Company Overview: Gage Roads Brewing Co Limited is engaged in brewing, packaging, marketing and selling craft brewed beer, cider and other beverages. The Company operates through two segments: proprietary brand brewing and contract brewing. The Company offers a range of ales and lagers, which are crafted in Western Australia. The Company offers dry-hopped and unfiltered beers. The Company's beers include Little Dove, which is a new world-style pale ale; Sleeping Giant, which is an India pale ale; Single Fin, which is a summer ale; Narrow Neck, which is an American-style pale ale; Break Water, which is an Australian-style pale ale; Atomic, which is an American-style pale ale; Small Batch Lager, which is a European lager, and Premium Mid Pils, which is a Czech Pilsener.

.png)

GRB Details

Top-Line Growth of 20% Witnessed in FY19: Gage Roads Brewing Co Limited (ASX: GRB) is primarily engaged in brewing, packaging, marketing and selling of beer, cider and other beverages. As on August 23, 2019, the market capitalisation of GRB stood at ~$108.41 million. The company released its results for the year ended June 30, 2019 in which it continued to deliver on the key leading indicators during 3rd year of 5-Year proprietary brand strategy. In FY19, the company has garnered revenues amounting to $39.7 million (unaudited) which reflects a YoY growth of 20% and its gross profit rose 26% and stood at $25.5 million (unaudited). With respect to 5-Year proprietary brand strategy, it was stated that it seeks to increase awareness of the proprietary brands and expand those brands into the broader national markets, which could help in driving incremental sales from independent retail and on-premise channels to market. On September 20, 2018, the company made an acquisition of 100% of Matso’s Broome Brewing Pty Ltd. Since on-boarding the brands, the company has improved the growth in sales rates of Matso’s flagship product named Matso’s Ginger Beer and have reversed the decline of Matso’s Mango Beer. Additionally, the acquisition of Matso’s brands provided a step-change for 5-year proprietary brand strategy. In line with the strategy, own-brand portion of total sales mix has witnessed a rise from 39% in FY18 to 61% in FY19. The shift with respect to sales mix towards own brands has improved the total gross profit from 61% in FY18 to 64% in FY19. From the analysis standpoint, the company has improved its ROE to 2.2% in 1HFY19 from the prior corresponding period of 1.6%, and the debt-to-equity ratio stood at zero. Over the last three years (FY16-18), the company’s revenue from continuing activity and net profit attributable to members have been at compound annual growth rate (CAGR) of 14.1% and 83.6%, respectively.

Moving forward, there are expectations that the company’s debt-free position, decent operational and revenue-generation capabilities might act as tailwinds for overall growth. The company plans to explore potential targets for acquisition, which might help in the performance over the long-term.

.png)

FY19 Sales and Earnings Results (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader idea of the top 10 shareholders in Gage Roads Brewing Co Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Decent Key Margins in 1H FY19: The company’s key margins have witnessed a YoY growth in 1H FY19 as its net margin stood at 5.1%, which implies a YoY growth of 2.1% and, thus, it can be said that the company has improved its capabilities to convert its top-line into the bottom-line. The company’s EBITDA margin stood at 12%, which is an increase of 2.5% on a YoY basis. The current ratio of Gage Roads Brewing Co Limited stood at 1.34x, which can be considered at decent liquidity levels. Since the company happens to be in the debt-free position, it can be said that its balance sheet is stabilised. A deleveraged balance sheet is generally good for the long-term prospects of the business.

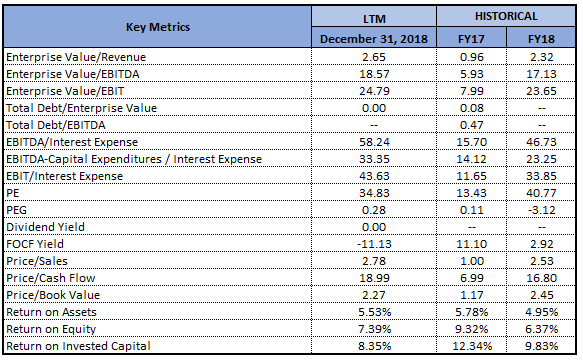

.png)

Key Metrics (Source: Thomson Reuters)

Announcement About Employee Share Plan Issue: Gage Roads Brewing Co Ltd has recently advised that, in accordance with the company’s executive and employee share plan, 3,000,000 shares have been issued to the number of eligible employees. Additionally, in the release it was stated that the issue was made to the key employees and shares are subject to the retention and earnings hurdles to help secure the employees for long-term benefit of the company and all shareholders. The shares were issued at an issue price of $0.093 each. The issue price was funded through a limited recourse loan provided by the company to eligible employees in accordance with the company’s Executive and Employee Share Plan, which was approved at the 2017 AGM.

