Company Overview: GUD Holdings Limited manufactures, imports, distributes and sale of automotive with operations in Australia, New Zealand, France and Spain. The Company's segments include Automotive and Davey. The Automotive segment provides automotive and heavy-duty filters for cars, trucks, fuel pumps, gaskets, gasket kits and associated products for the automotive after-market. The Davey segment includes pumps and pressure systems for household and farm water, water transfer pumps, swimming pool products, spa bath controllers, and pumps and water purification equipment.

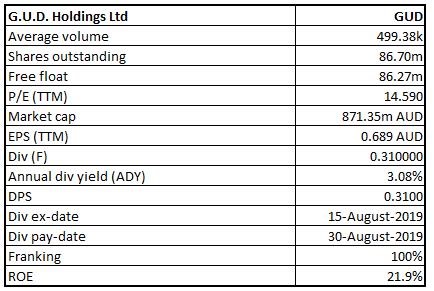

GUD Details

Decent Performance in FY19: G.U.D. Holdings Limited (ASX: GUD) focuses on two main activities, i.e., automotive aftermarket and water products, with its key geographic markets being Australia and New Zealand. As on September 26, 2019, the market capitalisation of GUD stood at ~A$871.35 million. The company released its results for the year ended June 2019 in which its revenue amounted to A$434 million, which reflects a YoY growth of 9%. The company’s NPAT from continuing operations amounted to A$60 million in FY19, implying an increase of 18% on a YoY basis. The company has managed to deliver robust automotive result in a challenging environment. GUD’s cash conversion has witnessed an improvement which is in line with H1 FY19 projections and FY19 target. It was added that the working capital would be providing continued support for the growth in sales. The company also announced a fully-franked final dividend of 31 cents per share, which reflects an increase of 11% on a YoY basis. Resultantly, the full year-dividend increased and stood at 56 cents, fully franked, an increase from 52 cents previously, showing a dividend pay-out of 80% on underlying basic earnings per share from continuing operations and a rise of 8% on Y-o-Y basis. The company’s net debt witnessed a rise to $132.7 million from $92.4 million after the acquisition of Disc Brakes Australia, an earn-out payment for IM Group with regards to its FY18 performance, a further investment towards Liftango, and a rise in the net working capital in 1H FY19. With respect to the outlook, the company happens to be well-placed for medium to long term horizon. In 2019-20, the company expects further revenue and EBIT growth in automotive and water businesses, although the economic sentiment and recent demand suggest that the growth would be modest.

Hence, considering the balanced approach towards capital allocation coupled with decent operational capabilities, robust balance sheet position and paying dividend regularly to its shareholders, we have valued the stock using four year average P/E market multiples of 16.27x for FY20E with consensus EPS of $0.678 and have arrived at a target price upside of lower double-digit growth (in percentage terms). At CMP of $10.03, the stock of the company is trading at P/E multiple 14.79x of FY20E EPS.

.png)

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

Overview of GUD’s Key Margins: The company’s net margin stood at 13.7% in FY19, which reflects an increase from FY18 figure of 12.7% and, therefore, it looks like the company has improved its capabilities to convert its top-line into the bottom-line. In FY19, GUD’s gross margin stood at 48.8% in FY19, which is higher than the industry median of 37.8%. The company’s RoE stood at 21.9% in FY19 that is marginally higher than the FY18 figure of 21.7% and, thus, it can be said that the company has been delivering decent returns to its shareholders. The company’s current ratio stood at 2.91x in FY19, which is higher than the industry median of 1.43x and, thus, it can be said that GUD could meet its short-term obligations in an effective way. Additionally, it looks like that decent liquidity standing might help it in making deployments towards the core business activities moving forward, which could help it in achieving long-term growth.

.png)

Key Metrics (Source: Thomson Reuters)

Top 10 Shareholders: The following table provides an idea of the top 10 shareholders in GUD:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Key Takeaways from GUD’s Annual Review: The company’s key personnel stated that its balance sheet remains robust with a debt increase reflecting in part the purchase of DBA at the beginning of the 2019 financial year. It was further stated that the balance sheet position supports further acquisitions with respect to the automotive aftermarket, where GUD’s appetite is still robust. The company’s net working capital as at June 30, 2019 rose $30.4 million over the prior-year levels of which $7.9 million relates to net working capital acquired through Disc Brakes Australia acquisition. With respect to external financing, the company is four years into a 5-year debt financing facility amounting to $245 million, which involves Westpac, National Australia Bank as well as Commonwealth Bank which expires on July 1, 2020. It comprises the core tranche amounting to $185 million and an acquisition tranche of $60 million. The facility gives capacity for the logical bolt-on acquisitions through a balance of financing facility. The company would be commencing refinancing exercise during the first quarter of 2019-20 and anticipate the commercially favourable outcome.

