Kalkine has a fully transformed New Avatar.

Company Overview: Fluence Corporation Ltd, formerly Emefcy Group Ltd, is an Israel-based company that is engaged in providing water treatment solutions. It offers decentralized, packaged water and wastewater treatment solutions. Its solutions include decentralized treatment, desalination, reuse, waste-to-energy, water treatment, wastewater treatment, food and beverage processing. It provides services and support for project financing and after-sale support. The Company offers water treatment products and wastewater treatment products. Water treatment products include NIROBOX SW, NIROBOX BW, ultrafiltration and reverse osmosis. Wastewater treatment includes MABR, NIRBOX WW, packaged plants, aeration equipment and dissolved air flotation. The Company operates in approximately 70 countries.

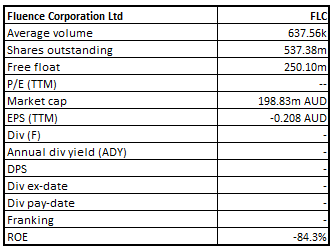

FLC Details

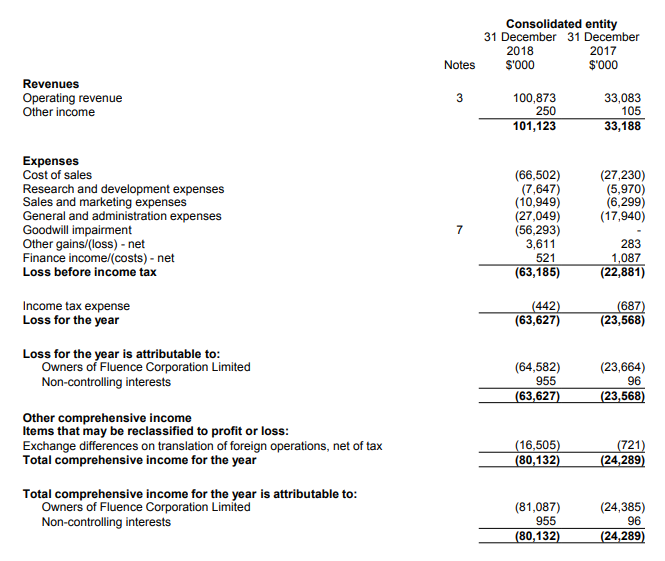

Significant Rise in Revenues: Fluence Corporation Limited (ASX: FLC) happens to be a leader when it comes to decentralized water, wastewater and reuse treatment markets while the stock’s market capitalization is of the order of $198.83 million. It lately garnered revenues amounting to US$100.8 million in the year ended December 2018 (Preliminary final report) reflecting the rise of 204.9% on the YoY basis. During the same period, the company’s operating revenue and other income amounted to US$101.1 million while, in the same period of the previous year, it was $33.1 million. The rise was mainly driven by increased operating revenue and other income. The company’s consolidated loss after tax amounted to US$64 million in the year ended December 2018 while, in the prior year, the loss was US$24 million. The consolidated loss included US$56 million of goodwill write off at the half-year ended June 2018. Also, the company witnessed strong improvement in FY 2018 on the YoY basis with respect to its key margins, thus, building further confidence in the company’s business strategies. The YoY improvement in FLC’s net margins demonstrates its capability to convert the top line into the bottom line. However, a YoY rise in operating margin reflects the execution of FLC’s cost-effective strategies. The company generated revenues amounting to US$43.7 million in Q4 FY 2018 which implies the rise of 73% on the YoY basis. The company had managed to improve the overall cost structure and also achieved favourable sales mix.

Therefore, it can be said that moving forward, FLC would mainly be aided by its geographical, industrial and technological diversification and by its strong cash generation capabilities. Also, the company’s robust financial position and improvements in market share would act as the tailwinds for the company’s long-term growth prospects.

Income Statement (Source: Company Reports)

Decent Liquidity Standing: At the end of December 2018, the company had cash and cash equivalents of US$39 million which can be considered at the decent levels and it might support the company for the execution of its strategic objectives. Also, as at December 31, 2018, the company’s borrowings were less than $1 million. After the 2018 results, the company has plans to work towards its current growth. Its smart solutions revenue in 2017 amounted to US$10 million while, in 2018, it witnessed the rise to US$22 million and the company expects that it would further rise in 2019.

