Analysis - Horizon Oil Ltd (ASX: HZN) has announced that production from the Maari MR7A development well has come on stream with an provisional initial production rate of between 1500 and 2000 barrels of oil per day (bopd). The optimal production rate will be determined after several weeks of production history after taking into account considerations for reservoir management. The total daily production from the Maari field is around 15,000 bopd. Production started on 18 May 2015 from the Moki Formation reservoir in the field and the well was drilled horizontally to a depth of 4200 m of which roughly 920 m has been completed in the high net-to-gross good quality section. Based on the initial production and the information currently available, the company anticipates the well to meet the pre-drill expectations and contribute significantly to the production from the field.

Asset Portfolio (Source - Company Reports)

The Maari growth project located in offshore Taranaki in New Zealand is being carried out to enhance reservoir production and recovery from the field. The drilling is being carried out by the Ensco 107 rig to establish an additional producer in the Maari field. At a future date, this will be converted to a water injector well to support production and increase recovery from the formation. The participants in the PMP 38160 are 10% Horizon Oil, 5% Cue Taranaki Pty Ltd, 10% Todd Maari Ltd and 69% OMV New Zealand Ltd.

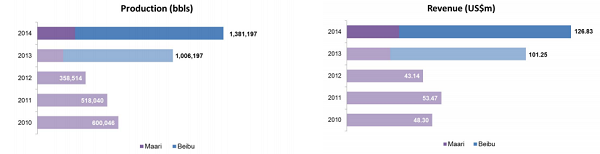

There were several highlights during the quarter. Production gains, including hedging revenues, amounted to US $ 25.7 million, a growth of 8% over the preceding December quarter. Year-to-date 2014/15 financial revenues amounted to US $79 million. Production for the quarter was 324,478 bbls an increase of 6% over the preceding quarter and YTD production is 843,143 mmbo. Despite falling oil prices, strong levels of operating income were reported because of lower operating expenditure down 23% from the preceding quarter and gains from hedging. Capital expenditure was slashed 78% to US $38.2 million in the December quarter to US 8.9 million in the March quarter because of the completion of drilling in China and PNG. The Maari growth projects program is making progress with completion of the MR6A development well and initial production rate of 7800 bopd and development well drilling plan for MR7A.

Production + Revenue (Source - Company Reports)

The company started negotiations in late 2014 with its lenders to renegotiate the terms of its reserve based lending facility (presently drawn to US$110 million.) The key objective was to minimise the extent of amortisation of the facility to 30 June 2016, ( currently US$60 million).During the quarter, the company and ANZ agreed terms for a revised facility. The terms have achieved the objective of doing away with the scheduled debt repayments currently required over at least the next 15 months and, subject to debt capacity criteria, providing for an additional US$50 million accordion feature to accommodate working capital requirements as well as redemption of the US$80 million, 5.5% convertible bonds due in June 2016. The terms of the new revolving cash advance facility provide greater flexibility to the Group The terms of the new revolving cash advance facility provide greater flexibility to the company with improved commercial terms and additional tenor extended to March 2019.ANZ was appointed mandated lead arranger, book runner and structuring bank during the quarter for credit approved commitments for the company's requested US$120 million base facility.

Net Operating Income + Reserves (Source - Company Reports)

Exploration and development capital expenditure for calendar year 2015 has been considerably slashed from the levels of previous years and discretionary expenditure have been minimised across all of the joint ventures in which the company is involved.. The substantial reduction in capital expenditure in comparison with recent quarters reflects the completion of programmed exploration and development drilling in China and PNG with the remaining drilling in respect of the Maari Growth Program scheduled to be completed in mid-2015. The company and its joint venture partners have recognised the need to conserve capital in the current oil price environment. However, budgeted capital expenditure ensures the continuation of planning for important development projects, particularly in China and Papua New Guinea, to progress so that they can benefit from lower costs of development.

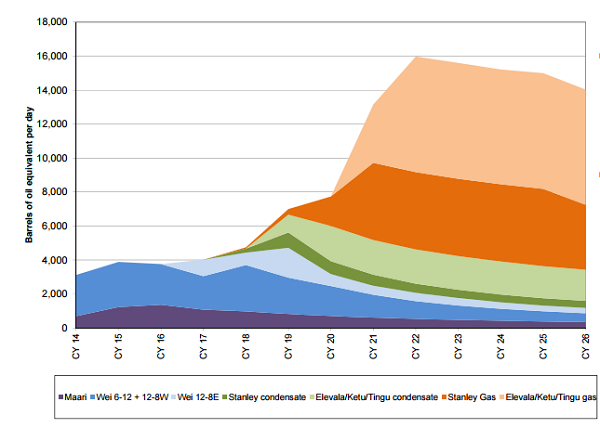

Forecast Production (Source - Company Reports)

After taking into account, the Company’s cash balance of approximately US$40 million at 1 April 2015 and additional undrawn debt capacity of US$10 million under the revised facility, forecast net operating income to June 2016,(inclusive of hedging gains,) in excess of US$110 million (at current oil prices substantially reduced budgeted/forecast capital expenditure profile over the coming 15 months of approximately US$50 million, the potential for additional debt, the company expects to generate substantial cash reserves to meet the redemption obligation under the Company’s US$80 million, 5.5% convertible bonds maturing in the middle of 2016.

Oil Price Hedge Profile (Source - Company Reports)

Revenue for the quarter amounted to US$25.73 million from sales of 327,636 bbls of oil. The average realised prices of oil sold over the quarter, including hedging gains, were US$78.52/bbl.The average cash operating costs were US$15.02/barrel produced during the quarter. The company expects operating costs to be sustained at similar levels through calendar year 2015 based on operators’ budget estimates, with the possibility for further reductions resulting from cost deflation in this low oil price environment.Quarterly net operating income was US$20.85 million.

Production

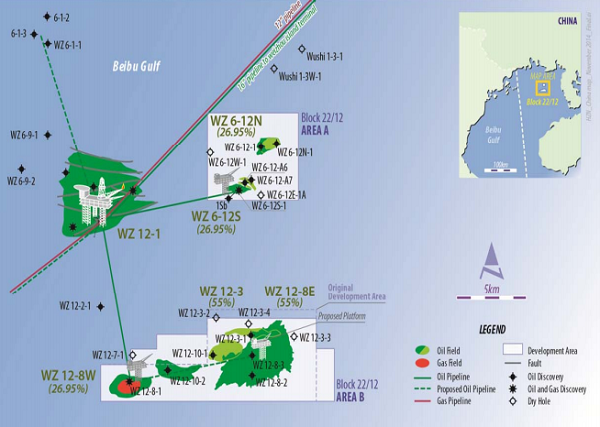

Block 22/12, Beibu Gulf, Offshore China

The company has an interest of 26.95% in the field. Gross oil production averaged 10,533 bopd (HZN: 2,839 bopd) and the 15 production wells are now being provided with artificial lift by electrical submersible pumps. Cumulative oil production from the combined fields at 31 March 2015 exceeded 8.0 mmbo. Evaluation of two successful exploration wells, the WZ 12 -10-1 and WZ 12-10-2 proceeded during the quarter and the planning for a potential appraisal well on WZ 12-10-2 to evaluate the south eastern part of the structure is in progress. If successful, the well will be completed for production and processing will take place through the existing facilities on the WZ 12-8W platform.

Beibu Gulf Field Production (Source - Company Reports)

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...