Company Overview: Gage Roads Brewing Co Limited is engaged in brewing, packaging, marketing and selling craft brewed beer, cider and other beverages. The Company operates through two segments: proprietary brand brewing and contract brewing. The Company offers a range of ales and lagers, which are crafted in Western Australia. The Company offers dry-hopped and unfiltered beers. The Company's beers include Little Dove, which is a new world-style pale ale; Sleeping Giant, which is an India pale ale; Single Fin, which is a summer ale; Narrow Neck, which is an American-style pale ale; Break Water, which is an Australian-style pale ale; Atomic, which is an American-style pale ale; Small Batch Lager, which is a European lager, and Premium Mid Pils, which is a Czech Pilsener.

.png)

GRB Details

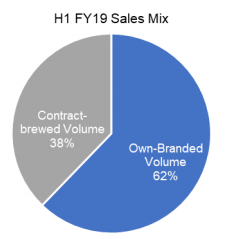

Understanding GRB’s Primary Driver of Growth: Gage Roads Brewing Co Limited (ASX: GRB) is an ASX listed company whose principal activities consist of brewing, packaging, marketing and selling of beer, cider, and other beverages. As on June 28, 2019, the market capitalisation of the company stood at ~A$99.56 million. The company had come forward and made an announcement about the half-year results ended December 2018 (i.e. 1H FY 2019) in which its proprietary brand sales witnessed a rise to 62% of the overall sales mix while GRB brand sales to the independent retailers rose 64%. The company continued to deliver on the primary leading indicators of 5-year proprietary brand strategy. In summary, the strategy focuses on increasing the awareness of its proprietary brands and expand those brands into the broader markets, driving incremental sales through retail and on-premise channels to market. The company stated that greater awareness of the consumer combined with the expanded access to these channels might help to continue to increase the annual volumes of the brands, delivering further improvement in the margins and sustained growth in the earnings through the shift in sales mix towards higher-margin proprietary products.The company stated that sales into national retail chains have witnessed an improvement as they have increased by 13% on H1 FY 2018. It was mentioned that a higher margin, on-premise draught sales have been performing well, and there was a total sales uplift of 136% as compared to 1H FY 2018. However, excluding the draught volume which was sold under the “brand-in-hand” strategy, the draught sales witnessed an improvement by 69%.

Moving forward, the company is expected to be benefited by flexibility of the balance sheet, respectable revenue generating capabilities, enhanced ability to drive the revenue and margin growth, strong operational capabilities. Additionally, the company is expected to be supported by capital raising.

1H FY 2019 Sales Mix (Source: Company Reports)

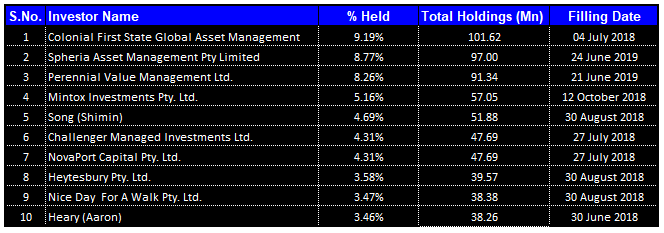

Top 10 Shareholders: The following table gives the broad overview of the top 10 shareholders of Gage Roads Brewing Co Limited:

Top 10 Shareholders (Source: Thomson Reuters)

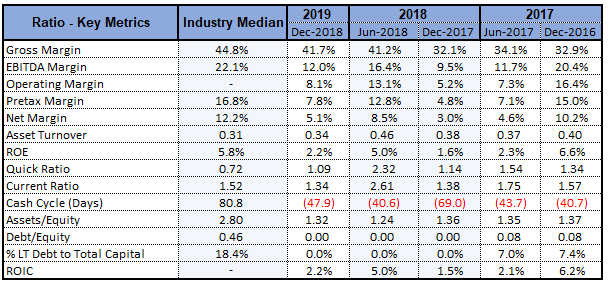

Improvement in Key Financial Metrics: The key financial ratios of Gage Roads Brewing Co Limited witnessed an improvement in 1H FY 2019 on the YoY basis as its net margin stood at 5.1%, reflecting a rise of 2.1% on the YoY basis and, thus, it can be said that the company has been effectively converting its top line into bottom line. Also, its EBITDA margin stood at 12%, which implies a rise of 2.5% on the YoY basis.

Key Metrics (Source: Thomson Reuters)

Also, the company’s Assets/Equity ratio stood at 1.32x in 1H FY 2019, which is lower than the industry median of 2.80x. GRB’s return on equity (or RoE) stood at 2.2%, which reflects a rise of 0.6% on the YoY basis, implying that the company has been delivering decent returns to the shareholders. The improvement in financials might help the company in gaining traction among the market players.

Significant Initiatives Might Help for Long-term Growth: During the half-year of 2019, Gage Roads Brewing Co Limited had spent $13.1 million in acquiring Matso’s Broome Brewing Pty Ltd, which was financed with the help of $10 million placement and a $2 million share purchase plan as well as operating cash. The company had made deployments amounting to $1.8 million towards the plant improvements, including small-scale canning line, flash pasteurisation capabilities as well as additional tank capacity. The company had ended half-year by having the cash reserves of $4.8 million as well as, with the additional headroom in credit facility (to the approved limit of $6 million), GRB happens to be in the decent position.

