Kalkine has a fully transformed New Avatar.

Company Overview: Freedom Foods Group Limited is engaged in sourcing, manufacturing, sale, marketing and distribution of cereal and snacks; sourcing, manufacturing, selling, marketing and distributing plant and dairy based beverages; selling, marketing and distributing canned seafood, and investment in dairy farming operations. The Company operates through five segments: Freedom Foods, which includes cereal, snacks and branded plant-based beverages; Pactum, which offers a range of ultra-high temperature processing (UHT) food and beverage products, including liquid stocks, soy, rice, almond and dairy milk beverages; Pactum Dairy Group, which offers a range of UHT dairy milk beverage products; Specialty Seafood, which offers a range of canned seafood, such as sardines, salmon and specialty seafood, and Freedom Foods North America, which offers a range of products for consumers, including allergen free, low sugar, or salt, or fortified or functional.

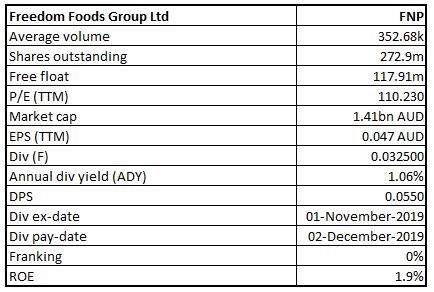

FNP Details

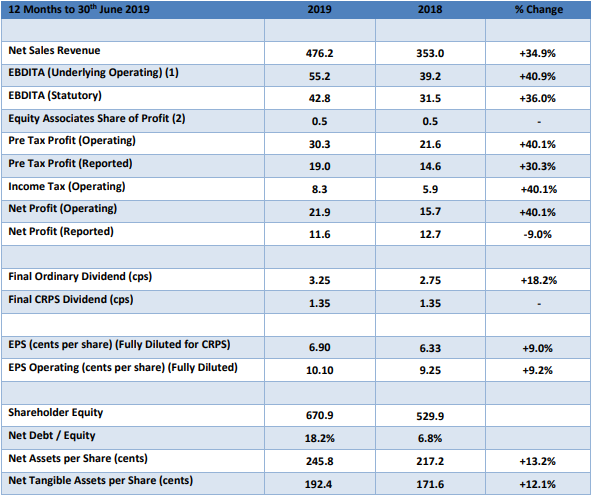

Decent Fundamentals: Freedom Foods Group Limited (ASX: FNP) is engaged in the business of operating sales, marketing and distribution activities in Australia, New Zealand, China, South East Asia and North America. As on October 8, 2019, the market capitalisation of Freedom Foods Group Limited stood at ~A$1.41 billion. The company released its full-year results for the year ended June 30, 2019 in which it stated that the company continues to achieve the high growth through its key brands, which include Australia’s Own and Freedom Foods in retail and MilkLab in out of home channels, in the primary markets of Australia, SE Asia, and China. The company’s net sales rose 34.9% and stood at $476.2 million, which implies an increase of $123.2 million while its operating EBDITA encountered a rise of 40.9%, and the figure stood at $55.2 million, implying a rise of $16.0 million. In the same period, EBDITA margin rose from 11.1% to 11.6%, with operating NPAT of $21.9 Mn, exhibiting an operating NPAT growth of 40.1% on a Y-o-Y basis. The primary growth drivers for EBITDA were dairy & nutritional ingredients (+110.8%), plant (+45.8%), and consumer nutritionals (+46.7%). On August 29, 2019, the Directors of the company declared an unfranked final dividend of 3.25 cents per ordinary share, which will be paid on December 2, 2019 with an ex-dividend date of 1 November 2019. It was further added that a record date for determining entitlement to the final dividend happens to be November 4, 2019. The total estimated dividend to be paid stood at $8,869,357. The company added that its key brands Australia’s Own and Freedom Foods would be at forefront of driving the returns from innovation as well as manufacturing capabilities in Australia and international markets, together with the new successes, i.e., MilkLab and Messy Monkeys. Revenues and operating profits are expected to increase as the company moves out of investment cycle, balanced against the requirement to invest in people, systems and process to manage the scaled and diversified business platform.

