Company Overview: Freedom Foods Group Limited (ASX: FNP) is engaged in sourcing, manufacturing, sale, marketing and distribution of cereal and snacks and various other consumer staples. The company operates through five segments, namely Freedom Foods, Pactum, Pactum Dairy Group, Specialty Seafood, and Freedom Foods North America. The group operates sales, marketing and distribution activities various countries including Australia, New Zealand, China, South East Asia and North America.

.png)

FNP Details

Decent Increase in EBITDA and High Growth in Various Jurisdictions: Freedom Foods Group Limited (ASX: FNP) is engaged in manufacturing, selling, marketing and distribution of specialty cereal and snacks and plant and dairy beverages. As on 10 March 2020, the market capitalisation of the company stood at ~$1.22 billion. During FY19, the company witnessed an increase of 34.9% in net sales to $476.2 million and a growth of 40.9% in operating EBITDA to $55.2 million. The increase in earnings was mainly due to increased sales and earnings contributions from dairy beverage, nutritionals and plant beverage business units, which were offset by reductions in cereals & snacks and specialty seafood. In the same time span, the group achieved an operating net profit after tax (NPAT) of $21.9 million, up by 40.1% on pcp, reflecting increased operating EBITDA, offset by higher depreciation costs. During the year, the company witnessed high growth in various jurisdictions including Australia, South East Asia and China. This growing demand in dairy, plant-based beverage and cereal and snacks reflects the positive impacts on the company’s operational footprint. FNP is well-positioned to build into major global food and beverage business with scale in key food and beverage platforms. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR of 51.04% in revenue and a CAGR of 37.47% in gross profit. The decent financial and operational results enabled the Board to declare a fully franked final dividend of 3.25 cents per share, bringing the total dividends for FY19 to 5.5 cents per share. FNP has increased focus on building its brands in retail and other channel trade activities.

During 1H20, the company continued to achieve strong growth through key brands including domestic and out of home channels in its key markets of Australia, SE Asia and China and has also accelerated the final stages of its major capital investment programs including Shepparton and Ingleburn. In the same time span, FNP delivered an improved financial performance with higher sales revenue and earnings. During 1H20, the group established a Chinese Wholly Foreign Owned Enterprise in order to improve service and efficiency within its China operations.

New product revenue streams from key capital expenditure projects, including the Nutritional capability, are expected to have a positive impact on sales and earnings in the upcoming years. The company is reducing risks through diversification and is focusing on global and scalable brands. FNP will continue to evolve its scaled dairy capabilities into high value added protein based ingredients and consumer applications and is investing in people, systems and processes to manage a scaled and diversified business platform..png)

FY19 Financial Highlights (Source: Company Reports)

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Freedom Foods Group Limited. Arrovest Pty. Ltd. Ltd is the largest shareholder in the company, with a percentage holding of 52.61%. .png)

Top 10 Shareholders (Source: Thomson Reuters)

Increased Profitability and Financially Stable Balance Sheet: During 1H20, gross margin of the company stood at 27.1%. In the same time span, EBITDA margin of the company witnessed an improvement over the previous half and stood at 11.5%, up from 10% in 2H19. This indicates the increased profitability of the company. During 1H20, net margin was broadly in line with 1H19 and stood at 1.5%. In the same time span, current ratio of the company stood at 1.37x, up from 1.14x in 1H19. This indicates that the company is managing its costs well and is able to pay off its current liabilities using its current assets. During 1H20, Assets/Equity ratio of the company was 1.69x, lower than the industry median of 1.99x. This indicates that the business is financed with a more significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet..png)

Key Margins (Source: Thomson Reuters)

