gulf at China). Meanwhile, HZN hedged 842,500 mmboe during 2015 Jan to mid-2016 at average of US$95/bbl to offset the pricing pressure, which would decrease the falling prices impact on cash flows. Horizon Oil is decreasing its reliance on Oil and focusing on gas sales and consequently building a solid gas production base for the future. On the other hand, Horizon is maintaining a decent balance sheet, with net debt to EBITDA ratio around 2 times.

Oil price hedge profile (Source: Company Reports)

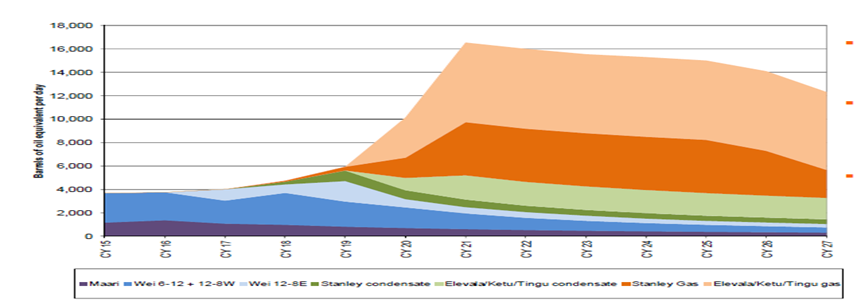

Planned a series of developments and production in the long term: Horizon Oil’s WZ 12-8E, 12-10 and 12-3 fields in Beibu Gulf development might start production from 2017. Stanley condensate start-up gas sales to OTML might start from 2018, while more large scale gas sales are estimated to start from 2020. Condensate monetization coupled with gas sales in PRL 21 might start from 2020. The group expects a better potential of higher oil recovery from WZ 12-8W. Horizon Oil forecasts to generate a cost recovery oil entitlement of US$98 million during 2016 and 2020. The group is also planning to develop a further 17.6 mmboe gross in WZ 12-8E, 12-10 and 12-3 oil accumulations. On the other hand, Horizon oil is focusing on improving its PNG and accordingly the group is expanding its PNG LNG capacity and Papua LNG which might progress to FID by end 2017.

Net production estimates from Reserves and Contingent Resources as of July 2015 (Source: Company Reports)

Stock Performance: The shares of Horizon Oil plunged around 41.4% (as of November 30, 2015) in the last fifty two weeks as falling crude oil prices led to lower average realized prices impacting the group’s revenues. On the other hand, the group is focusing on LNG to decrease its reliance on just oil production. LNG demand is estimated to be decent in the medium to long-term with global contractual supply forecasted to be more than 30 mtpa with short of demand in 2022 while more than 120 mtpa would be short by 2025. The group issued a better outlook in fiscal year of 2016 and intends to decrease the impact of lower oil prices on its operating cash flows. Accordingly, Horizon Oil is cutting its capex by 50% in FY16 and is well positioned to repay its US$80 million Convertible Bond by next year of June. Horizon Oil Beibu Gulf field’s development plan is on track while targeting to achieve a final investment decision for Papua New Guinea Stanley LNG project.

Asset Portfolio (Source: Company Reports)

The group’s hedging contracts would help HZN to maintain a decent average realized prices for oil in the coming periods. Moreover, the shares of Horizon Oil recovered more than 28.1% in the last three months and we believe the group’s stock has the potential to rise further in near future. Investors seeking for long term potential stocks could leverage the recent 14.58% (in the last four weeks) decline in HZN, to enter the stock. The heavy correction in the stock also placed Horizon Oil at very cheaper valuation with a relatively lower P/E of about 5x. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $0.10

HZN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...