Kalkine has a fully transformed New Avatar.

Company Overview: Helloworld Travel Limited, formerly Helloworld Limited, is a travel service provider offering retail, wholesale, corporate, inbound and tour operating businesses in Australia, New Zealand, the South Pacific and Asia. The Company is engaged in selling of international and domestic travel products and services, and the operation of a franchised network of travel agents. It operates through three segments: Retail, Wholesale and Travel Management. The Retail segment is engaged in acting as a franchisor of retail travel agency networks, including Helloworld branded Network, Helloworld Associate Network, Helloworld for Business and My Travel Group. The primary purpose of the Wholesale segment is to procure air, cruise and land product for packaging and sale through retail travel networks and other third-party retailers. The Travel Management is engaged in providing travel management services to corporate and government customers, including the booking of flights and accommodation.

.png)

HLO Details

Decent Performance in FY19: Helloworld Travel Limited (ASX: HLO) is a small-cap travel-distribution company with the market capitalisation of $525.07 Mn as of 20 February 2020. In FY19, the company delivered decent growth in TTV, revenue, EBITDA, and net profit as compared to the prior year. It has successfully grown the scale of business in ANZ and benefited from the focus of profitable revenue streams and cost control strategy. During the year, the company continued its significant investment in consumer marketing to increase the Helloworld Travel retail network and expanded its retail networks to 2,447 members as at 30th June 2019, which includes 30 new Helloworld Travel branded agencies throughout ANZ. TTV registered a growth of 9.1% and amounted to $6.5 billion, mainly because of full- year impact of business acquisitions undertaken in 2H FY18 including the Magellan Travel Group, Flight Systems and Asia Escape Holidays and addition of Show Group that was acquired in the month of December 2018.

Revenue increased by 9.8% to $357.6 Mn in FY19 against FY18. It was mainly driven by the inclusion of the business acquisitions and robust trading performance by the Australia and New Zealand retail networks. Revenue margin was maintained at 5.5%, which was in line with the previous year. The margin was helped by the improvement in contracting outcomes and a focus on profitable revenue streams. This was partially offset by changes in the business unit and product revenue mix. Notably, the company’s profit before tax amounted to $54.5 million, reflecting a rise of 21.0% or $9.5 million on YoY basis. Based on FY19 performance, the Board of Directors declared a fully franked final dividend of 12.5 cents per share and it was paid on 17 September 2019 to its shareholders. This summarized a total dividend payment of 20.5 cents per share for the full year, reflecting a rise of 2.5 cents per share or 13.9% on YoY basis. Considering the aforesaid facts, decent fundamentals, paying dividend consistently over the last four consecutive years, completion of TravelEdge Group acquisition, robust business strategy, brand awareness initiatives, and increasing network uptake of preferred products, we have valued the stock using a relative valuation method, i.e., P/E multiple and 3-year average P/E market multiple of ~15.72x to FY20E consensus EPS of $0.357 and arrived at a target price of lower double-digit upside (in percentage term). At CMP of $4.260, the stock of the company is trading at P/E multiple 11.93x of FY20E EPS.

.png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters)

Top 10 Shareholders: The following image provides a broader overview of the top 10 shareholders in Helloworld Travel Limited:.png)

Overview of Margins: The company’s net margin stood at 10.7% in FY19, which reflects an improvement from FY18 figure of 9.5% and, therefore, it can be said that HLO is possessing decent capabilities to convert its top-line into the bottom-line. HLO’s operating margin stood at 15.9% in FY19 as compared to FY18 figure of 14.3%. The company’s RoE stood at 12.7% in FY19 which reflects an improvement from previous year’s figure of 11% and, therefore, it can be said that the company has been delivering decent returns to its shareholders. Current ratio stood at 1.14x in FY19, which is higher than FY18 figure of 1.06x and, thus, it can be said that HLO can be meet its short-term obligations. Also, decent liquidity levels reflect that the company can make deployments towards strategic growth prospects which could help it in achieving long-term growth.

.png)

Key Metrics (Source: Thomson Reuters)

Key Updates Investors Need to Know: Helloworld Travel Limited recently made an announcement about the appointment of Mr David Hall to the designation of the Chief Financial Officer of the company. Mr Hall is possessing a substantial amount of experience throughout the range of industries as well as businesses which includes Qantas, WMC Resources, ANZ Bank and Rio Tinto. HLO also made an announcement that Michael Burnett has stepped down from the role of Company Secretary.

