Kalkine has a fully transformed New Avatar.

Company Overview: GPT Group (ASX: GPT) is an owner and manager of a diversified portfolio of high-quality Australian retail, office, and logistics property assets. The company was listed on ASX in 1971 and since then it has established itself as one of the leading diversified listed property groups. The company’s portfolio includes some of Australia’s most prominent real estate assets, including Melbourne Central and Highpoint Shopping Centre in Melbourne, Darling Park and 2 Park Street in Sydney, Australia Square, Governor Phillip Tower and Governor Macquarie Tower..png)

GPT Details

.png)

Continuous Growth in FFO Per Security: GPT Group (ASX: GPT) is one of Australia’s largest diversified listed property groups with a market capitalization of around $7.81 billion, as on 21 May 2020. The company’s current portfolio includes high-quality Australian retail, office, and logistics property assets. With GPT’s funds management platform, the company has around $25.3 billion of property assets under management (AUM).

GPT is focused on leveraging its extensive real estate experience to deliver strong returns through disciplined investment, asset management and development. Over the recent years, the company has increased its exposure to the Office and Logistics sectors which has increased the resilience of the business. From 2015 to 2019, the company’s Net tangible asset (NTA) per security has increased at a CAGR of 8.6%, rising from $4.17 in 2015 to $5.80 in 2019. Over the same period, the FFO per security has increased at a CAGR of 3.68%. .png)

Group Financial Performance (Source: Company Reports)

For FY20, the company was expecting its FFO per security to grow further by 3.5% on last year. However, due to the uncertainty surrounding the Covid-19 pandemic, the company recently withdrew its earnings guidance. It is to be noted that GPT Group commenced 2020 with solid momentum and entered Covid-19 pandemic in a strong position. In response to the pandemic, the company has implemented several measures to protect its people and operations. The company expects that the significant government stimulus that is being applied and the co-operation between the levels of government to revive the economy, will provide GPT room for optimism for the recovery period. Moving forward, the company will continue to manage the business prudently and take the necessary steps to safeguard the business while the uncertainty prevails..png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters)

FY19 Performance Highlights: For the financial year 2019, the company reported FFO of $613.7 million, up 6.8% on FY18, driven by strong operating income from the office and logistics segments. For the year, the company reported statutory net profit after tax of $880.0 million, impacted by lower property valuation increases of $342.2 million and a higher negative mark to market of financial instruments of $82.7 million driven by lower market swap interest rates. For the full year, the company paid a distribution of 26.48 cents per share.

During the year, the company made significant progress in executing its strategy by delivering strong portfolio performance, growing its development pipeline and increasing investment in the logistics sector. In FY19, the company’s earnings were mainly driven by growth in its Logistics, Office, and Funds Management divisions, combined with savings in interest expense.

Over the year, the company secured 48 hectares in Melbourne’s west and 36 hectares of land in Western Sydney for future developments. Further, the company also completed the acquisition of the 25% interest in Darling Park Towers 1 and 2, along with Cockle Bay Wharf..png)

Financial Summary (Source: Company Reports)

Segment Wise Results: In the Office segment, the company reported net profit of $276.3 million in FY19, up 2.8% on last year. During the year, the company witnessed 6.2% comparable income growth in Office segment, driven by positive rent reversion, fixed rent increases and higher occupancy. In the Logistics division, the company saw 10.1% growth in income, driven by acquisitions and development completions, offset by lower development profits. Net income from Fund Management increased by 8.7% during the year, due to an increase in assets under management to $13.3 bn, mainly from the GPT Wholesale Office Fund acquisitions. Net income in the Retail segment was flat during the year..png)

Segment Results (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 37.57% of the total shareholding.

.png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

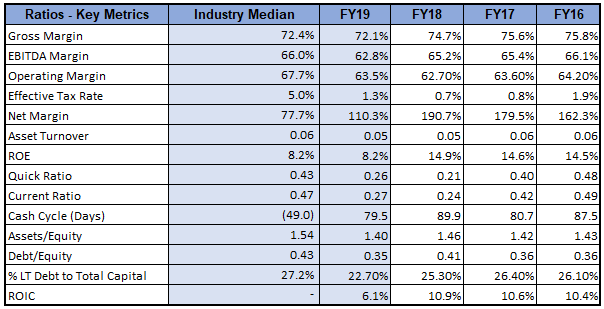

A Quick look at Key margins: For FY19, the company’s net margin stood at 110.3%, higher than the industry median of 77.7%. The company has an ROE of 8.2%, in line with the industry median. For FY19, the company reported a current ratio of 0.27x, up 10.2% on last year, demonstrating that the company has improved its ability to pay its short-term obligations.