Financial Highlights (Source: Company Reports)

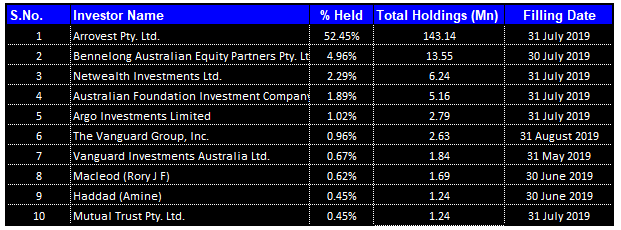

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Freedom Foods Group Limited:

Top 10 Shareholders (Source: Thomson Reuters)

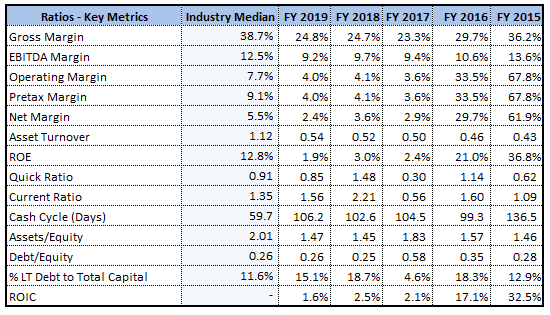

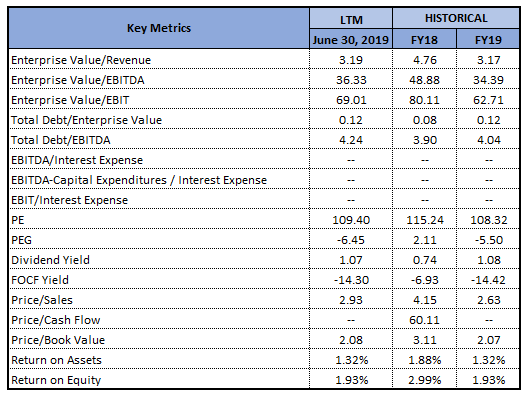

Key Metrics: Net margin stood at 2.4% in FY19 while its operating margin came in at 4%. The company’s gross margin stood at 24.8% in FY19, which reflects a marginal increase from FY18 figure of 24.7%. Current ratio stood at 1.56x in FY19, which is higher than the industry median of 1.35x and, thus, it can be said that FNP would be able to meet its short-term obligations. Additionally, decent liquidity footing places the company in a position to make deployments towards strategic growth objectives. These deployments might act as the key growth catalysts moving forward. The company’s Debt/Equity ratio stood at 0.26x in FY19, which is in-line with the industry median of 0.26x and, thus, it can be said that the balance sheet of FNP is quite stable. The lower debt/equity ratio is better for the company as it reflects lower debt on the balance sheet. With the help of lower debt, the company can focus on its long-term growth objectives.

Key Metrics (Source: Thomson Reuters)

Nutritional Ingredients Business Platform Update: Freedom Foods Group Limited has recently issued an update with respect to the progress of development of the nutritional ingredients business platform. The company has made an announcement that it has entered into the long-term supply agreement for Lactoferrin with a major global pharmaceutical company. The supply agreement would be utilising the significant component of the current and planned capacity for Lactoferrin at FNP’s nutritional ingredients facility in Shepparton, Victoria. The company has wrapped up $130 million equity raising, and an institutional component of equity raising was significantly oversubscribed, and there was robust demand from the broad range of high-quality institutional investors, which includes the current shareholders.

Understanding Performance in Different Markets: In the Australian domestic market, the company witnessed strong growth momentum and recorded sales growth of 37.5% on Y-o-Y basis. The following image has been extracted from the company’s presentation:

(1).png)

Domestic Sales Growth (in %) (Source: Company Reports)

The company witnessed high growth in China, and the region contributed $18.3 million in sales growth. However, the growth was impacted by the supply constraints with respect to UHT capacity expansion, but this would not be the ongoing issue into FY20. The company stated that there has been exceptional growth in SE Asia and the region has contributed $13.7 million in sales growth. In FY19, there has been an establishment of the local team throughout key SE Asian countries.

