.PNG)

Australia has been doing well so far in terms of responding to the outbreak of coronavirus, with 6,713 confirmed cases of the coronavirus and recorded ~83 deaths as of 27th April 2020, as compared to a large number of cases and deaths reported in other countries. The government has acted proactively to prevent the virus from spreading on a massive scale and has taken the necessary steps to protect the individuals and the economy. The country has been able to deal with the outbreak by completely sealing itself off from the world, to prevent any chances of infection. As the economy has tumbled in the last few months, showing the adverse impacts of the outbreak on businesses and households, there has been an increased risk of a near-term recession.

Continued Efforts to Flatten the Curve: The Department of Health is managing the situation well and reported that majority of the COVID-19 cases in Australia were acquired overseas. There have been strict travel restrictions since the outbreak claimed its space in the country and since then, the situation has been brought quite under control. The flattening of the curve suggests a sign of recovery from the ongoing tensions and uncertainty, and a possible return to activity across the country. The government and health authorities, however, are not overlooking any kind of risk associated, which can ruin the efforts made so far.

.png)

COVID-19 Cases (Source: Department of Health, Australia)

Testing, Tracing and Distancing at the Heart of Containment: The National Cabinet met on 21st April 2020 to discuss on further decisions to be taken regarding the containment of the virus outbreak. The authorities will work closely with the medical professionals to progress on an elimination strategy for the virus, with the measures taken so far, largely leading to a slowdown in the number of coronavirus cases. As a result of the efforts in place, the government has been able to keep a continuous check on the burden on the healthcare system in the fight against the pandemic. Currently, the country is detecting around 92% of all the symptomatic cases and stands at a better position in terms of detection, as compared to many other countries dealing with the virus right now. In continuation of the above efforts, there will be continued development in the public health response to curb COVID-19, in terms of enhanced testing, tracing and local health response capabilities. In order to enable contact tracing amid the rising threat of community spread, Australia also has a contact tracing app under development, which will provide notifications about a nearby person diagnosed with COVID-19.

Economic Support for Survival: The Government is simultaneously taking gradual steps to ease the restrictions which might lead to the revival of the economy. With keeping the economic growth into consideration, the government has pulled up its socks to improve the country’s resilience against the challenges put forward in the current scenario. The state and federal governments have rolled-out stimulus packages to support the economy. For instance, the government announced ~$150 billion worth of packages to support workers, job seekers, families and businesses.

Discussion on the Roadmap to Recovery: In the National Cabinet’s meeting, one important point of discussion comprised of a possible ease of restrictions on some of the activities or services amid the current state of events. As the containment measures taken by the government have been denounced by businesses due to a blockage in profitability, the authorities mulled over an ease in restrictions to a certain level, with the Prime Minister stating that all restrictions put forward in light of the outbreak would be reviewed in four weeks’ time.

There has been a proposed ease of restrictions on Selected Services: As a result of the success in lowering the rate of COVID-19 spread, the subsequent flattening of the curve, and sufficient stock of Personal Protective Equipment (PPE) to meet the expected demand for COVID-19 response through to December 2020, the government has decided to lift the restrictions on elective surgeries, which, if withheld, may lead to adverse health outcomes, increase anxiety and social tensions. This, in turn, will impact the economic productivity, leaving the country in a worse position. Moreover, the National Cabinet also agreed on the recommencement of certain procedures from 27th April 2020, which will include IVF, screening programs for cancer and other diseases, post cancer reconstruction procedures such a breast reconstruction, procedures for children under 18 years of age, joint replacements including knees, hips, shoulders, cataracts and eye procedures, and endoscopy and colonoscopy procedures.

Increased Need for Testing and Treatment: An increased need for testing comes as a by-product of the above decisions, as more and more people will now move out for treatments, leading to an increased risk of spread. As a result, the government has discussed over the need for enhanced testing and tracing along with the easing of restrictions. Therefore, a rise in demand for testing services can be expected in the near term, to support the government’s objective of preventing the outbreak. Goes without saying that any increase in activity across the country will lead to a possibility of increased infections, which means an increased demand for treatment.

