Company Overview - G8 Education Limited is an Australia-based company that provides developmental and educational child care services. The Company's principal activities are the operation of early education centers owned by the Company and its subsidiaries, and the ownership of early education center franchises. It is a provider of quality care and education facilities across Australia and Singapore through a range of brands. The Company's portfolio consists of approximately 490 child care centers. The Company's subsidiaries include Grasshoppers Early learning Centre Pty Ltd, Togalog Pty Ltd, Bourne Learning Pty Ltd, Ramsay Bourne Licences Pty Limited, Sydney Cove Children's Centre Pty Ltd, Kool Kids Operations Pty Ltd, Huggy Bear Operations Pty Ltd, Janes Place Operations Pty Ltd and World Of Learning Pty Limited.

.png)

GEM Details

Strong Portfolio across Australia: G8 Education Ltd (ASX: GEM) operates under 24 brands in Australia and Singapore, and had added 44 new centers and 13,697 licensed places in 2015. GEM owned 489 centers in Australia and 18 centers in Singapore with a total of 35,221 licensed places as on 31

st December 2015. Moreover, GEM’s acquisition strategy focuses on the consolidation opportunities in and around metropolitan areas where supply and demand dynamics combined with attractive pricing would create opportunities for earnings accretive acquisitions. GEM has the second largest market share of 7% for child care services in Australia. The group managed to execute the G8 corporate model with an emphasis on first class care provision through on-going investment in the staff, facilities and brand that has driven the occupancy growth. Meanwhile, GEM had enhanced the direct capital investment in the centers by 40% during 2015 while the operational support team has seen a step change in its quality and caliber with a number of key new hires and the investment in professional development to revolutionize the ability to train and upskill the staff.

.png)

Centre Portfolio and Market Share (Source: Company Reports)

Target market opportunity: Despite the short-term challenges including the impact from the recent election results, the company seems to be poised to take advantage from the rising demand for childcare services with both parents preferring to work for several reasons. This forces families to put their kids into childcare facilities and there is continuing pressure on governments to subsidize the same. The Australian Government is thus offering families with two types of financial assistance to approve child care costs. The Government intends to invest a good amount in the next five years for child care assistance, including a new Child Care Subsidy. The simplified Child Care Subsidy would be implemented from 1 July 2017 with a single subsidy as the family income, replacing the Child Care Benefit, Child Care Rebate and Jobs, Education and Training Child Care Fee Assistance Programme. GEM seems to be well positioned to capture the growing demand for child care services while adapting with the regulatory changes. Moreover, the sector continues to exhibit high degrees of fragmentation coupled with favorable underlying fundamentals. This combined with the investment in the foundation of the business would ensure that the group is well positioned to deliver on its commitment. Investors need to note that from the last few years, the post-tax ROE is growing.

.png)

ROE Performance (Source: Company Reports)

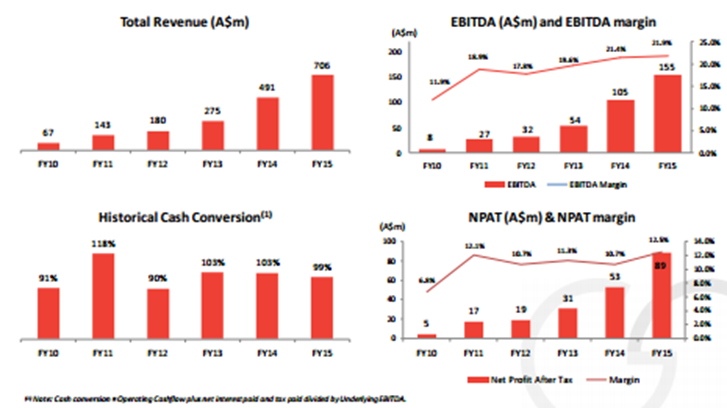

Strong Growth based Financials:GEM reported 68% growth in the profit for the fiscal year of 2015, ending at 31

st December 2015 and the revenue grew 44% to $706.2m during 2015 compared to the corresponding period last year. The underlying earnings per share increased 29% to 23.9 cents per share during the year. Moreover, GEM’s revenue has increased more than fivefold in the last five years. The EBITDA margin & the net profit margin has more than doubled in the last five years.

