Company Overview: Freedom Foods Group Limited is engaged in sourcing, manufacturing, sale, marketing and distribution of cereal and snacks; sourcing, manufacturing, selling, marketing and distributing plant and dairy based beverages; selling, marketing and distributing canned seafood, and investment in dairy farming operations. The Company operates through five segments: Freedom Foods, which includes cereal, snacks and branded plant-based beverages; Pactum, which offers a range of ultra-high temperature processing (UHT) food and beverage products, including liquid stocks, soy, rice, almond and dairy milk beverages; Pactum Dairy Group, which offers a range of UHT dairy milk beverage products; Specialty Seafood, which offers a range of canned seafood, such as sardines, salmon and specialty seafood, and Freedom Foods North America, which offers a range of products for consumers, including allergen free, low sugar, or salt, or fortified or functional.

.png)

FNP Details

Growth Driven by Key Brands: Freedom Foods Group Limited (ASX: FNP) is engaged in selling, marketing and distributing plant-based beverages, consumer nutritional products, canned specialty seafood, specialty cereal and snacks, etc. In FY19, the company continued to experience strong demand across its key markets and channels. During the year, the company was focused on accelerating its growth strategy and raised an amount of $130 million in May 2019 to fund the same. During the year, the company reported net sales amounting to $476.2 million, representing an increase of 34.9% on the prior corresponding year. Growth came in as a result of a positive response for key brands, including Australia’s Own, Freedom Foods, MILKLAB, and Messy Monkeys. Operating EBITDA and operating net profit for the year also reported double-digit growth in FY19. Overall, the period saw an improvement in financial performance with an increase in sales and earnings, through a continued contribution from key brands delivering improved results across key markets, including Australia, China and Southeast Asia. The company also invested in innovation, brand and market development, which assisted in shaping the performance during the year. During the year, the company also reported some major business initiatives, including a long-term supply agreement for lactoferrin, launch of 130 new product formats, expansion across the consumer nutritionals market through the acquisition of the Crankt assets and business, completion of stage one of a transformational nutritionals capability, etc.

As depicted in the picture below, the company’s sales over the four years period covering FY15-FY19, have responded positively to the business investments, comprising acquisitions, new product development, and capital expenditure. This reflects the company’s capability to make judicial use of funds and invest across areas that will boost growth in sales..png)

Five-Year Sales and Investment Performance (Source: Company Reports)

Going forward, the company expects continued support from the key brands mentioned above and expects to see the major impact of its capital expenditure initiatives in FY20 and beyond. The new product revenue stream brought into place through capital expenditure projects are expected to provide a boost to sales and earnings. In FY19, the company paid a final dividend amounting to 3.25 cents per share, which totalled to a full-year dividend of 5.5 cents per share. Dividends to be paid for FY20 are also expected to be unfranked, reflecting reduced tax payments on the back of utilisation of tax losses from acquisitions and accelerated tax depreciation benefits from the current investment phase. From FY2021, the company will get back to paying fully franked dividends from increased profits.

Insights into the Financial Performance: During the year ended 30th June 2019, the company reported net sales revenue amounting to $476.2 million, up 34.9% on the prior corresponding year. The Dairy & Nutritional Ingredients segment made the highest contribution to FY19 sales at $249.3 million. Sales reported by other segments are provided in the figure below..png)

Segment Sales (Source: Company Reports)

Operating EBITDA for the year stood at $55.2 million, representing an increase of 40.9% on the prior corresponding year. Operating net profit after tax came in at $21.9 million, increasing 40.1% in comparison to the previous year. Statutory net profit after tax went down by 9% to $11.6 million, as a result of one-off non-operating costs, covering unrealised foreign exchange losses, pre-acquisition costs, and costs pertaining to write-down of inventory and discontinued product formats, etc. The company continued to see an increased contribution from key brands, with sales from Group Brands increasing to $230.9 million or 48.5% of total sales in FY19, as compared to $158.9 million or 45.0% of total sales in FY18..png)

FY19 Financial Summary (Source: Company Reports)

A look at the Chinese Market: Sales revenue in China also grew substantially, with Dairy being the key contributor to growth. The region contributed $18.3 million in sales growth, reporting a rise of 37.3% on the prior corresponding year. Growth across China was however impacted by supply constraints relating to the UHT capacity expansion.

Exuberant Growth in South East Asia: Sales in the region went up by 178.8% on the prior corresponding year. Over a period of two years covering FY17 – FY19, sales across the region have reported a CAGR of 99.1%. In FY19, the company established a local team across key countries in the region. In FY20, the company is planning to introduce Drinking yoghurt into the market.

