Company Overview - G8 Education Ltd. is an Australia-based company. The Company is a provider of developmental and educational child care services. The Company is engaged in the operation of child care centers owned by the group; contract management of childcare centers, and ownership of childcare centre franchises. As of December 31, 2011, the Company operated/managed 134 child care centers. The Company’s subsidiaries include Grasshoppers Early Learning Centre Pty Ltd, Ramsay Bourne Licences Pty Limited and G8 KP Pty Ltd, among others. In June 2013, the Company acquired Dolphin Early Learning Centres, an Austral-based provider of childcare and education services. In July 2013, the Company acquired Mary Poppins, Peppercorn & Smart Care Childcare and Education Centres. In December 2013, G8 Education Ltd, acquired 29 undisclosed premium childcare & education centres. In April 2014, the Company completed the acquisition of a number of companies which formed part of the Sterling Early Education group.

Analysis - G8 Education (GEM) has gained focus again in view of various recent announcements. As per the latest guidance announced by the Company, GEM anticipated an audited EBIT for FY ended 31 December 2014 to exceed the average forecast of the eleven brokers that cover GEM being $101 million, by less than 5%. This appears to be a positive guidance for CY14 and implies 2H14 EBIT of $70-75m as opposed to 2H13 of $33m while representing growth of 120% at the midpoint of the range. This also indicates that settlements may be ahead of what market expected earlier showcasing a relatively better operational performance.

.png) Cash & Cash Equivalents and Total Equity (Source – Company Reports)

Cash & Cash Equivalents and Total Equity (Source – Company Reports)

The Company further updated that during November 2014, the Company settled 15 childcare and education centres, adding 1054 places in Australia. GEM used existing cash reserves to fund the acquisitions. The Company has 437 childcare and education centres in Australia with a daily license capacity of 31,156 children. The ownership in Singapore remains unchanged at 18 childcare centres. Sometime back, the Company announced for acquisitions of 20 childcare centres at an EBIT multiple of 4.5x, which were to be funded by a $100m equity placement at $4.91. The total purchase price of the centres was highlighted to be $38.0m, with $36.7m payable on settlement and $1.3m of earnouts payable in 12 months upon the achievement of EBIT targets. These acquisitions have been expected to settle by the end of February 2015.

.png) Debt Profile (Source – Company Reports)

Debt Profile (Source – Company Reports)

Another insightful aspect is the Company’s announcement about the payment of 6 cent per share fully franked dividend for the quarter ending 31 December 2014. The dividend is expected to be paid and new shares are to be allotted on 21 January 2015. This comes in light of GEM’s decision to increase its dividend from 20 cents per share per annum to 24 cents per share per annum. As per the dividend reinvestment plan, shareholders electing to participate will be issued shares at a 5% discount to the daily volume weighted average market price for shares sold on ASX during the 10 trading day period commencing on the third trading day after the record date. The last date for receipt of election notices was 30 December 2014. DRP will be fully underwritten by UBS AG (Australia branch). Funds raised from this underwriting are planned for working capital purposes and to provide GEM with additional balance sheet capacity for acquisition strategy. This in a way also reflects that the Company is having strong performance of its operations. In fact, the acquisition led growth which has transpired over the past few months appears to be well handled and managed.

Over the last three years, GEM has achieved ~15% of organic EBIT growth per year indicating something which is more than the expectations. The annual fee increases along with GEM’s ability to better the operating metrics at acquired centres in terms of aspects such as occupancy levels, parent debt management etc. has facilitated good drive for organic growth. The Company is considered to be a top profit player in the long day care centre in Australia and has about 10% share of the addressable market currently. The financial health of the Company seems to be in good shape. The net debt to equity of 27% and EBITDA/interest coverage of 4.9 times constitute to the statistics. During the second quarter of 2014, sales totaled A$187.25 million, indicating an increase of 59.4% from the A$117.45 million in sales during the second quarter of 2013. In the near term, we see that acquisition multiple arbitrage is likely to continue and there will be demand for long day care services in metro areas which will be supported by government policies for child care funding. In fact, fee growth for long day care services has also grown ~8% per year over the past few years.

.png) Government Funding (Source – Company Reports)

Government Funding (Source – Company Reports)

The child-care industry has seen growth driven by Federal government policy and there is a commitment to spend more than AUD 25 billion during the next four years. Further, government incentives, such as the child-care rebate, have increased child-care affordability and encouraged higher female workforce participation. More particularly, the government investment in childcare has increased significantly over the last decade and the Commonwealth government funding is expected to continue with such a trend. There are also support initiatives put-in-place to assist with the cost of the childcare. Examples include, but are not limited to, jobs, education and training, childcare fee assistance program, the grandparent childcare benefit and the special childcare benefit. State and territory government funding focusses on the provision of preschool services. In a similar manner, the Singaporean government also provides child care subsidies to working and non-working mothers whose children are enrolled in a licensed centre. There are also some early childhood and development agencies to act as regulatory and development authorities for the early childhood sector in Singapore.

.png) Net Debt/EBITDA and EBITDA/Interest Expenses (Source – Company Reports)

Net Debt/EBITDA and EBITDA/Interest Expenses (Source – Company Reports)

Of course, certain risks revolve around acquisitions and competition for assets which may hamper the rate of making acquisitions; increased labor and property lease costs; and any changes to government regulation and changes to government subsidies to parents which may affect occupancy.

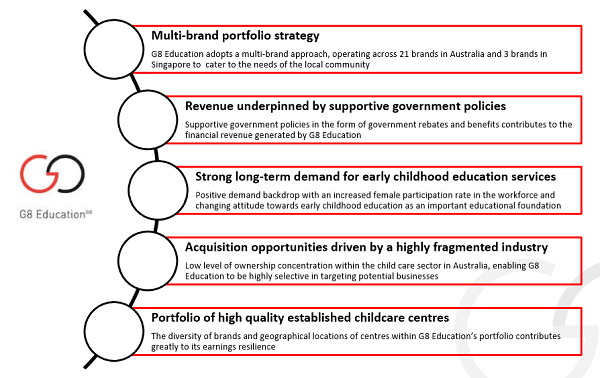

Competitive Strengths (Source – Company Reports)

Competitive Strengths (Source – Company Reports)

The robust growth profile coupled with good dividend yield and defensive earnings indicate a potential future. The Company’s long-term investment attractiveness appears to be good and is driven by higher quality business. GEM’s share price is steered through centre acquisitions. Thus, the acquisition-related announcements should act as the primary catalyst for performance. Then, the government’s response to the productivity commission proposal for increased government funding in the industry may act as an additional driver.

GEM Daily Chart (Source - Thomson Reuters)

GEM Daily Chart (Source - Thomson Reuters)

We put a

BUY recommendation for this stock at the current price of $3.93.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...