Overall, it can be said that an ease of restrictions does stand at the benefit of the society and the economy, as a whole. However, one cannot ignore the risks and uncertainties that come as a part and parcel of the above decisions. This is where some of the major players in the Australian healthcare sector come into picture, who are currently involved in the provision of services that form part of the relaxations announced and may witness increase in business activity as a consequence of rising demand for elective surgeries and other procedures. As a result, there will a rise in demand for testing and treatment, which is ought to benefit some healthcare providers which have been at the forefront of managing the crisis through testing kits and services and COVID-19 treatments. In light of the above scenario, let us have a look at few stocks in the healthcare domain that have the potential for growth and offer promising prospects despite the challenging external environment.

1. Virtus Health Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 233.13 Million, Annual Dividend Yield: 8.28%)

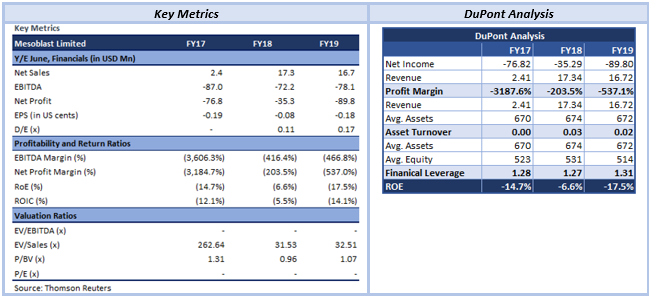

Stable Performance in Australian Operations: Virtus Health Limited (ASX: VRT) is a global leader in assisted reproductive services, focused on providing fertility care and related specialised diagnostic and day hospital services. For the half-year ended 31 December 2019, VRT reported revenue of $142.1 million, up 1% on pcp, showcasing the company’s resilient performance despite the changing market conditions. Over the same time span, the company’s total EBITDA grew by 21.9% to $39.5 million and NPAT increased by 3.7% to $15.5 million.

In terms of Australian operations, the company managed to maintain growth in Queensland and Victorian premium service volumes during the period, however, premium service volumes declined in New South Wales and TAS due to soft market conditions. Diagnostics revenue remained stable over the period, with cost management initiatives implemented. Australian IVF clinic EBITDA increased by 4.5% in H1FY20.

Outlook: Going forward in FY20 and FY21, the company is focussed on growing diagnostic revenue and non-IVF day hospital revenue in Australia. In order to deal with the impacts of Covid-19, VRT has recently taken a range of initiatives to reduce costs and minimise cash outflow to preserve liquidity. The company has reduced the fixed remuneration for Senior Executives and has decided to defer the payment of the interim dividend. In Australia, although the cycle activity in March was slightly ahead if compared to pcp, the Federal Government’s suspension of non-urgent elective surgery is expected to reduce cycles until the suspension is lifted.

Recently, the Australian Federal Government lifted the suspension on elective surgery, including Assisted Reproductive Services, as a result of which, VRT is planning to resume fertility services and ARS treatment from 27 April with increased infection control and safety protocols. Notably, the company has introduced COVID-19 testing for patients after consultation with their fertility specialist, with a 24-hour test turnaround time for results.

.png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales multiple based relative valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

.png)

A-VIX vs VRT (Source: Thomson Reuters)

Stock Recommendation: In the last three months, the stock of VRT has declined by 35.12% but over the last one month, the stock has increased by 34.88%. The company continues to implement cost saving initiatives and reduced its cash outflow activities. As 31 March 2020, VRT had a cash balance of $24 million, up ~$11 million in comparison to the cash balance as at 31 December 2019. After a steep fall in the stock price due to high market volatility during March 2020, there has been a commendable recovery as the business continued to be resilient to the current market conditions. A speedy recovery can be attributed to an excellent business model, backed by a strong domestic and international presence. After the recommencement of IVF treatment, the company’s Day hospitals and diagnostics services in Australia are expected to be key catalysts for further growth. We have valued the stock using EV/Sales based illustrative relative valuation method and have arrived at a target price of lower double-digit upside (in percentage terms). Considering the company’s stable performance in H1FY20, its recent cost reduction initiatives, and recommencement of fertility services and ARS treatment in Australia, we give a “Buy” recommendation on the stock at the current market price of $2.95, up 1.724% on 27 April 2020.