Also, over the past three years to FY 2018 (i.e., FY 2016- FY 2018), the company’s cash receipts had witnessed significant improvement which is reflective of the company’s strong cash generation capabilities. The company’s robust financial position reflects wrapping up of US$25 million net proceeds which was the result of share placement and share purchase plan, securing of US$50 million project financing facility from Generate Capital and sales of NIROBOX™ Smart Packaged desalination plants which had helped in reducing the inventory. As at 31 December 2018, current ratio and quick ratio stood at 1.24x and 1.0x, respectively.

A Deeper Understanding of FLC’s Q4 FY 2018: In Q4 FY 2018, Fluence Corporation successfully executed on the global growth strategy and won new contracts in the new regions and industries and also managed to deliver an increased level of service and quality to its clients and industry partners. We expect that sealing new contracts in new regions would continue to strengthen the company’s pipeline and would help in increasing market share. Also, the proportion of annual recurring revenue booked has witnessed robust increase. The management expects that it provides substantial and sustainable growth opportunity for the company moving forward. The primary sources of revenues for FLC include smart products solutions, custom-engineered solutions, and recurring revenue and aftersales.

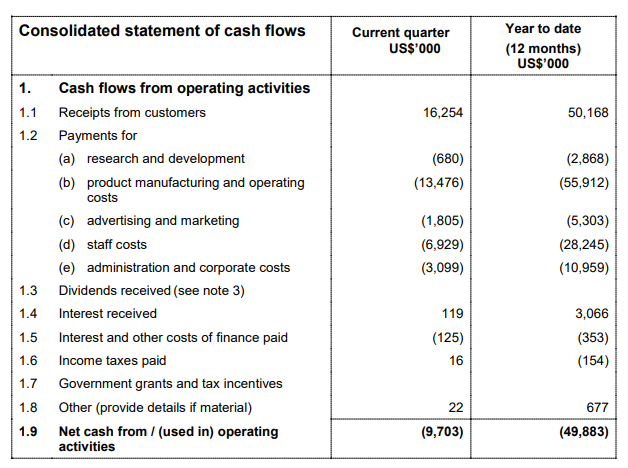

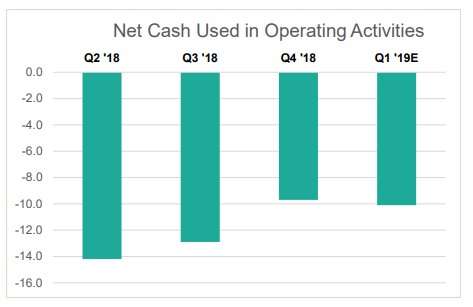

Coming to the cash flow report, the company’s net cash used from operating activities amounted to US$9.7 million in Q4 FY 2018 and result reflects US$3.2 million improvements as compared to previous quarter which reflects improved receivables’ collection, delivery of product in inventory and cost controls. FLC witnessed receipts from customers amounting to US$16.3 million in Q4 FY 2018 excluding the receipts from PDVSA for US$6.4 million revenue recognized in the fourth quarter for Portuguesa project, as contract value was prepaid in full.

Net cash used in operating activities (Source: Company Reports)

Signing of Contract in Ivory Coast- Growth Catalyst: Recently, FLC had made an announcement that they have signed a landmark €165 million commercial agreement with Federal Government of Ivory Coast which involves the turnkey supply of a 150,000 m3 /day surface-water treatment plant. The plant would be treating water from Lagune Aghien, Ivory Coast’s largest freshwater reserve near Abidjan, which happens to be dense with algae and other contaminants, to help meet the needs of fresh water. The contract happens to be conditional upon the arrangement of the export credit financing, which FLC is in the process of finalizing. The company’s management had stated that substantial contract award is a testament to FLC’s reputation as a global leader with respect to water treatment technology which is able to deliver optimal end-to-end custom engineered solutions. Hence, we presume that this deal might act as a growth catalyst for the company and support to improve financial profile in the upcoming years.