Key Metrics (Source: Refinitiv, Thomson Reuters)

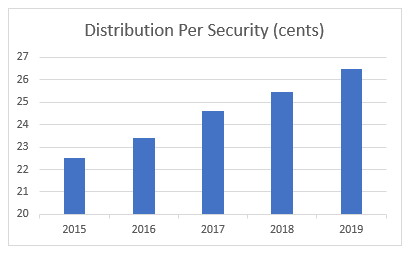

5-year Average DPS growth of 4.5%: The company follows a distribution policy that effectively aligns the Group’s capital management framework with its business strategy. For FY19, the company paid a distribution of 26.48 cents per ordinary security, up 4% on last year. This reflects a payout ratio of 103.4% of AFFO. The FY19 distribution growth has taken the company’s 5-year Average DPS growth to 4.5%. Before Covid-19, the company was expecting to achieve a growth of 3.5% for its FY20 distribution per ordinary security. However, due to the change in the company’s operating environment, and the uncertainty and unpredictability caused by Covid-19 outbreak, the company has withdrawn its distribution guidance.

Dividend Trend (Source: Company Reports)

Tackling Covid-19 Impacts: In response to Covid-19, the company has implemented a variety of initiatives to reduce or defer spending on non-essential and discretionary items across the business. The company has decided to defer the commencement of both the Rouse Hill retail expansion and the Melbourne Central office and retail development and has withdrawn 2020 Short Term Incentive Compensation scheme as well as the 2020 – 2022 Long Term Incentive scheme. It is expected that these measures will help the company to remain in a strong financial position and will place it better for the recovery phase post COVID-19.

March Quarter Update: In the middle of the March quarter, the company implemented measures to contain the spread of the coronavirus. This resulted in lower levels of foot traffic and a reduction in the number of stores trading, causing Total Centre monthly sales to decline by 21.3% and monthly Combined Specialty sales to decline by 27.3%. During the quarter, the Logistics portfolio occupancy increased to 98.6% as a result of the let-up of vacancies, the completion of developments, as well as the acquisitions over the period. In the March quarter, the company completed the Office leasing of 27,600 square metres and Logistics leasing of 38,500sqm.

What to expect: The company’s portfolio of high-quality assets in growth markets coupled with its development pipeline, has positioned it well to continue to deliver attractive returns. As mentioned above, earlier the company was expecting its FFO per security and distribution per security to grow by 3.5% in FY20. However, due to the uncertainty and unpredictability caused by Covid-19 outbreak, the company withdrew its FY20 distribution and earnings guidance. The company remains in a strong financial position, with approximately $1.3 billion in cash and undrawn facilities and only $5 million of debt to be re-paid before the end of 2021. The company expects that the significant government stimulus that is being applied, as well as the level of co-operation between all levels of government to revive the economy, will provide GPT room for optimism for the recovery period. Moving forward, the company will continue to manage the business prudently and take the necessary steps to safeguard the business while the uncertainty prevails.

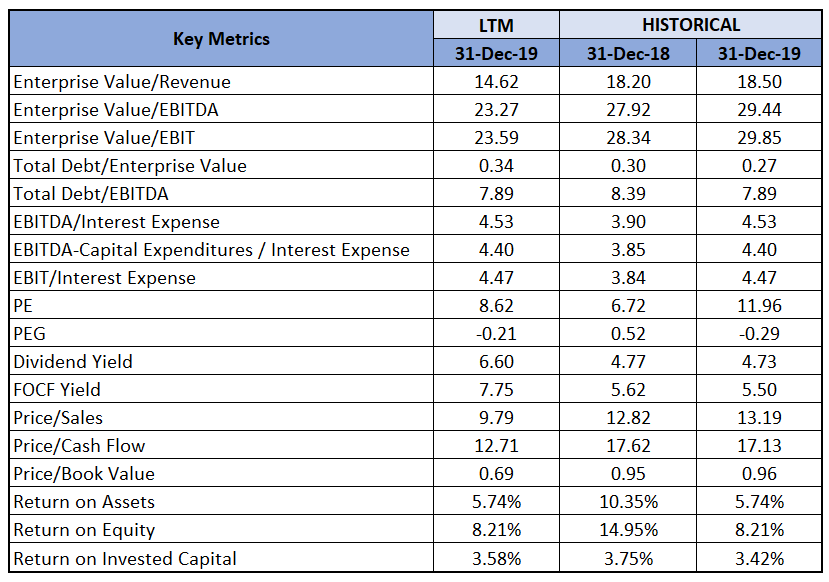

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

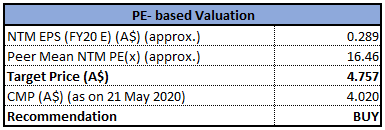

Valuation Methodology: P/E Multiple Based Relative Valuation Approach (Illustrative)

P/E Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months,

Stock Recommendation: The stock of GPT has corrected by 33.39% on ASX in the past six months, and it is currently inclined towards 52 weeks low price of $2.82, offering investors a decent opportunity to accumulate. The company is currently in a strong financial position, with around $1.3 billion in cash and undrawn facilities. We have valued the stock using Price to Earnings multiple based illustrative valuation method and have arrived at a target price with low double-digit upside (in % terms). For the purpose, we have taken peers like Dexus (DXS), Charter Hall Group (ASX: CHC), and Shopping Centres Australasia Property Group Re Ltd (ASX: SCP), etc. Considering the company’s diversified portfolio of high-quality assets in growth markets, its development pipeline, robust financial position, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $4.020, up by 0.249% on 21 May 2020.

.png)

GPT Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...