2. Healius Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$1.49 Billion, Annual Dividend Yield: 2.5%)

Decent Performance Across All Divisions: Healius Limited (ASX: HLS) is one of Australia's leading healthcare companies with three main businesses – Pathology, Medical Centres and Imaging – and three emerging businesses – Dental, IVF and Day Hospitals. For the half-year ended 31 December 2019, the company reported revenue of $945.1 million, up 7% on pcp, with Pathology and Montserrat being the key contributors. The company’s EBIT and NPAT grew by 4% and 8%, respectively. In all its three main businesses, the company witnessed decent revenue growth. Performance during the period reflects the efficiencies derived out of organisational redesign and cost savings initiatives.

Outlook: Due to the Covid-19 pandemic, the company is currently focused on reducing costs and preserving liquidity. As per a business update in late March, the company’s performance was in line with expectations. However, due to the current uncertain environment, the guidance issued in February 2020 has been withdrawn. Recently, the company witnessed a strong increase in demand in COVID-19 tests per day at its laboratories. Due to significant deferral of non-COVID19 testing and elective services, the company has witnessed varying rates of volume decline in its businesses. HLS is closely working with Federal and State Governments to ensure its essential healthcare services are readily available in the community. The company has recently decided to defer its FY20 interim dividend. Through the combination of trading, cost reductions, cash conservation and Government funding, the company is expecting to remain within its banking covenants in FY20 and is targeting to maintain its bank gearing ratio below 3.0x.

.png)

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation Method (Illustrative)

.png)

Price to Cash Flow Multiple Based Relative Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

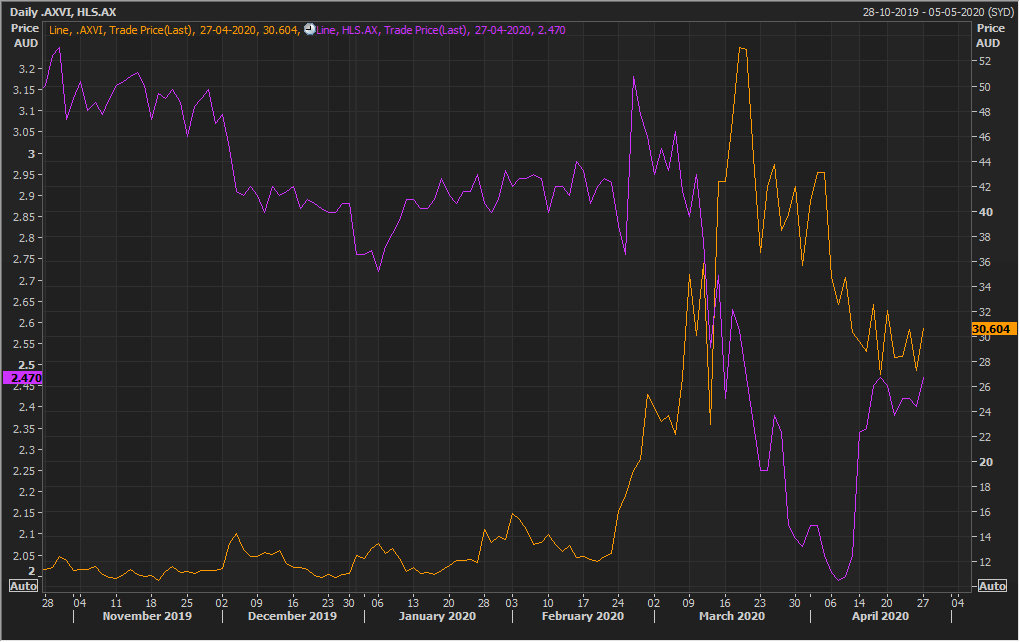

A-VIX vs HLS (Source: Thomson Reuters)

