Kalkine has a fully transformed New Avatar.

Company Overview: Healius Ltd, formerly Primary Health Care Limited is a medical center operator. The Company also operates as a provider of diagnostic imaging services; a provider of pathology services, and a provider of health technology. It provides a range of services and facilities to healthcare practitioners, and its medical center operations include the provision of day surgery and in vitro fertilization services by healthcare practitioners. Its segments include Medical Centres, Pathology, Imaging, Health Technology and Other. The Medical Centres division provides services and facilities to general practitioners, specialists and other healthcare providers, and includes Transport Health. The Pathology division provides pathology services. The Imaging division provides imaging and scanning services from standalone imaging sites and from within the consolidated entity's medical centers. The Health Technology division develops, sells and supports health-related software products.

.png)

HLS Details

Healius Limited Rides on Segmental Performance & Structural Redesign: Healius Limited (ASX: HLS) is involved in providing diagnostic and pathology services to consumers and their consulting practitioners, along with facilitating a range of individual healthcare professionals to provide patient care in alliance with Healius’ nurses and support staff. The company has three main businesses – Pathology, Medical Centres and Imaging, along with three evolving businesses Dental, IVF and Day Hospitals.

The company is a top market network leader in Australia with around 2,558 total sites, 2,318 pathology centres, 95 medical centres and day hospitals, along with 145 imaging centres. Pathology remains Healius’ largest division, employing 280 expert pathologists, 2,300 scientists and assistants, and 3,800 collectors. Healius’ medical centre network consists of 73 medical centres, 13 Health & Co practices along with 9 stand-alone day hospitals. The company operates 145 imaging centres, located in medical centres, community centres and hospitals.

.png)

Healius’ Market Leading Network (Source: Company Report)

Total underlying revenue for FY19 (period ended 30 June 2019), was approximately $1,804.5 million, which increased from $1704.6 million reported in FY18. The increasingly positive momentum across all divisions remained a key catalyst. The company reported Underlying EBIT of $167.3 million for FY19, which increased 4.5% year over year. EBIT was impacted by favourable results in all three divisions.

For FY20, the company expects underlying net profit after tax to be greater than FY19, subject to any unexpected market conditions along with any adjustments from the implementation of AASB 16 on leases. The company remains on track to refresh and renew its Medical Centres and invest in leading-edge infrastructure technology and emerging businesses. The company further expects long-term market growth backed by improvements in healthcare technology and cancer endurance rates, favourable population trend and increasing patient expectations.

Looking at the past four-years performance over the period covering FY15 to FY19, the company witnessed a top-line CAGR of ~3.1%. Over the above stated period, the company witnessed constant rise in its largest business, Pathology, along with significant decrease in net debt. The company aims to generate significant cash from operations and maintain a healthy balance sheet. The company remains on track to deliver significant value to its shareholders through continuous payments of dividends, and investment in new and latest technologies. During the year, the company declared a final dividend (fully franked) of 3.4 cents per share.

.png)

Reduction in Net Debt (Source: Company Reports)

FY19 Performance Propelled by Strong Performance in all Three Business Segments: During the period, revenue rose by 5.9% and came in at $1,804.5 million. The company reported underlying EBITDA of $236 million, up from $228 million reported in the year-ago period. EBIT for the period stood at $167.3 million, up 4.5% from $160.1 million reported in the year-ago period. The increase can primarily be attributed to decent growth in Pathology, Medical Centres and Imaging businesses. Underlying NPAT for the period stood at $93.2 million, as compared to $87.5 million reported in the year-ago period. Earnings per share came in at 9.2 cents per share, up from 0.8 cents per share reported in FY18. In FY19, the company declared a final dividend at 3.4 cents per share, with total dividend for the year amounting to 7.2 cents per share.

.png)

FY19 Key Financial Highlights (Source: Company Reports)

Segmental Highlights: Revenue from the Pathology segment came in at $1,128.3 million, an increase of 3.5% from $1,090.6 million reported in FY18. Underlying EBIT rallied sharply in the second half of FY19, skyrocketing 46% as compared to the first half results. Revenue from the Medical Centres division stood at $327.4 million, an increase of 13% year over year, on the back of Montserrat acquisition and revenue growth in Health & Co. By the end of the period, the company recruited 259 General Practitioners (GPs), a 63% increase from FY18. In FY19, revenue from the imaging division increased 7.9% year over year and came in at $391.3 million, primarily due to growth from existing and new sites coupled with continuous potency in MRI. EBIT from the imaging division in FY19 stood at $38.7 million, an increase of 14.5%, that represents a third consecutive year of double-digit growth. Dental revenue in FY19 increased 4.8% year over year and came in at $35.2 million. The division is meeting the growing demand in the community by launching an innovative fixed-price general dentistry.

