Company Overview: Freedom Foods Group Limited is engaged in sourcing, manufacturing, sale, marketing and distribution of cereal and snacks; sourcing, manufacturing, selling, marketing and distributing plant and dairy based beverages; selling, marketing and distributing canned seafood, and investment in dairy farming operations. The Company operates through five segments: Freedom Foods, which includes cereal, snacks and branded plant-based beverages; Pactum, which offers a range of ultra-high temperature processing (UHT) food and beverage products, including liquid stocks, soy, rice, almond and dairy milk beverages; Pactum Dairy Group, which offers a range of UHT dairy milk beverage products; Specialty Seafood, which offers a range of canned seafood, such as sardines, salmon and specialty seafood, and Freedom Foods North America, which offers a range of products for consumers, including allergen free, low sugar, or salt, or fortified or functional.

.png)

FNP Details

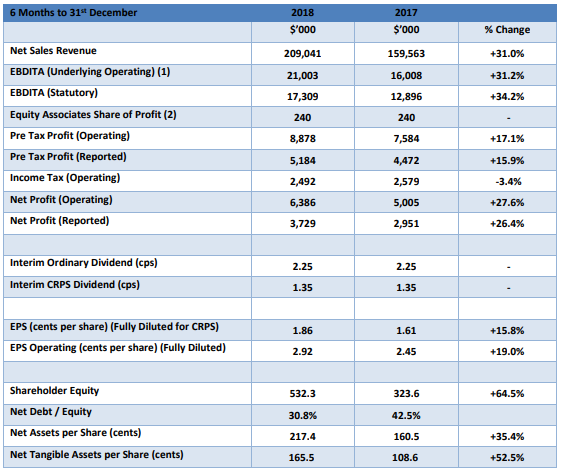

Decent Performance in 1HFY19: Freedom Foods Group Limited (ASX: FNP) is an ASX listed company that is engaged in the preparation, sale, marketing and distribution of plant and dairy based food products and beverages, in Australia, New Zealand, China, South East Asia, and North America. As on July 2, 2019, the market capitalisation of Freedom Foods Group stood at ~A$1.39 billion. The company had earlier released its results for the half-year ended December 31, 2018 in which its net sales witnessed a rise of 31.0% and stood at $209.0 million while, during the same period, its gross margin witnessed a rise of $14.5 million to $51.7 million and the margins increased to 24.7% from 23.3%. The company’s operating net profit witnessed a rise of 27.6% and stood at $6.4 million, while its statutory net profit increased by 26.4% to $3.7 million. The company stated that continued transformation has been driving growth via iconic brands, which includes Australia’s Own and Freedom Foods in retail and food service channels in the key markets of Australia, SE Asia, and China.

The company is one of Australia’s leading investors in the state-of-the-art food and beverage manufacturing capability and they have deployed over $80 million in the plant and equipment in 1H period. FNP stated that 1H sales and earnings results did not materially benefit as the result of the key capital expenditure initiatives which were undertaken since March 2018. However, the company anticipated these capital expenditure initiatives aligned with the increasing demand to further grow sales and earnings into 2H FY19 and beyond.

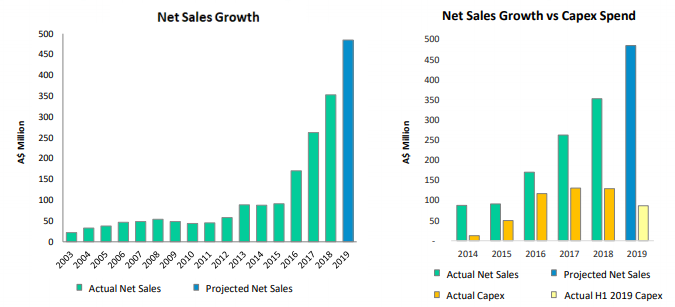

With respect to Dairy demand, there are expectations that there would be robust ongoing demand for the dairy products which includes UHT milk from export markets. Importantly, the company's revenue has grown at a CAGR of ~41.6% over the period of FY14-FY18. Going forward, the Management expects revenue to record a Y-o-Y growth in the range of 36.0% to 38.8% in FY19E against FY18. With this, we expect the CAGR-growth in revenue for the period FY14-FY19E at between 40.4% and 41.02%.

