Company Overview: Gage Roads Brewing Co Limited is engaged in brewing, packaging, marketing and selling craft brewed beer, cider and other beverages. The Company operates through two segments: proprietary brand brewing and contract brewing. The Company offers a range of ales and lagers, which are crafted in Western Australia. The Company offers dry-hopped and unfiltered beers. The Company's beers include Little Dove, which is a new world-style pale ale; Sleeping Giant, which is an India pale ale; Single Fin, which is a summer ale; Narrow Neck, which is an American-style pale ale; Break Water, which is an Australian-style pale ale; Atomic, which is an American-style pale ale; Small Batch Lager, which is a European lager, and Premium Mid Pils, which is a Czech Pilsener..png)

GRB Details

Strong Growth Across All Channels and Decent Increase in EBITDA: Gage Roads Brewing Co Limited (ASX: GRB) is engaged in brewing, packaging, marketing and selling of beer, cider and other beverages. As on 21st February 2020, market capitalisation of the company stood at ~$80.33 million. In the recently held Annual General Meeting, the management of the company stated that it had a pleasant year with strong growth, which resulted in increased earnings and ultimately higher value for the shareholders. Strong growth across all channels resulted in total proprietary brand sales of 8 million litres, up by 61% on pcp. During the year, both Single Fin and ALBY brands were extended into can formats and took advantage of the substantial growth within the craft market, which went up by 74%, and the total packaged beer market, which witnessed a growth of 11%. Matso’s Ginger Beer saw substantial growth over the year and continued to be the most valuable ginger beer brand in the retail channel. The increase in sales of the company’s higher-margin brands stemmed a rise in revenue by 20% to $39.7 million. In the same time span, the company’s own-brand portion in the sales mix has grown to 61% from 39% in FY18. This shift of sales mix to the company’s own brand resulted in an increase in gross profit to 64% from 61% in FY18. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR (Compounded Annual Growth Rate) of 12.95% in revenue and a CAGR of 26.99% in gross profit. The combined proprietary sales of the company along with AQB (Australian Quality Beverages) volumes resulted in a total throughput of 13.2 million litres. This generated an unaudited EBITDA of $5.5 million for FY19, an improvement of 25% over FY18. The company finished the financial year with a healthy cash balance of $9.3 million and zero debt.

The company has recently updated the market about its interim performance wherein it reported an increase of 10% in revenue to $19.3 million. This was mainly due to the growth in sales of the company’s own brands. The own-brand portion of the total sales mix went up to 68% in H1 FY20 from 62% in H1 FY19. This shift in sales mix and improvement in the margin are key performance indicators of the Proprietary Brand Strategy, indicating that the company is on track to deliver margin expectations in the upcoming years.

The company continues to see growth with its cost-neutral marketing strategy- Brand in Hand, which is expected to increase sales through greater brand awareness. Gage Roads Brewing Co Limited will continue to expand its distribution and is on track to deliver margin growth and earnings targets for FY20 and beyond. .png)

Sales and Channel Mix (Source: Company Reports)

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Gage Roads Brewing Co Limited. Perennial Value Management Ltd is the largest shareholder in the company, with a percentage holding of 10.06%. .png)

Top 10 Shareholders (Source: Thomson Reuters)

Cost Management and Increasing Returns to Shareholders: During FY19, the company witnessed an improvement in gross margin and EBITDA margin over the past year, at 42.4% and 14%, up from 37.5% and 13.5%, respectively. In the same time span, net margin of the company went up to 6.7% from 6.2% in FY18. This indicates that the company is managing its costs well and is able to convert its revenue into profits. Over the span of 4 years, Return on Equity witnessed an improvement and stood at 5.9%. This implies that the company is well deploying the capital of its shareholders and is capable of generating profits internally. During FY19, current ratio of the company was 1.89x, higher than the industry median of 1.53x. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. In the same time period, Assets/Equity ratio of the company was 1.24x, lower than the industry median of 1.99x. This indicates that the business is financed with high proportions of investors funding and a small amount of debt, resulting in a financially stable balance sheet..png)

Key Margins (Source: Thomson Reuters)