TTV for Q1 FY 2020 rose 10.4% YoY: Helloworld Travel Limited recently gave a business update for the quarter ended September 30, 2019 (or Q1 FY 2020). The company’s TTV for the said period amounted to $1.878 billion, reflecting a rise of 10.4% as compared to the same period of the previous year. However, it was up 9.2% if the impact of business acquisitions, as well as disposals, are excluded. As compared to Q1 FY18, Q1 FY 2020, TTV grew 15.5% over the last two-year period. HLO’s Australian corporate travel management TTV witnessed an increase of 14.3%, which includes an impact of the Show Group Travel acquisition but there was no impact from the TravelEdge acquisition which was wrapped up on 30th September 2019. The company posted unaudited EBITDA for Q1 FY 2020 of $24.7 million, reflecting a rise of 7.7% on pcp and an EBITDA to revenue margin stood at 24.6% as compared to 24.4% for the same period of the last year. The company added that both the periods exclude the impact of a new lease accounting standard. As per the release, The Thomas Cook collapse had zero impact on Helloworld Travel and the company is anticipating to incur net costs related to the collapse of Tempo Holidays and Bentours of under $1.0 Mn.

Wrapping Up of TravelEdge Group Acquisition: Helloworld Travel Limited earlier made an announcement that it has wrapped up the acquisition of the TravelEdge Group. The key personnel of HLO stated that the company looks forward to continuing to provide service to TravelEdge’s corporate, educational institution and leisure clients across ANZ. The release also added that additional expertise and capability brought by TravelEdge would be complimenting Helloworld Travel’s existing corporate operations in ANZ.

Highest Ever Dividend Paid in FY19: The Board of the company declared the final dividend amounting to 12.5 cents per share. This brought the total dividends declared (fully franked) for FY19 to 20.5 cps as compared to 18.0 cps in the previous year. This happens to be the fourth consecutive year the company has declared increased dividend payment. Therefore, it reflects that HLO is possessing decent fundamentals, and it is focusing on delivering returns to the shareholders. The dividend of 20.5 cents per share (fully-franked) is the highest ever, which could attract the attention of the dividend-seeking investors..png)

Dividend on Rise (Source: Company Reports)

What to Expect from HLO Moving Forward: Helloworld Travel Limited earlier gave an EBITDA guidance for FY 2020 in the range of $83 million- $87 million, subject to no significant change in the trading conditions. However, following on from the wrapping up of TravelEdge acquisition, the company has announced a rise in EBITDA guidance, and it is expecting to be in the range of $86 million- $90 million, again subject to no significant change in the trading conditions over the balance of the financial year. Notably, it excludes an impact of the new lease accounting standard.

As mentioned in the company’s annual report, the outlook for the company is decent. The company remains focused on growing its TTV at the profitable margin levels, and at the same time, it plans to carefully control the costs. The company would continue its commitment to focus on strategically growing the business and delivering for the agent networks at the profitable margins. HLO is committed to increase its deployment towards people, brands, products and technology in order to ensure that the business is well-placed to deliver sustainable long-term growth.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

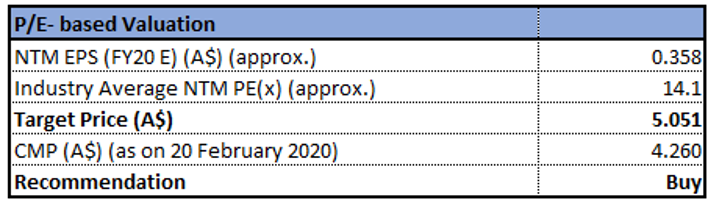

Valuation Methodology: P/E Based Relative Valuation

P/E Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months(20).png)

Historical Price Band (Source: Thomson Reuters)

Stock Recommendation: The company witnessed a CAGR growth of 6.38% between the time span of FY15- FY19 and, therefore, it can be said that HLO is possessing decent capabilities to garner revenues. The Board’s policy revolves around maintaining the robust capital base so that investor, creditor and market confidence can be maintained, and future development of the business can be sustained. The Board monitors return on capital, level of dividends to the ordinary shareholders, cash flow generation and debt to equity mix when it comes to determining an appropriate capital structure. Considering the aforesaid facts, decent fundamentals, paying dividend consistently over the last four consecutive years, completion of TravelEdge Group acquisition, robust business strategy, brand awareness initiatives, and increasing network uptake of preferred products, we have valued the stock using a relative valuation method, i.e., P/E multiple and 3-year average P/E market multiple of ~15.72x to FY20E consensus EPS of $0.357 and arrived at a target price of lower double-digit upside (in percentage term). Hence, we give a “Buy” recommendation on the stock at the current market price of $4.26 (up 1.188% on 20 February 2020).

.png)

HLO Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...