Stock Recommendation: HLS currently has over $200 million in available cash and committed undrawn debt facilities. In the last three months, the stock of HLS has declined by 18.64% on ASX but has increased by 6.67% in the last one month. The stock is currently trading slightly below the average of its 52 weeks trading range of $1.925 - $3.315. As the market fell prey to the outbreak of coronavirus and witnessed highly volatile conditions, the stock price plummeted as a response to panic selling by investors. However, recovery in the price has been decent afterwards, underpinned by a strong increase in demand. The company expects the demand to continue rising in all aspects of the business with a good market position and non-discretionary services at scale. We have valued the stock using Price to Cash Flow multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Considering the company’s decent performance in H1FY20, its recent cost reduction and cash preservation measures and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $2.47, up by 2.917% on 27 April 2020.

3. Mesoblast Limited (Recommendation: Hold, Potential Upside: High Single-Digit)

(M-cap: A$ 1.47 Billion)

Strong Revenue Growth in H1FY20: Mesoblast Limited (ASX: MSB) is a leading provider of allogeneic (off-the-shelf) cellular medicines with strong and extensive global intellectual property (IP) portfolio. For the half year ended 31 December 2019, the company reported revenues of US$19.2 million, up 43% on pcp. The company witnessed a 32% reduction in loss after tax to US$30.1 million driven by the increase in total revenues and a 22% decrease in research and development expenditure. During the period, the company experienced continued growth in revenues of TEMCELL in Japan. MSB filed a Biologics License Application (BLA) with the US FDA to seek approval of remestemcel-L2 for SR-aGVHD in children under the brand name RYONCIL3 and established a US commercial team for potential launch of its first allogeneic cellular product candidate RYONCIL for SR-aGVHD in children. In addition, the company entered into an agreement with Lonza for the commercial manufacture of RYONCIL to facilitate inventory build ahead of the planned US market launch.

Outlook: For the remainder of 2020, the company is targeting for several operational milestones, including the US launch of RYONCIL, expansion of investigator-initiated clinical trials for chronic GVHD and other indications, initiation of confirmatory trial in end-stage heart failure, and clearance from European regulatory authorities to begin European Phase 3 trial. The company had recently started evaluating its allogeneic mesenchymal stem cell (MSC) product candidate remestemcel-L in patients with acute respiratory distress syndrome (ARDS) caused by COVID-19 in the United States, Australia, China and Europe. Till now, the company has achieved remarkable clinical outcomes in these critically ill patients with 83% survival in ventilator-dependent COVID-19 patients (10/12) with moderate/severe ARDS. The company continues to progress with the randomized, placebo-controlled Phase 2/3 trial in COVID-19 ARDS patients to confirm that remestemcel-L improves survival in these critically ill patients.

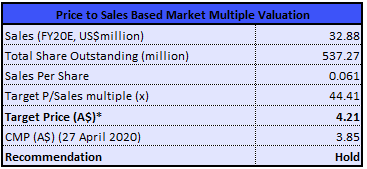

Valuation Methodology: Price to Sales Based Market Multiple Valuation (Illustrative)

Price to Sales Based Market Multiple Valuation (Source: Thomson Reuters), * 1USD= ~1.55 AUD as of 27 April 2020