Additionally, GEM’s EBIT growth is driven by maintaining the revenue growth in excess of cost growth and exercising the discipline at the support office cost level. GEM has continued to generate year on year improvements in underlying EBIT margin of 21.2% for FY 15. GEM’s EPS growth over the last three years has been 115% while the total shareholder return, capital and dividends have been over 150%.

Financial Performance Track Record (Source: Company Reports)

High Cash Conversion Level:GEM has consistently given the high levels of cash conversion from underlying EBITDA.

This is through the stable and growing revenues generated by occupancy growth and market based fee rises, controllable and well understood operating costs and the capital light business model with the visible capital expenditure requirements.

.png)

Historic Cash Conversion (Source: Company Reports)

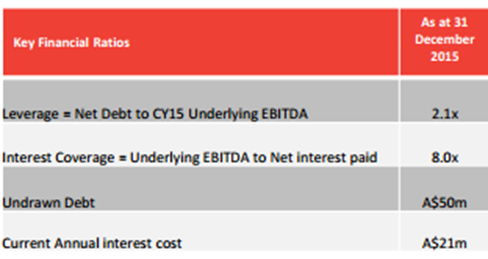

Capital Management efforts: GEM has replaced the Series 001 Notes (Singapore Dollars 260 million) by the Series 003 Notes (Singapore Dollars 270 million with maturity in May 2019) and had entered into the Second Supplemental Trust Deed and Settlement of Notes in connection with the S$260m 4.75 percent bonds. The fixed rate notes due 2017 (ISIN: SG6QC9000008) are issued pursuant to GEM’s S$600,000,000 Multicurrency Debt Issuance Programme.

Moreover, GEM’s gross debt to EBITDA and interest coverage highlight the company’s conservative capital management strategies. The group has received proposals to refinance the SGD260m bonds. GEM wants to hedge any residual FX exposure on the current SGD bonds to the refinancing date and fully hedge the new bonds to maturity. Additionally, the group will re-enter into a tender process for a senior secured revolving line of credit in the second half of 2016.

Debt Structure program (Source: Company Reports)

Quarterly Dividend Player:The Company pays its dividends on a quarterly basis rather than every six months rewarding shareholders with regular income. With further potential to consolidate and grow its share of the childcare market, G8 Education has the ability to grow its dividends over time. The group recently declared a distribution amount of $0.06 in the month of July 2016.

Management changes:The group has undergone certain management changes recently. GEM’s Chief Financial Officer, Chris Sacre left after ten years of the service. Three new members, namely, Gary Carroll, David Foster and Maria Forgione joined at the higher level. Gary has joined as the Chief Financial Officer, David has joined as a Non-Executive Director and Maria has joined as the company secretary. We believe that these transitions in key roles would be smooth.

Stock Performance:The group reported its objectives for CY16 and estimates a double digit growth in EPS, intends to refinance SGD$260m unsecured notes, to acquire between $50m and $150m in center acquisitions and to maintain the net debt to EBITDA about 2x (expected to be 2.1x at December 31, 2016). Meanwhile, the shares of GEM generated returns of over 17% in the last one year while the stock rose over 16.14% in the last six months (as of August 12, 2016). On the other hand, the stock has corrected over 6.9% in the last one month ahead of its results, as investors are concerned over the group’s potential increase in costs coupled with the current volatile market conditions that may impact its performance. However, we believe that the group is well positioned to handle this pressure and is on track to achieve its EPS targets. The group’s efforts to achieve maximum occupancy at its centers could offset the costs pressure to a certain extent. Moreover, despite the stock rally, GEM stock is trading at reasonable levels offering an investment opportunity for long term investors. GEM is having a solid dividend yield and is trading at decent P/E.

GEM continues to pursue its objectives of increasing the profitability and the market share of its child care business. This will be achieved through organic and acquisitions led growth. We have been bullish on GEM for quite a while and despite the stock generating profits, we believe there is more long-term potential. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $3.69 , ahead of its results which are scheduled by the end of August.

GEM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...