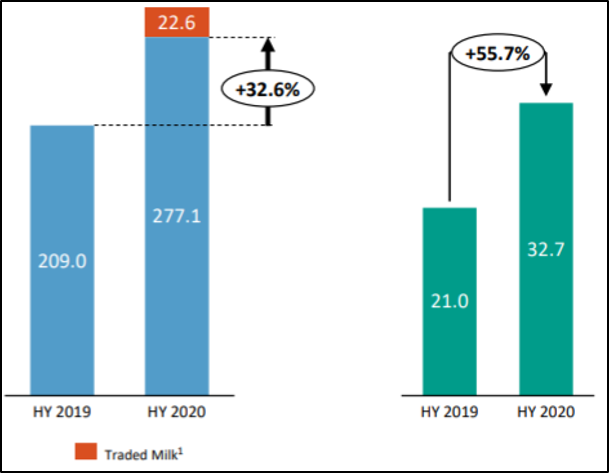

Increase in Net Sales and Net Profit: The company has recently released its interim results for the period ending 31 December wherein it reported an increase of 32.6% in net sales to $277.1 million and a growth of 55.6% in operating EBITDA of $32.7 million. This resulted in an increase of 45.6% in statutory net profit to $5.4 million. During the half year, the company achieved growth in key branded categories and channels and launched 40 new product formats into retail, grocery, out of home and export markets, supported by increased marketing expenditure. With an increased focus on building the group’s brands, FNP increased investments in brand building and marketing as well as in retail and other channel trade activities. During 1H20, the group finalised to upgrade the total processing capacity to 500 million litres per annum which will support the growth in UHT filling capability at Shepparton. In the same time span, the company reported a stable balance sheet with significant progress made on inventory management and total net borrowings of $188.5 million.

The company continued to make investments in people to ensure growth and further progressed the transformation of its IT / ERP systems to ensure increased efficiency and productivity. The company has declared an unfranked interim dividend of 2.25 cents per ordinary share which is to be paid on 22 May 2020.

Sales and EBITDA Growth (Source: Company Reports)

Completion of New Group Financing Facilities: The company announced that it has entered into new syndicated bank facility of $407 million with its long-term banking partners, HSBC and NAB for a period of three years. This new facility will provide a more flexible structure and will assist the company in ongoing growth over the medium term. The company, in another announcement, noted that all the payments had been made in respect to Blue Diamond Growers and there was no disruption to the supply of Blue Diamond almond paste. FNP has additional filling capacity being installed at its Ingleburn facility, which will provide ongoing growth in both the domestic and export markets of the company.

Future Expectations and Growth Opportunities: FNP is well-positioned to build into a major global food and beverage business with a larger scale in key food and beverage platforms, offering diversification in sales and earnings growth. The company’s partnership with – Australian Fresh Milk Holdings provides a level of the underwriting of further growth in milk supply in the longer term, with an ability to increase offtake, reducing any reliance on recruitment of new suppliers. During the year, the group also expanded its “Freedom Farmers” sourcing strategy and hence expects a total supply of 400 million litres per annum in FY20, with milk supply in FY 2021 expected to be around 430 – 440 million litres. The direct supply strategy seeks to align a multi-year volume, quality and pricing relationship, supporting the growing demands of the group. The group intends to expand this direct supply strategy in key Victorian supply regions to cater to the growing demand for milk.

FNP is confident that keeping a focus on its own brand strategy will result in growth and increased opportunities and hence will result in increased financial returns in the medium to long term. The group intends to pay an unfranked dividend for FY 2020 and anticipates fully franked dividends from increased profits after FY 2021. The increasing scale and diversification of the company’s activities provide a hedge to assist in mitigating potential impacts from short term disruption to a particular market. Freedom Foods Group Limited is leveraging its growing dairy capabilities to build a branded high margin product portfolio in specialty nutritional products..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/Sales Multiple Based Relative Approach.png)

EV/Sales Multiple Based Relative Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of FNP is trading close to its 52-weeks’ low level of $3.950, proffering a decent opportunity for accumulation. The company is expected to generate returns from its key brands and is growing its sales and financial returns. To reiterate, the increasing base of dairy volumes within the group will increase the demand across its key channels. The company has a decent outlook over the long-term despite short-term headwind due to coronavirus outbreak. Considering the trading levels, improvement in margins, decent financial performance and growth opportunities in the long run, we have valued the company using an EV/Sales relative valuation method and have arrived at a target price of lower double-digit growth (in percentage terms). For the said purposes, we have considered Bega Cheese Ltd (ASX: BGA), Blackmores Ltd (ASX: BKL), A2 Milk Company Ltd (ASX: A2M), etc. as a peer group. Hence, we recommend a “Buy” rating on the stock at the current market price of $4.47, up by 0.449% on 10 March 2020.%20(002).png)

FNP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...