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

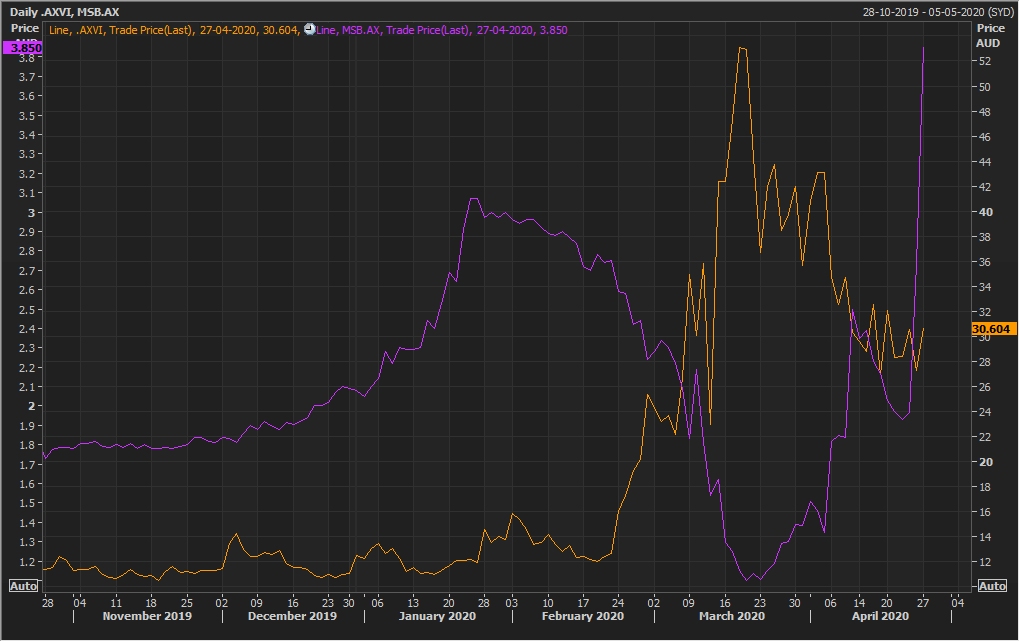

A-VIX vs MSB (Source: Thomson Reuters)

Stock Recommendation: In the last one month alone, the stock of MSB has increased substantially by 137.39%, and is inclined towards its 52 weeks high price of $4.450. While the stock price fell in response to high market volatility, demonstrating a usual response to panic selling by investors, it has picked up an excellent pace lately with a sharp rise, as depicted in the chart above. The company’s success can be attributed to a chain of recent developments involving the usage of Remetemcel-L in the treatment of COVID-19 related conditions. As a result of the above developments, the company will now be able to occupy a space in the frontline with respect to treatment of COVID-19. Considering the company’s strong H1FY20 results, remarkable clinical outcomes and expected operational milestones, we have valued the stock using Price to Sales market multiple based valuation method and have arrived at a target price with a high single-digit upside in percentage terms. Hence, we give a “Hold” recommendation on the stock at the current market price of $3.85, up by 41.026% on 27 April 2020.

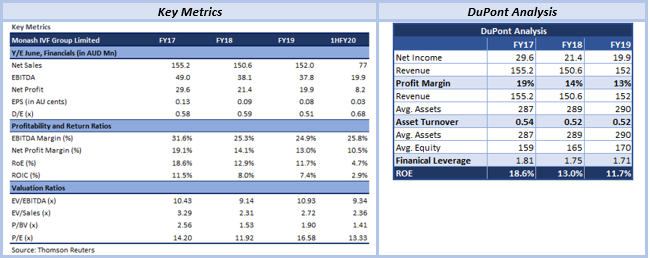

4. Monash IVF Group Limited (Trading Halt)

(M-cap: A$ 167.41 Million, Annual Dividend Yield: 7.18%)

Continuous investment in Operational and Strategic initiatives: Monash IVF Group Limited (ASX: MVF) is a leading provider of assisted reproductive services (ARS) and tertiary level prenatal diagnostics services. For the half year ended 31 December 2019, MVF reported group revenue of $77 million and Adjusted NPAT of $9.1 million. During the half-year period, the company witnessed volume growth in its SA and QLD businesses. In Australia segment, the revenues declined by 0.4% and Group Organic Stimulated Cycles grew by 0.5%, relative to pcp. Due to the loss of high marginal volume activity in Victoria and cost base investment in marketing, scientific capability and doctor capacity, the Australian Adjusted EBIT declined by 17.2% to $11.9 million whilst EBITDA margin declined by 2.6% to 20.1%.

In the international segment, revenue and Adjusted NPAT grew by 3.2% and 4.4%, respectively. Over the period, the company continued to make investment in its operational and strategic initiatives.