Announcement About Completion of Placement: GRB announced that it has wrapped up a bookbuild and received irrevocable commitments to raise $8 million at an issue price of $0.095 per share (by issuing 84,210,526 shares) from the institutions and sophisticated investors. The release also stated that placement was well supported by the existing and new high-quality investors. The raised capital would be deployed towards implementation of the company’s packaging line expansion program. The program includes installation of new commercial scale canning line, a new high-speed bottle filler as well as other plant improvements. The following picture provides a broader overview of the company’s performance in Q3 FY19, which has been extracted from the investor presentation:

.png)

Q3 FY 2019 Highlights (Source: Company Reports)

Using the small-scale pilot canning line, the company has released Single Fin Summer Ale, Alby Draught and Alby Crisp in can format and they got overwhelmingly positive feedback and support from the independent retail customers and consumers. Over the period, GRB expects beer in can format to form up to 25% of its proprietary brand sales. It was stated that the new can filler, bottle filler as well as plant improvements provide cost efficiencies and reduced waste. With the new machinery installed, GRB is expecting additional earnings in the range of $1.5 million to $2.5 million by FY 2022. The company’s Managing Director named John Hoedemaker stated that strong support from the investment community is indicative of success of the proprietary brand strategy and a vote of confidence for GRB’s capital expansion program which has been designed to deliver the incremental earnings to all the shareholders.

Decent Balance Sheet Position in FY19: GRB ended the financial year with a robust cash balance of $9.3 million and enjoyed a debt-free position. During FY19, the business witnessed one-off non-recurring working capital movements as a result of the change of trading terms with Woolworths and the natural increase of debtors because of onboarding of Matso’s sales and revenues. The company has debt facilities to an approved limit of $6 million. Considering the additional headroom in credit facility, the business happens to be in a decent financial position, which provides an excellent platform from which to continue to a execute 5-year plan.

.png)

Cash Flow and Balance Sheet (Source: Company Reports)

What to Expect From GRB: The company stated that Good Drinks brands growth and 5-year strategy are on track to deliver the margin growth and earnings targets for FY 2020 and beyond. Additionally, it was stated that National chain volumes are in line with the anticipations. Moving forward, the company is expected to continue to explore the targets for potential acquisition and international opportunities. It was added that considering the flexible balance sheet, a management team strongly-aligned to the shareholders, existing revenue streams secured and enhanced ability to drive the revenue and margin growth, the company is well-positioned to deliver the growth in earnings and sustained value for the shareholders.

The company Managing Director has reflected favourable views and stated that the successful year was indicative of momentum of the business, and the key targets which have been set as a part of 5-year proprietary brand strategy are being delivered. Additionally, it was stated that business delivered robust growth in the earnings even with an increase in sales and marketing investment. In our view, the company has good potential to grow further at the back of decent cash position with nil debt facility and enhance the awareness of proprietary brands and expand those brands into broader national markets.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/EBITDA Multiple Approach (NTM)

.png)

EV/EBITDA Multiple Approach (NTM) (Source: Company Reports), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of Gage Roads Brewing Co Limited has witnessed a rise of 4.26% in the span of previous one month, while in the time frame of past six months, the stock has fallen 6.67%. As per ASX, the stock is trading closer to its 52-week lower levels of $0.087, indicating a decent opportunity for accumulation. Additionally, it was stated that Good Drinks team has been focusing on building capable, empowered, and nationally represented sales team.

On the analysis front, the company’s top line has witnessed a CAGR growth of 14.1% in its top-line in the time frame of FY16- FY18 and, thus, it can be said that the company has decent capabilities to generate revenues. The company’s cash from operating activities has witnessed a CAGR growth of 43.74% in the time frame of FY16- FY18 and, therefore, it looks like that GRB has decent operational capabilities. There are expectations that the company’s revenue-generation and operational capabilities might help it in tap growth opportunities moving forward. Considering these parameters, we have applied a relative valuation method, EV/EBITDA multiple, and have arrived at a target price of around lower double-digit (in % terms). Hence, in view of aforesaid facts and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.097 per share (down 1.02% on 23 August 2019).

.png)

GRB Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...