Validation of FLC’s MABR Technology: Earlier, Fluence had made an announcement that independent test results which have been gathered from its Stanford, California demonstration plant have been published, and the same validate compliance of FLC’s MABR technology with California’s Title 22 water recycling legislation. The company’s MABR demonstration plant is installed at Codiga Resource Recovery Center (CR2C) in Stanford, California, which has been operational since January 2018. Title 22 of California’s Water Recycling Criteria happens to be among strictest water treatment standards for water recycling and reuse in the US. According to the report published by the third party i.e., CR2C, the MABR technology system achieved the objectives of mean Total Nitrogen concentrations below 10mg/L and met T22 requirements as measured by Turbidity and Total Coliform in the Tertiary Effluent. Hence, the management is positive on its MABR technology which is ideally suited to address the toughest wastewater challenges in the United States and around the world.

FLC Got US$1.7 million Contract: Fluence Corporation had earlier announced that they have got US$1.7 million contract to supply its Smart Products Solutions for a prominent international beverage producer which happens to be long time repeat customer. The solution includes first Aspiral™ wastewater system which features FLC’s unique MABR technology and would be deployed in Latin America. Fluence Corporation expects that the project would be an important reference site in Latin America for other potential Aspiral™ customers.

Understanding Primary Sources of Revenue in Q4 FY 2018: With respect to Smart Products Solutions, the key factors include largest NIROBOX™ sale to-date in Egypt for the consideration of US$7.6 million with the units already in inventory which enables rapid deployment and US$8.4 million NIROBOX™ Seawater & installation for the Peru Build-Own-Operate-Transfer (or BOOT) project. With regards to recurring revenue and aftersales, the key sources include securing annual average recurring revenue for the consideration involving US$14.7 million at 31 December 2018. However, in custom-engineered solutions, a key factor to consider is PDVSA Portugesa project which is in Venezuela and is progressing as per schedule and is also nearing completion.

Drivers for Future: Fluence Corporation is inclined towards driving growth in smart products solutions and recurring revenue and aftermarket categories. In these, FLC has numerous competitive advantages, gets higher margins and it also sees significant large market opportunities. The custom-engineered plants have been a strong historical contributor to the revenues, and they are expected to be so moving forward. The company had managed to raise funds in a share placement and share purchase plan. These funds along with project financing facility which is now in place would be aiding FLC’s growth plans and its guidance of achieving sustainably EBITDA profitable quarter by 2019 end. Also, the company expects that net cash used in operating activities would be decreasing in the following quarters until break-even which is expected in Q4 2019. With respect to the current contracts, FLC anticipates US$17.3 million of cash inflows from customers in Q1 FY 2019 and a net operating cash outflow of US$10.1 million for the same period.

Expectations for Q1 FY 2019 (Source: Company Reports)

The company’s leading range with respect to smart products solutions, growing backlog on recurring revenue as well as technical expertise places FLC to tap the future growth opportunities. The robust sales pipeline in all regions of the world coupled with wrapping up of the existing project milestones, will help the company’s accelerated growth objectives for 2019. The rise in awareness of FLC’s brand and value proposition is aiding it in terms of having recurring orders and is also helping in garnering interest from the prospective customers and partners.

Stock Recommendation: On the daily chart of FLC, Moving Average Convergence Divergence or MACD has been used and default values were used for the purposes. After observation, it was noted that the MACD line has crossed the signal line and had moved in an upward direction after crossover which reflects bullishness.

Also, the company is expected to be supported by cost-effective approaches and a decent financial position which provides headroom for future growth. The company’s contract revenue backlog amounted to US$57.7 million at 31 December 2018 and FLC expects that most of the backlog might get converted into 2019 revenue. However, in the past five years, the company’s stock had delivered -58.89% return and in the previous one year, it delivered -8.64% return. In the past one month, it posted an 8.82% return. This shows that the stock faces some volatility. Hence, considering the aforesaid facts and current trading level with given growth prospects, we have a “Speculative Buy” recommendation on the stock at the current market price of A$0.360 per share (down 2.703% on March 08, 2019).

FLC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...