Company Overview - Galaxy Resources Limited is an Australia-based company engaged in mineral exploration and processing. The Company's principal activities include the production of Lithium Carbonate and exploration for minerals. Its segments include Australian operation, Argentina operation and Canada operation. The Australia operation segment includes the development and operation of the Mt Cattlin spodumene mine and exploration for minerals. The Argentina operation segment includes the development of the Sal de Vida project and exploration for minerals. The Canada operation segment includes the development of the James Bay project and exploration for minerals. The Mt Cattlin spodumene project is located over two kilometers north of the town of Ravensthorpe in Western Australia. The Sal de Vida Project is located in north-west Argentina. Its James Bay project is located in northwest Quebec, over two kilometers south of the Eastmain River and approximately 100 kilometers east of James Bay.

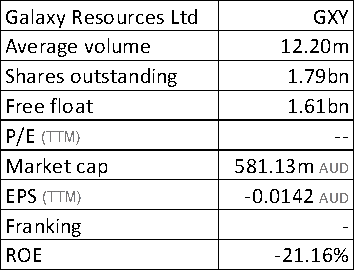

GXY Details

Turnaround to profit during the first half of 2016:Galaxy Resources Limited (ASX: GXY) has reported a fall in revenue to $15,215 in the first half of 2016 as compared to the corresponding period of 2015 of $17,738. On the other hand, the group reported a turnaround to profit during the first half of 2016. The generated profit after tax was of the order of $ 70,350,305 as compared to the loss after tax of $15,429,424 in the corresponding period 1H 2015. Therefore, in the first half of 2016, GXY reported the diluted earnings per share of 5.54 cents as compared to a loss per share of 1.44 cents in 1H 2015.

.png)

Financial Performance for First half of 2016 (Source: Company Reports)

World class asset development pipeline:GXY has a more attractive ownership then many of its peers as it has three wholly owned projects. The group made a second definitive offtake agreement on July 2016 at a price of US$ 600 / tonne with General Mining (GMM), Mitsubishi Corporation and a Chinese customer for the sale of 15,000 tonnes of lithium concentrate from the Mt Cattlin plant in 2016. They got a 50% prepayment of US$ 4.5 million from GMM. Moreover, the group reported for an off-market takeover bid for GMM Limited last month, while successfully closed with Galaxy acquiring a relevant interest in 96.74% of GMM’s fully paid ordinary shares. The Company even sent a compulsory acquisition notice to acquire the remaining GMM shares which were not accepted in the takeover bid, and expects to complete the acquisition by September 30, 2016. Meanwhile, the group estimates to deliver over 45,000 tonnes of lithium concentrate in 2016 at a minimum product specification of 5.5% grade of lithium oxide, and at US$600/tonne (FOB Esperance), which has less than 5% mica and 8% moisture content. Prepayment monies which account over 50% of the 2016 contract value were also made while the first tranche representing US$9 million was delivered in May 2016.

Moreover, the group along with GMM also agreed to deliver 120,000 tonnes of lithium concentrate in 2017 for the current customers while the sale price would be confirmed by fourth quarter of 2016 based on the market conditions at that time.

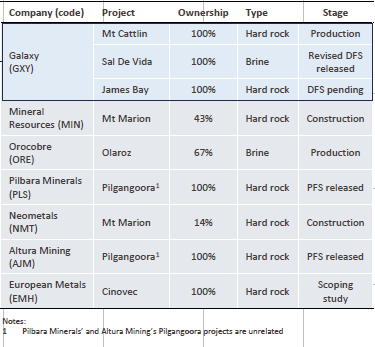

ASX Li Projects in development (Source: Company Reports)

Acquisition of General Mining:Galaxy Resources has acquired 96.74% General Mining Corporation Limited’s (GMM) shares through off-market takeover bid. The combined company would have the Mt Cattlin project, and is developing the Sal De Vida brine project in Argentina and also has the James Bay hard rock project in Quebec, Canada. The merger would also create Australia’s second largest lithium play and a major global supplier of high quality lithium. Moreover, the merged entity would improve the financial position and cash flow generation which would support project expansion, development and industry opportunities.

Diversified Project Portfolio: GXY has a diversified project portfolio with hard rock and brine based lithium assets across Argentina, Australia and Canada. The diversification provides GXY better margins performance irrespective of the lithium demand and pricing cycles. But as the lithium prices improve, GXY is well positioned to make good margin at Mt Cattlin and Sal De Vida Project. But, in case of a softer price environment, the brine assets are protected due to the superior low cost of operations.

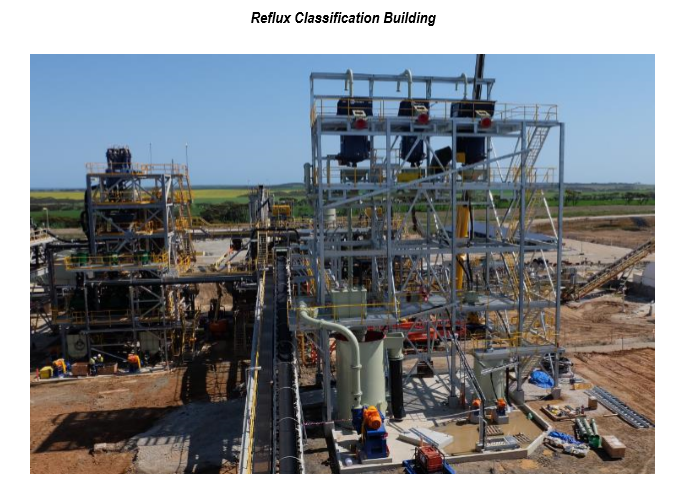

Mt Cattlin - Reflux Classification Building (Source: Company Reports)