Key Financials (Source: Company Reports)

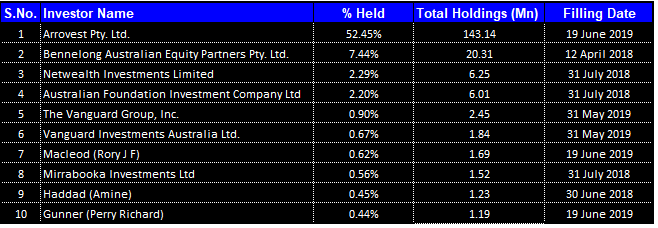

Top 10 Shareholders: The following table gives a broader overview of the top 10 shareholders of Freedom Foods Group Limited:

Top 10 Shareholders (Source: Thomson Reuters)

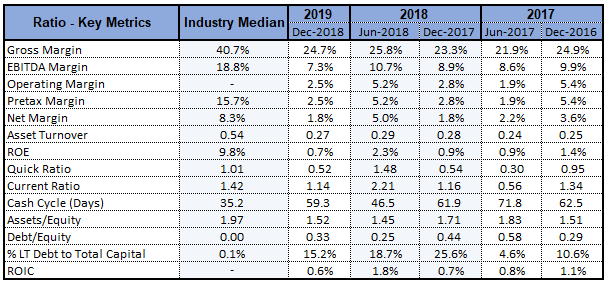

Decent Key Metrics: Freedom Foods Group Limited possesses a decent position with respect to its key margins as, in FY 2018, its net margin stood at 3.6% that implies a rise of 0.7% on the YoY basis, which reflects its capability to convert its top line into the bottom line. In FY 2018, its EBITDA margin stood at 9.7%, reflecting an increase of 0.3% on the YoY basis. However, in 1H FY 2019, its net and EBITDA margin stood at 1.8% and 7.3%, respectively. Also, in 1H FY 2019, the company Debt/Equity ratio stood at 0.33x, which reflects a fall of 25.2% on the YoY basis and, thus, it looks like that the company has been deleveraging its balance sheet.

Key Metrics (Source: Thomson Reuters)

Announcement About Completion of Retail Entitlement Offer and Shortfall Placement: On May 23, 2019, Freedom Foods Group Limited had made an announcement about the pro rata accelerated non-renounceable entitlement offer and institutional placement of the ordinary shares involving an offer price amounting to $4.80 per new share to garner around $130 million. In the release dated June 19, 2019, the company stated that they have issued a total of 27,193,464 New Shares which comprises of 24,857,605 new shares issued on May 30, 2019 and 2,335,859 new shares issued on June 19, 2019.

The shares issued on June 19, 2019 comprises of 1,485,787 new shares to the eligible investors and 6,262 new shares to a nominee for ineligible shareholders. However, it also comprises of 843,810 new shares which have been placed by Veritas Securities and UBS AG, Australia Branch to sub-underwriter Arrovest Pty Limited under shortfall placement. As per the same release, the total number of Freedom Foods ordinary shares now on issue stood at 272,903,282.

The retail offer booklet, which is related to 1 for 18 accelerated pro-rata non-renounceable entitlement offer at offer price amounting to $4.80 per new share, had stated the usage of funds. The funds garnered from entitlement offer would be utilised towards financing Freedom Foods’s growth strategy, which includes the key initiatives like accelerating the capital expenditure programs in nutritional ingredients through 2019 / 2020 amounting to $100 million and to support the increased working capital of $30 million to meet the growth in demand.

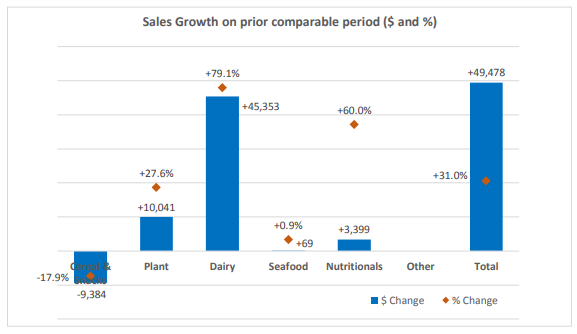

Key Business Unit Financial Performance In 1H FY19: Freedom Foods Group Limited stated that the dairy operations at Shepparton achieved significant sales growth, which reflects increasing demand in Australia, China and SE Asia. The earnings contribution witnessed an improvement through increased sales and factory utilisation. The company stated that the plant-based beverage operations had delivered increased sales, which reflects the growth in retail and food service brands.