Balance Sheet Position: At the end of the year, the company reported a cash balance of $119.7 million. The company’s net debt at the end of the year came in at $678.2 million, down from $776.8 million as at 30 June 2018. The company witnessed a significant improvement in leverage since FY15 from the capital recycling program, free cash flow generation and capital raise in 1H19. Furthermore, continuous plans to balance challenging demands and higher strategic investment are key positives. Gearing ratio for FY19 stood at 24.8%.

.png)

Debt Details (Source: Company Reports)

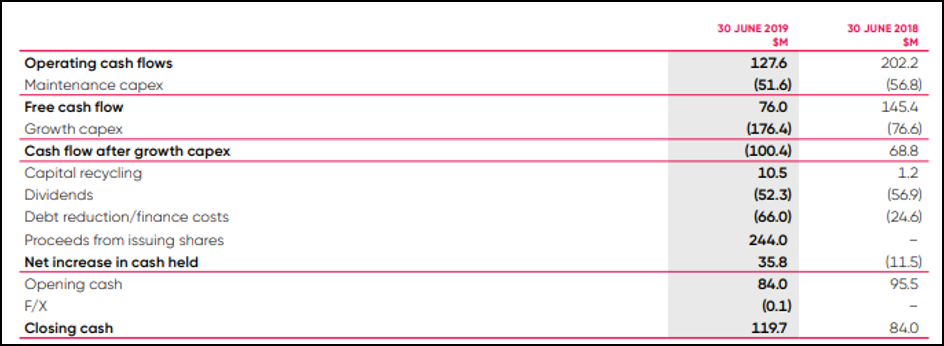

Cash Flow Highlights: In FY19, the company’s operating cash inflow stood at $127.6 million as compared to $202.2 million in FY18. Net cash outflow from investing activities came in at $217.5 million, up from $132.2 million in FY18. Net cash provided by financing activities amounted to $125.7 million in FY19 as compared to an outflow of $81.5 million in the previous year. Maintenance capital expenditure for the period came in $51.6 million. Whereas, growth capex stood at $176.4 million, representing payments made for Montserrat Day Hospitals acquisition, strategic projects along with platforms in Pathology and Imaging.

Cash Flow Details (Source: Company Reports)

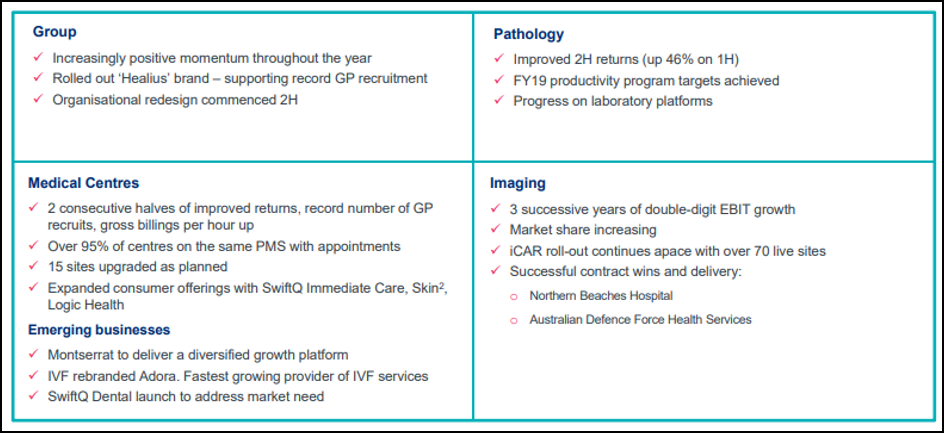

Key Growth Strategies: The company witnessed increasing positive momentum throughout FY19. It rolled out the ‘Healius’ brand supporting record GP recruitment, attained the productivity program targets in the pathology division and advanced on laboratory platforms. In 2HFY19, the company initiated an organizational revamp to improve its productivity and better serve its patients. Coming to medical centres, the company experienced improved returns for two successive halves and upgraded 15 sites as per its plan and expanded customers’ offerings with SwiftQ Immediate Care, Skin2 and Logic Health. The Imaging division witnessed three consecutive years of double-digit EBIT growth. With the above scenario in place, the company is confident about retaining its existing customer base and expects to maintain a dominant growth momentum in FY20.