Restarting Operations at Mt Cattlin:Operations at Mount Cattlin plant are estimated to start in November with first shipment from the Port of Esperance during December 2016. Mt Cattlin is the only new lithium mine to begin production globally. From this project, the group is forecasting to boost its cash flows. The production capacity has been increased from 800,000 tonnes to 1,600,000 tonnes annually. This would deliver substantial operational efficiency while higher capacity would meet the current demand for spodumene production from the Chinese market. Moreover, entire management control of Mt Cattlin is assumed to be by GXY after the completion of General Mining takeover, and the refurbishment and upgrade of Mt Cattlin is past 80% complete. In addition, there is an off take counterparty, wherein Mitsubishi Corporation and one of their Chinese customers have requested for an increased tonnage, which is above the already contracted amount for 2017 and later years. Galaxy is now negotiating terms with Mitsubishi and its Chinese customers for the additional tonnage which is now available from the expanded production. GXY has received US$13.5 upfront prepayment for 2016 volumes. Additionally, GXY has done combination of changes being built into the mica removal circuit for reduction of mica content below 5% of the total mass in the finished concentrate, while upgrading fine lithium content to above 5.5% Li

2O and cutting the operational costs for fines treatment by removal of flotation circuit.

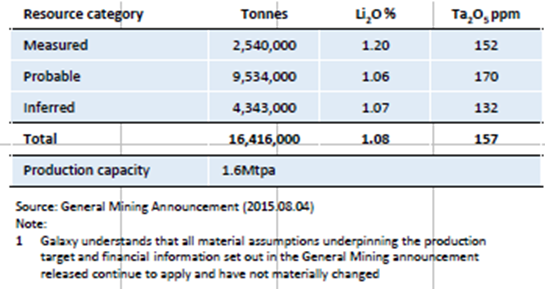

Resource and Production Capacity (Source: Company Reports)

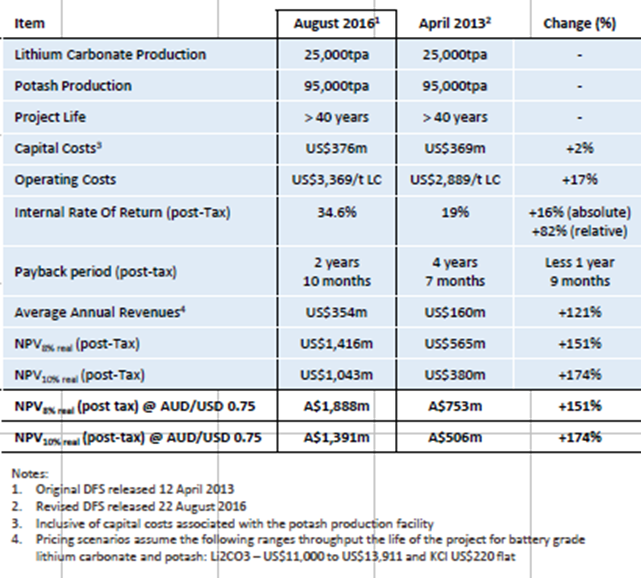

Sal De Vida Project:The project offers solid protection against lithium carbonate price changes given its high margins coupled with low opex associated with brine related to hard rock. Moreover, GXY has reaffirmed the strong potential for a low cost and long life operation from the update to its Definitive Feasibility Study (DFS). The revised DFS now estimates a post-tax net present value (“NPV”) of US$1.416 billion at an 8% discount rate (US$1.043 billion at a 10% discount rate). Sal De Vida has the potential to generate average annual revenues of US$354 million and average operating cash flow of US$273 million per annum. The Mineral Reserve estimate of 1.1 million tonnes of recoverable lithium carbonate equivalent and 4.2 million tonnes of potassium chloride (potash or KCI) equivalent for the project supports annual production of 25,000 tonnes of battery grade lithium carbonate and 95,000 tonnes of potash over a period of 40 years.

As a result, the revised DFS highlights the long project life with the low operating cost of the project, firmly positioning Sal De Vida as a low cost, high grade lithium project. In addition, the project supports 25,000 tpa lithium carbonate and 95,000 tpa potash production. On the other side for James Bay Project, a DFS team was assembled in Q1 2016 for review and GXY would recommence DFS work at the end of 2016, while the company would take advantage of the earlier projects. The total inferred resources are 22.2Mt at 1.28% Li2O. Meanwhile, the group’s discussions efforts are underway for the offtake and potential strategic end users.

DFS Financial Comparison (Source: Company Reports)

Well positioned to leverage the booming Lithium Demand: Favorable economics and demand growth for lithium due to increase in new energy vehicle sales worldwide with large volumes led by China, are good signs for the company to prosper.

Moreover, the significant tightening of the supply side has led to significant increase in the price of the lithium. The lithium market is projected to grow at the compounded rate of 10%-12% annually, compounded through to 2020.

Stock Performance:The shares of Galaxy Resources stock rose over 57.78% in the last six months (as of September 13, 2016) and still have more potential. The lithium offtake for 2017 contracts would be negotiated given the rising demand for lithium which is consequently driving the lithium prices from the Mt Cattlin project.

The Sal De Vida project reflects better project economies. GXY securities have been added to the S&P/ASX 300 Index, S&P/ASX 200 Index and S&P/ASX All Australian 200 Index effective September 16, 2016, which would add more liquidity and shareholders return. We believe the stock has more upside left in the coming months and based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $0.36

GXY Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...