Sales Growth (Source: Company Reports)

The company stated that specialty seafood sales were in line with the previous comparable period. Considering the increasing focus towards building the company’s brands, FNP substantially increased the investments towards brand building and marketing as well as in retail and other channel trade activities.

Understanding FPN’s Innovation Capabilities: Freedom Foods Group Limited stated that they would continue to be a leading innovator with respect to its chosen product and channel segments. The company has been deploying significantly towards the innovation capabilities throughout business groups, which includes the appointment of product development personnel. This investment, aligned to the capital investment towards the manufacturing capabilities, gives a strong base to accelerate the new product development pipelines.

Insights into FNP’s Liquidity and Finance Facilities: Freedom Foods Group Limited was holding cash of $9.7 million as at December 31, 2018, while total borrowings stood at $173.7 million, comprising the term facilities, equipment finance leases as well as working capital facilities. The company’s net debt, as at December 31, 2018, amounted to $164.0 million.

With respect to dividends, the company intends to pay only a 50% franked dividend for any dividends relating to FY19, reflecting likely reduced tax payments as it utilises the tax losses from acquisitions and accelerated tax depreciation benefits from investment phase.

What To Expect From FPN Moving Forward: Freedom Foods Group Limited had created a unique supply and manufacturing footprint with respect to its key categories. The company stated that its key brands Australia’s Own and Freedom Foods would be at the forefront of driving the returns from the innovation and manufacturing capabilities in the Australia and International markets. FNP had added that the growth in the sales and improving financial returns in Plant beverage business is reflecting the investment towards the new capabilities at the Ingleburn site in Sydney. As per the report, the site is anticipated to continue to deliver improvements as well as would further contribute materially to increases in the sales and profitability over the medium term as the company focus towards driving the brands in Australia and into SE Asia and China.

Actuals and Projections (Source: Company Reports)

Considering the large and significantly increasing base of the dairy volume within the company, the focus is towards driving a dairy business towards specialty and high value-added products. Also, the cereal and snacks business are strategically well placed in order to build a significant growth platform in multiple products, channels, and distribution throughout Australia/NZ, China, and SE Asia. As per the equity raising presentation dated May 23, 2019, the company has been witnessing robust demand throughout each of the key business units. Based on the current sales performance and with the company prioritising sales to domestic demand in the recent months, there are expectations that FY19 net sales revenues would be between $480 - $490 million, a rise of $127-$137 million or 36-39%.

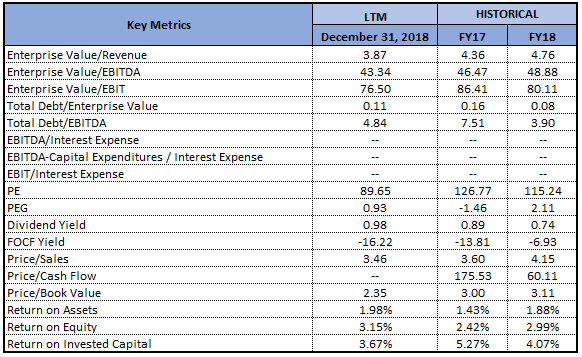

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies: EV/Sales Multiple Approach

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Freedom Foods Group Limited has been experiencing a robust demand throughout the business activities in Australia, China, and SE Asia. The growing demand with respect to dairy, plant-based beverage, cereal and snacks is reflecting positive impacts of the structural change in the Australian dairy industry, demand for products from the company’s expanded operational footprint and increasing brand penetration providing for the increased market share in the key channels and categories in Australia, SE Asia and China. Considering the stock’s performance, in the span of previous three months, the company’s stock has delivered the return of 12.33% while in the span of previous one month, the return stood at 0.39%. However, the company’s activities expose it primarily to the financial risk of changes in the foreign currency exchange rates as well as interest rates. Considering the growth potential in the business, we have valued the stock using relative valuation method, EV/Sales multiple and have arrived at the target price upside of about double-digit (in %). Hence, in view of the aforesaid facts and current trading level, we give a “Speculative Buy” rating on the stock at the current market price of A$4.970 per share (down 2.549% on 02 July 2019).

.png)

FNP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...