Strong Base for Future Earnings: During 1HFY20, the company diversified its channel mix which delivered strong growth across the independent channel and on-premise draught channel, resulting in total Good Drinks brands going up by 17% to 4.2 million litres. During the half-year, the company deleted several non-performing brands expecting that the development of new products will compensate for the deleted volume. In the same time period, gross profit of the company went up by 12% to $13.3 million, and unaudited EBITDA stood at $0.3 million. Gage Roads Brewing Co Limited ended the half-year with a cash balance of $5.7 million and is expecting a positive cash flow impact in the second half. In the same time span, the company continued to invest in the Good Drinks Strategy with additional sales and marketing expenditure of $1.9 million. This strategy is building a strong base for future earnings, including the expansion into the east coast. During the half-year, the company has witnessed good traction in executing its strategy to develop opportunities in the underweight east coast markets..png)

H1 Earnings (Source: Company Reports)

Matso’s Acquisition and Good Drinks: During FY19, the company acquired 100% of Matso’s Broome Brewing Pty Ltd and introduced a new brand, Matso’s Hard Lemon. This acquisition delivered volumes and earnings expectations and provided a step-change for the 5-year proprietary brand strategy. This acquisition provided a major expansion to GRB’s brand portfolio. The company has recently issued 14,318,615 shares as a performance-based milestone payment owing to the acquisition of Matso’s Broome Brewing Pty Ltd. Matso’s acquisition triggered the re-branding of GRB’s sales & marketing team to Good Drinks and the Good Drinks strategy, which is expected to develop a highly capable sales, distribution and marketing team to enable broader distribution and deliver sustained sales and earnings growth.

Future Expectations and Growth Opportunities: The company is well-positioned to deliver growth in margins and achieve targets for FY20 and beyond, owing to the growth in Good drinks brands and its 5-year strategy. FY20 is expected to be the year of changing gears for GRB. Good Drinks team has placed its focus on developing a capable, empowered and nationally represented sales team. The company is also exploring potential targets for acquisition and international opportunities. New products have performed well during the year, and the company anticipates that major national retailers will follow the market. The company’s strategy to strengthen the relevance of its brand to each regional market is on track with the start of its taproom and microbrewery in Redfern. GRB expects to open the venue by Q4 FY20 at a cost of $4.5 million.

GRB has successfully placed itself as a top-tier national beer business partner and is strengthening its key account service capabilities. The company expects to spend an additional $3.2 million to finalise the venue for Redfern and another $4 million for completing expansion in the packaging line, in the second half of FY20. In 2HFY20, GRB is likely to have a positive cash flow impact, and remains funded through the operating cash flows and existing facilities. The company is targeting own brand growth of 20-25% per annum and has set a gross profit target of 65-70%. It is also targeting EBITDA growth of 25-30% per annum. However, temporary loss in sales impacted the short-term earnings and it is unlikely for the company to achieve EBITDA growth for FY20. The company also expects to achieve cost savings in distribution and warehousing and is targeting a gross contribution percentage similar to the prior year..png)

Key Valuation Metrics (Source: Thomson Reuters)

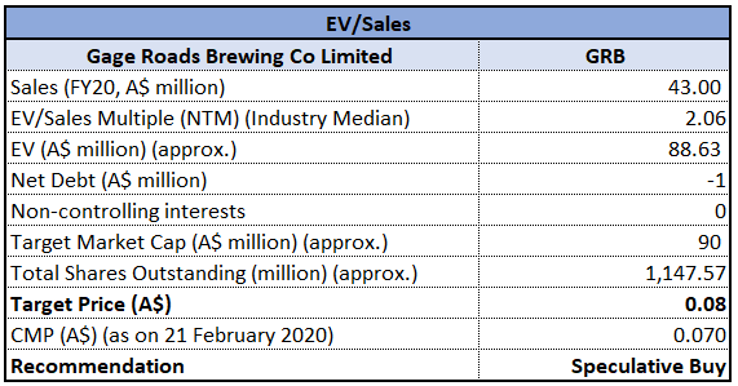

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of GRB is trading near its 52-weeks’ low level of $0.063, proffering a decent opportunity for accumulation. The company believes that the targets it has set are sound and achievable. GRB will continue to brew, sell and market beer and other beverages and will continue to expand its distribution. The addition of new brands, including the Atomic Beer Project, an evolving range of Gage Roads, and Matso’s, are complementing the existing brand portfolio. Considering the trading levels, improvement in key margins, CAGR in gross profit and significant growth opportunities, we have valued the stock using EV/Sales based relative valuation approach and have arrived at a target price offering an upside of lower-double digit (in percentage terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.07, with no change as on 21st February 2020.

GRB Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...