Outlook: Going forward, the company is focused on the expansion of its IVF domestic footprint and growing the full-service businesses through enhancing the group’s best-in-class patient experience and scientific leadership. Due to the uncertainty pertaining to current economic conditions and supply side risk caused by COVID-19, MVF has withdrawn its FY20 guidance. Further, the company has taken pre-emptive measures to protect its patients, employees and doctors and to manage the business through this period. In order to make sure that the business is well-positioned for the anticipated recovery, the company has decided to defer its interim dividend payment until 2 October 2020. To address the business impacts of COVID-19 and improve its balance sheet flexibility, the company has recently raised ~$80 million in equity raising. Following the equity raising, the company will stand with total liquidity of ~$97 million, after the payment of ~$77 million worth of debt.

After the announcement by the National Cabinet regarding recommencement of elective surgery procedures, including IVF, the company is ready to grab the opportunity to provide immediate services to patients with its leading technologies. With the gradual return of patients and an improved balance sheet position, the company has set the foundation to redeem the organic and inorganic opportunities available in Australia and South East Asia.

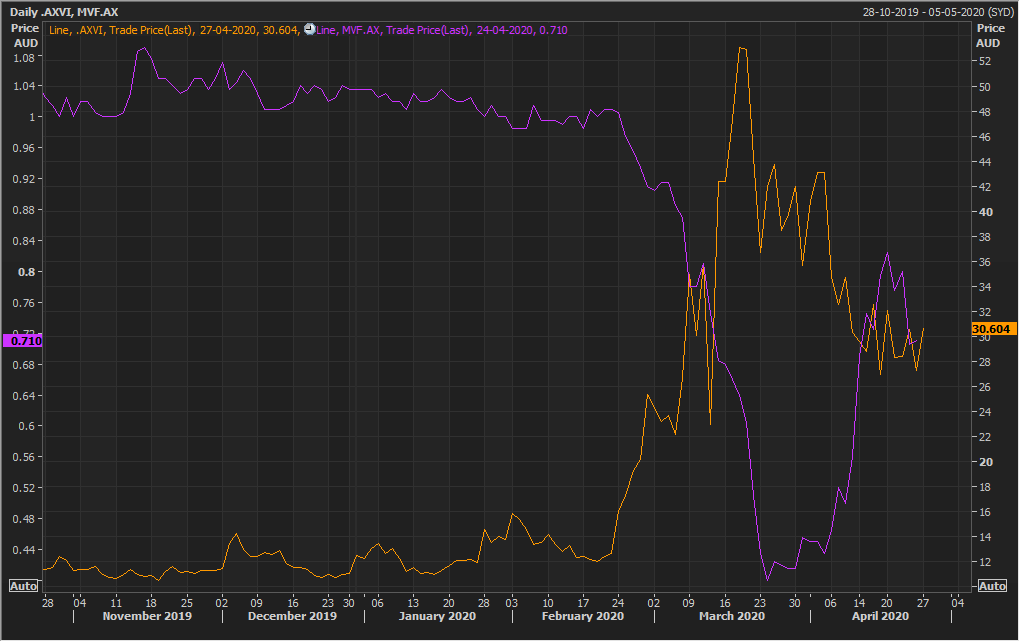

A-VIX vs MVF (Source: Thomson Reuters)

Stock Details: In the past six months, the stock of MVF has declined by around 30.05% but has increased by 77.5% in last one month. The company has a strong growth agenda behind the recent equity raising and aims to invest the money in specific growth initiatives including, opening of the new Sydney CBD fertility clinic as a flagship offering in NSW and joint venture, partnership and acquisition opportunities across South East Asia. Furthermore, the company is eyeing long term growth through transformation of its Melbourne footprint and further clinic upgrades. In addition to the above initiatives, the stock’s speedy recovery in an uncertain and volatile environment, forms another factor to confide in the business, going forward. Currently, the stock is on a trading halt pertaining to release of a pending announcement, with trading to commence on 29 April 2020 or on release of the update, whichever is earlier.

.JPG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

AU

AU

Please wait processing your request...

Please wait processing your request...