The company had witnessed the sales revenues amounting to $17.5 million for 1H FY 2019, which reflects a rise of 21% as compared to the previous corresponding period. The continued shift in product mix towards GRB’s proprietary brands had lifted the overall gross profit margin from 59% to 66%. The company happens to be on track to achieve FY 2021 target of 70%. In accordance with the 5-year strategy, the business had continued to make deployments towards sales and marketing capabilities, increasing the sales and marketing expenditure by $1.8 million and also accounting for additional $0.6 million in the employee expenses. GRB has been progressing Good Drinks Strategy, which revolves around the expansion of the national sales and marketing capability under trade facing brand of “Good Drinks”, developing the platform to the house as well as represent multiple separate brands. The strategy focuses on increasing consumer awareness and sales of Good Drinks portfolio.

Announcement About the Completion of $8 Million Placement: Gage Roads Brewing Co Ltd had made an announcement that it had successfully wrapped up the bookbuild and received the irrevocable commitments to garner $8 million involving an issue price amounting to $0.095 per share from the institutions and sophisticated investors. The company stated that the capital raised would be applied towards the implementation of GRB’s packaging line expansion program. The program consists of the installation of the new commercial scale canning line, a new high-speed bottle filler as well as other plant improvements. The improvements might help in driving increased plant efficiencies that would be resulting in the lower operating costs and improvement in the earnings. In the release dated April 24, 2019, the company stated that 84,210,526 ordinary shares have been issued to the institutional and sophisticated investors at $0.095 per share. It was added that placement had been made without the approval of the shareholder in reliance on GRB’s 15% annual placement capacity.

Project Funding (Source: Company Reports)

The company had also provided the highlights for Q3 FY 2019 and stated that its proprietary brand strategy happens to be on track and that GRB branded volume to the independents witnessed a rise of 55%. Additionally, it was mentioned that GRB branded draught volume (excl. “brand-in-hand volume”) witnessed an increase of 62%. Also, Matso’s brands have been performing strongly and the contract brewing volumes are in line with the FY 2019 expectations.

.png)

Q3 FY 2019 Highlights (Source: Company Reports)

Information About Employee Share Plan Issue: Recently, Gage Roads Brewing Co Ltd had noted that, in accordance with the company’s executive and employee share plan, 3,000,000 shares had been issued to the number of eligible employees. The release stated that the shares had been issued at an issue price amounting to $0.093 each and corresponding limited recourse loan agreements had been executed in accordance with terms of the executive and employee share plan.

What To Expect from GRB Moving Forward: GRB stated that there are distributionand sales growth opportunities in the independent channel and national chain volumes happen to be in line with the expectations and commitments. With respect to Good Drinks, the company would be focusing towards establishing the consumer and trade facing branded taproom and brewery venues in the key states, increasing the national marketing visibility as well as consumer awareness, increasing the partnerships and events to complement the growing east coast distributions and increasing the sales capabilities. The company stated that considering the flexibility of the balance sheet, a management team which is strongly-aligned to the shareholders, existing revenue streams secured and enhanced ability to drive the growth in revenue and margin, it is well positioned to deliver the growth in earnings and sustained value for the shareholders.

The company would be focusing on continued growth of the proprietary brands through all the channels and to deliver the incremental earnings as well as value to the shareholders.

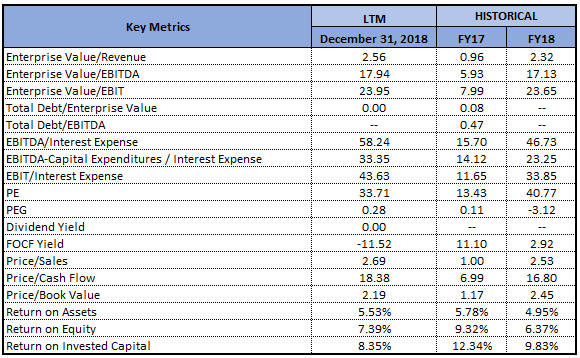

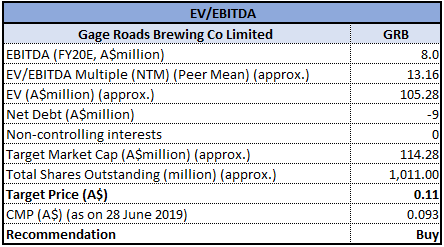

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/EBITDA Multiple Approach

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM: Next Twelve Months

Stock Recommendation: During the half-year, the company had on-boarded the Matso’s brands into the Good Drinks product portfolio. Since the acquisition in late September, the brands had performed as per the expectations and business is starting to witness growth as the company applies the sales and marketing capabilities to the brands. The company had witnessed a CAGR growth of 4.84% in its top line (FY 2014-FY 2018), which can be considered at respectable levels and reflects the company’s capability to generate the revenues. From the past few years (i.e. FY 2016-FY 2018), the company’s cash from the operating activities have been improving, which reflects its decent operational capabilities. Moving forward, there are expectations that the company’s respectable revenue generating capabilities and operational capabilities might be the primary growth catalysts for the company.

However, the company’s stock has delivered the return of -10% in the span of previous three months, while in the time frame of past one month, the stock’s return stood at -8.16% on an intraday basis. As per ASX, the company’s stock price is trading towards the 52-week lower levels, proffering an opportunity for accumulation. Based on the foregoing, we have valued the stock using relative valuation method, EV/EBITDA multiple and arrived at the target price, which offers a double-digit upside potential (in %). Hence, considering aforesaid facts and current trading level, we give a “Speculative Buy” rating on the stock at the current market price of A$0.093 per share (up 3.333% on 28 June 2019).

GRB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...