Key accomplishments with a Strong Run-Rate into FY2020 (Source: Company reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 40.22% of the total shareholding. Jangho Group Co Ltd is the entity holding maximum shares in the company at 15.91%. Dimensional Fund Advisors, L.P. is the second-largest shareholder, with a holding of 5.5%.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

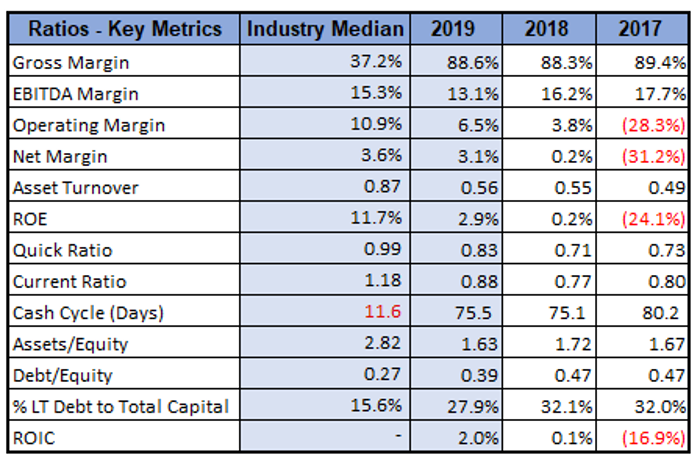

Key Metrics: In FY19, the company had a gross margin of 88.6%, which was higher than the industry median of 37.2%. Gross margin was also higher than the margin of FY18, representing decent fundamentals. Debt-to-equity ratio for the year stood at a decent level of 0.39x, lower than 0.47x reported in FY18, indicating sound financial position.

Key Metrics (Source: Thomson Reuters)

Outlook: Higher investments in healthcare technologies and utilizing the capability of big data by the industry participants to successfully test methods, uncover trends and provide data and information to aid their doctors and clinicians to improve the quality of care are key positives for the company. This is likely to lead to cost productivity, along with higher patient admissions, thus supporting both the top line and margins.

Over the past few years, the industry has started consolidating through mergers and acquisitions mainly due to the difficulties of healthcare reforms. The move has aided the players in establishing operational efficiencies, and financial value for their business. Several deals have assisted the industry to effectively handle costs and enhance productivity, thus leading to economies of scale. HLS is taking essential measures to progress on laboratory platforms in the coming years, which will ultimately impact the company’s long-term growth and profit margins.

For FY20, the company anticipates underlying net profit after tax to be in the ambit of $94 million - $102 million, before any changes from the application of AASB 16 on leases and subject to any unforeseen circumstances. At the top end of the guidance range, growth on the previous year will be ~9.4%. Furthermore, we believe that the extension of the strong operating conditions in Pathology is likely to be the most vital factor in the positive delivery of the prediction. Also, the strategic proposals and structural changes undertaken by the company are expected to provide a business differentiated by clinical quality, customer-friendly access, and cost-effectiveness. This, in turn, is expected to support customer well-being along with the prevention of severe illness with initial intervention. Additionally, the company has a strong FY20 pipeline with M&A and BaU roll-ins in the medical centre segment.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies-

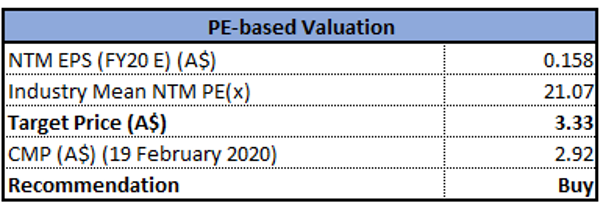

Method 1: Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Method 2: EV/EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated positive returns of ~4.4% on a year to date basis. In FY19, the company delivered a stellar result, driven by positive contributions from all three divisions and expects to thrive further on the back of population trends and increasing patient expectations. From the analysis standpoint, the company has recorded revenue CAGR of 3.1% over the last four years. Notably, the company is expected to report its 1HFY20 results on February 25, 2020. Considering the above factors, we have valued the stock using two relative valuation methods, i.e., Price to Earnings and EV/EBITDA multiples, and have arrived at a target price offering an upside of lower double-digit (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.92, up 1.389% on 19th February 2020.

.png)

HLS Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...