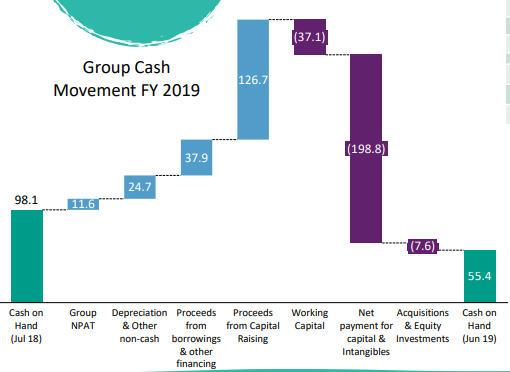

Financial Summary of FY19 Results: The company has achieved operating net profit after tax of $21.9 million, which reflects a gain of 40.1%, implying increased operating EBDITA, offset by the increased depreciation costs as compared to the previous corresponding period. The following image provides a brief overview of the group cash movement in FY19:

Group Cash Movement (Source: Company Reports)

The company had cash on hand of $55.4 million and borrowings of $177.4 million. The cash generated from operating activities stood at -$0.9 million for 12 months and the cash generated in 2H amounted to over $23.0 million. It was added that the positive movement is anticipated to continue into FY20. The company has received financing from the borrowings as well as equity raisings in order to help the accelerated strategy plans. Between the time span of FY15- FY19, the company’s top line has witnessed a CAGR growth of 51.04% and, thus, it can be said that the company is possessing sound capabilities to generate revenues. There are expectations that FNP’s revenue-generation capabilities might support its long-term growth prospects.

What to Expect from FNP Moving Forward: The company is increasingly well-positioned to build into a major global food and beverage business with scale in key food and beverage platforms. The company has been experiencing robust demand throughout the business activities in Australia, China as well as SE Asia. The growing demand in dairy, plant-based beverage and cereal and snacks implies a positive impact on expanded operational footprint and increasing brand penetration and market share in the primary strategic channels as well as categories in Australia, SE Asia and China. With the completion of stage one of transformational Nutritionals capability, the company would be continuing to evolve the scaled dairy capabilities into the high value added protein based ingredients as well as consumer applications.

The company stated that new product revenue streams from the major capital expenditure projects, which includes nutritionals capability are anticipated to positively impact sales and the earnings into FY20 and beyond.The recently wrapped up equity raising amounting to $130 million would be primarily used towards the acceleration of Freedom Foods’s growth strategy, which includes acceleration of $100 million in the capital expenditure in Nutritional ingredients through calendar year 2019 and 2020, that includes increased capacity for protein streams like native whey protein isolate, micellar casein as well as Lactoferrin and accessing the new protein streams.

The company’s cash receipts have witnessed a CAGR growth of 51.2% in the time span of FY15- FY19, and, therefore, it can be said that FNP possesses sound capabilities to build cash levels. It can be said that these capabilities might support the broader growth prospects of the overall company.

Key Valuation Metrics (Source: Thomson Reuters)

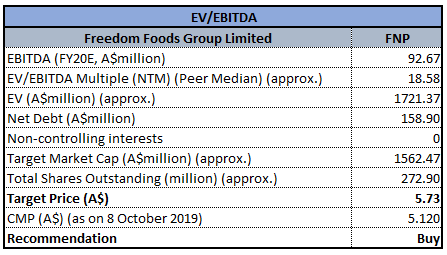

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Multiple Approach (NTM) (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The stock price of FNP has delivered a return of 5.08% in the time span of previous three months while, in the time frame of previous six months, the stock has increased 0.39%. At the current market price of A$5.120 per share, the annual dividend yield of the stock stood at 1.06%. Talking about the earnings summary for FY19, the company delivered improved financial performance, and it witnessed higher sales revenue and earnings. It was added that further deployment towards the innovation, brand and market development help the company to grow in the primary business divisions and markets. During FY13- FY19, the company’s cash and short-term investments witnessed a CAGR growth of 25.62%, which can be considered at decent levels. The company has sound capabilities to generate revenues and build cash levels, which can help it gaining traction among the market participants. Considering the performance in FY19 and decent growth prospects, we have valued the stock using a relative valuation method, i.e., EV/EBITDA multiple and arrived at a target price of lower double-digit growth (in %). Hence, we give a “Buy” recommendation on the stock at the current market price of $5.120 (down 0.967% on 8 October 2019).

.png)

FNP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...