Highlights of Key Business Units: The company reported strong sales growth across the Dairy operations at Shepparton, which came in as a result of increasing demand in Australia, China and, Southeast Asia. The company also saw a minor contribution to results from the new integrated dairy nutritionals operation. With respect to the Consumer Nutritionals business, the company highlighted the contribution from increased sales of Vital Strength powder based branded products and Crankt branded beverage and bar formats. Sales increased for the plant-based beverage operations, with growth in retail and out of home brands. The Cereal and Snacks operations reported increased sales across key branded products. However, overall performance went down due to exit from some major contract manufacturing arrangements in cereals and milling. Earnings for the Cereal and Snacks operations were also impacted by increased investment in significant trade spend activities for the Messy Monkeys and Heritage Mill brands.

In FY20, the company expects to see the benefits out of its key capital expenditure initiatives undertaken since March 2018, complementing the financial results. These initiatives involve the capacity expansion in Shepparton and the new Nutritionals capabilities, which are expected to drive sales and earnings in FY20 and beyond. The company continues to attract farms that produce premium quality milk through long-term partnerships and has contracted ~400 million litres in FY20. Its key established brands, Australia’s own and Freedom Foods will continue to drive returns, with additional support from the recently launched MILKLAB, Messy Monkeys and Heritage Mill, which are expanding at an impressive rate.

Recent Updates:

Update on Bushfires: On 8th January 2020, the company released an announcement stating that the recent Victorian and New South Wales bushfires did not impact its dairy farms and site operations, with all sites remaining fully operational. The company reported zero disturbances to daily deliveries and is continuously in touch with the farmers to maintain an adequate supply of milk, which is currently in a strong position. To minimise the impact of any fresh milk shortage, the company is closely working with key retailers to provide the required support for the supply of ultra-high temperature (UHT) dairy beverages.

Business Update: On 10th January 2020, the company provided an update on reports pertaining to the dispute with Blue Diamond Growers. The company responded that all the payments for past shipments have been made and the supply of Blue Diamond almond paste has been carried out smoothly. Freedom Foods Group has a long-term relationship with Blue Diamond, for the manufacture and sale of the latter’s beverage products in Australia. The company also notified about the success of its plant-based beverage portfolio, which comprises Australia’s Own, Blue Diamond and MilkLab brands. As per the update, the portfolio has reported strong growth rates during the first half of FY20, more than the growth exhibited in 2HFY19. Growth across the portfolio is expected to accelerate as the company installs additional filling capacity at its Ingleburn facility in the second half. Further updates on the plant-based beverage portfolio will be provided on the release of the half-yearly results in late February 2020.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 66.55% of the total shareholding. Arrovest Pty. Ltd. held the maximum number of shares with a percentage holding of 52.67%.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

Key Metrics: In FY19, the company had a gross margin and EBITDA margin of 24.8% and 9.2%, respectively. Debt levels remained at decent levels, with a debt-to-equity multiple of 0.26x in FY19. Current ratio for the year stood at 1.56x, as compared to the industry median of 1.46x, depicting greater short-term liquidity in comparison to the industry..png)

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company aims to drive the dairy business towards specialty and high value-added products. Sales and earnings in FY20 and beyond are expected to benefit from the new product revenue streams from the Nutritionals capability. The plant-based beverages business is also expected to boost profitability over the medium term. Australia’s Own & Freedom Foods brands will continue to be key contributors to growth, with additional support from some newly launched brands. Overall, the management remains confident about building a globally successful business through continued benefits from diversification, earnings growth from key markets and channels, and brand success..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: Price to Earnings Multiple Approach.png)

Price to Earnings Based Valuation (Source: Thomson Reuters)

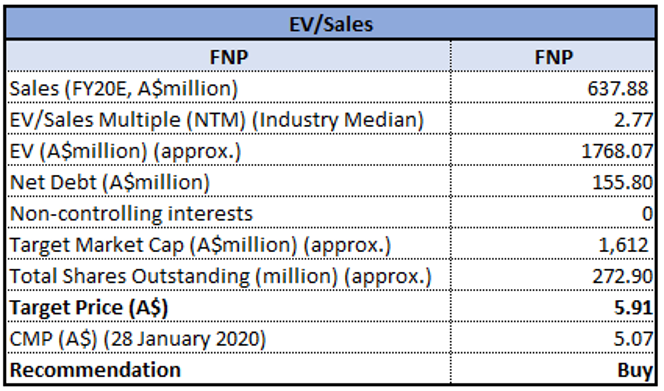

Method 2: EV/Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company generated positive returns of 9.68% over a period of 6 months. The company performed decently in FY19 and has issued a decent financial and operational outlook for FY20 and beyond. Combined benefits from new and existing brands, capital expenditure initiatives, and investment in innovation and market development, are expected to support the company’s growth strategy and boost its sales and earnings in the coming years. We have valued the stock using Price to Earnings and EV/Sales based relative valuation methods, and for the purpose, have taken the peer group Blackmores Ltd (ASX: BKL), A2 Milk Company Ltd (ASX: A2M) and Inghams Group Ltd (ASX: ING). As a result, we have arrived at a target price offering an upside of lower double-digit in % terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $5.070, down 2.687% on 28 January 2020..png)

FNP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...