.png)

Key Metrics (Source: Company Reports)

Sales Growth of 12% in Automotive Business: The Automotive business of GUD reported sales growth of 12%, that consisted of the organic growth of 1% while the balance was from acquired businesses involving additional 5 months’ contribution from the AA Gaskets and full 12 months from the Disc Brakes Australia. Disc Brakes Australia was acquired on July 2, 2018 and wrapped up the year well ahead of the anticipations with double-digit growth in domestic and export sales.

.png)

Automotive (Source: Company Reports)

Understanding Performance of Davey Business: The company’s Davey business reported a 3% rise in the full-year sales to $104 million, and there was a sales growth in all the regions. The full-year underlying EBIT of the business rose by 3% and stood at $9.4 million as compared to $9.2 million in the previous corresponding period, even though the resources were committed towards innovation as well as product cycle plan efforts. This business is continuing to focus on business fundamentals, which includes operational effectiveness, design for the manufacture and supply chain efficiency, product innovation, refreshing existing products, as well as commercialisation of Modular Water Treatment technology.

.png)

Davey (Source: Company Reports)

Increase in Dividends Reflect Decent Position: The total dividend for 2018-19 amounted to 56 cents per share, which consists of interim dividend amounting to 25 cents per share and final dividend of 31 cents per share. Notably, both the dividends are fully franked. When compared with the total dividends of 52 cents per share in the prior financial year, it implies a rise of 8%. The full-year dividend reflected a pay-out ratio of 80% on the underlying basic EPS from continuing operations.

.png)

Per Share Performance (Source: Company Reports)

Robust Balance Sheet Position: The company added that its balance sheet was robust with the gearing, being net debt against net debt and equity, of around 32%, robust interest cover and available banking lines well in excess of $80 million, which could support the bolt-on acquisitions in future. GUD is possessing robust balance sheet metrics which includes net debt/ Underlying (UL) EBITDA (continuing operations) of approximately 2 times, and UL EBITDA interest cover stood at around 13 times. The following image provides an idea of the gearing ratios:

.png)

Gearing Ratios (Source: Company Reports)

What To Expect From GUD Moving Forward: As mentioned earlier, the company is well-placed for medium to long-term horizon. The automotive business is maintaining robust brands, products and customer service in support of the large and proliferated Car parc, which the company believes is strongly defensible. In 2019/20, the company expects further revenue growth in automotive and water businesses, even though the economic sentiment and recent demand suggest that there would be modest growth.

The company would not be reducing its innovation, new product development or acquisition activity in order to compensate, as it remains committed towards ensuring that it has right mid-term foundations in place for the growth over long-term and shareholder value. It stated that FY20 is anticipated to focus on medium-term value rather than the short-term EBIT growth, and there are expectations to intensify the focus towards business-wide operating efficiency. In FY20, the cash conversion is anticipated to remain near 80%. The company has planned an investor day for October 1, 2019.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

.png)

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: On a YTD basis, the stock of GUD has witnessed a fall of 11.14% while, in the time frame of six months, it has fallen 17.08%. As per ASX, the stock is currently trading slightly below the average of 52 week-high and low levels of $14.85 and $8.43, respectively, indicating a decent opportunity for accumulation. The company’s cash from operating activities has witnessed a CAGR growth of 10.23% in the time span of FY15- FY19 and can be considered at decent levels. The company’s top-line has witnessed a CAGR growth of 1.98% between FY16- FY19.

It can be said that the company’s respectable operational capabilities might help the overall company to achieve growth in the long run, which could help it in gaining traction among the market players. However, the company’s net income has encountered a CAGR growth of 15.75% between FY15- FY19, which can be considered at decent levels. Hence, considering the balanced approach towards capital allocation coupled with decent operational capabilities, robust balance sheet and paying dividend regularly to its shareholders, we have valued the stock using four year average P/E market multiples of 16.27x for FY20E with consensus EPS of $0.678 and have arrived at a target price upside of lower double-digit growth (in percentage terms). Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of A$10.030 per share (down 0.199% on 26 September 2019).

.png)

GUD Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...