Company Overview: Flight Centre Travel Group Limited is engaged in travel retailing in both the leisure and corporate travel sector, and wholesaling. The Company's segments include Australia, United States, Europe, Rest of World and Other. The Europe segment includes businesses in the United Kingdom, Ireland and Netherlands. The United States segment includes businesses in the United States and Mexico. The Rest of world segment includes the aggregation of a range of geographic businesses. The Other segment includes Brisbane-based support businesses that support the global network. It operates retail, corporate and wholesale brands in Australia. Its leisure travel brands include Flight Centre, Escape Travel, Student Flights, Travel Associates and Cruiseabout. Its corporate business includes brands, such as Travel Money, Campus Travel and 4th Dimension. Its wholesale brands include Infinity Holidays and Explore Holidays. It is also engaged in activities, such as recruitment marketing and bike retailing.

.png)

FLT Details

Decent Performance in FY19: Flight Centre Travel Group Limited (ASX: FLT) is a mid-cap travel retailing company with the market capitalisation of circa $4.25 Bn as of 04 November 2019. The company posted a decent set of results for the year ended 30 June 2019 and recorded 8.8% growth in Total Transaction Value (TTV) to $23,727.78 Mn as compared to the prior year. In FY19, FLT exceeded record FY18 result by almost $2 Bn and achieved 23rd year of TTV growth in 24 years since listing. This reflects a further growth momentum in the near future. Revenue for the period increased by 4.5% on Y-o-Y to $3,055.26 Mn. EPS stood at 261.6 cents per share, exhibiting a modest growth of 0.2% on Y-o-Y basis. As at 30 June 2019, the company had a cash and cash equivalent of $1,172.25 Mn, debt to equity of 0.17x, net operating cash flow of $278.88 Mn, and free cash flow of $177.9 Mn. And, the company is expecting to maintain a robust balance sheet in order to ensure that it can reap the benefits of future growth opportunities and continue to deploy towards key business drivers across the economic cycle.

The company stated that the international businesses and corporate travel operations generally posted robust profit growth and is a positive sign for the future. This growth was more than offset by soft Australian results in fairly subdued trading cycle and during a period of disruption for the leisure business in particular. The higher dividend payments, that were supported by special dividend, followed the review of balance sheet early in FY19 and meant that the company has managed to return $310.2 million in terms of fully franked dividends to shareholders, in addition to going for a modest level of debt. The company is focusing on FY22 transformation program targets, and they are making decent progress towards TTV and cost margin goals.

.png)

FY19 Financial Summary (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Flight Centre Travel Group Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Key Metrics: The company’s gross margin in FY19 stood at 94.9%, which is higher than the industry median of 51.8%. Notably, during the same time period, FLT’s net margin stood at 8.6%. The company’s RoE stood at 17.8% in FY19, which is comfortably higher than the industry median of 11.5% and, therefore, it can be said that FLT has delivered higher returns to its shareholders as compared to the broader industry. FLT’s current ratio stood at 1.31x in FY19, which is higher than the industry median of 1.08x and, therefore, it can be said that the company is in a decent position to meet its short-term obligations when compared to the broader industry. Also, decent liquidity levels reflect that FLT could make deployments towards key strategic objectives, which could help it in long-term growth. The company’s Debt/Equity ratio stood at 0.17x, which is lower than the industry median of 0.46x and, thus, it can be said that FLT’s balance sheet is less leveraged as compared to the broader industry. Generally, the lower debt on a balance sheet reflects stability.

.png)

Key Metrics (Source: Thomson Reuters)

FLT Assumes Full Ownership of Ignite Travel Group: Flight Centre Travel Group Limited has recently published a release in which it stated that the company strengthened the Australian leisure business with 100% acquisition of growing Gold Coast-based Ignite Travel Group. The company was previously holding a 49% stake in the award-winning company, and the parties have decided to bring forward the full purchase of Ignite’s Australian and New Zealand businesses. This has been done to capitalise on the highly successful “readymade” holiday package model. FLT’s key personnel has stated that Ignite has been successful and its sales have witnessed a growth of over 40% per annum for the previous 2 years, and FLT is optimistic about the future potential in Australia as well as overseas.

Key Takeaways from Morgans Queensland Conference: In the presentation at Morgans Queensland conference, the Managing Director of FLT named Graham Turner stated that online leisure sales in the country doubled in 3 months to September 30, 2019, even though there was a relatively challenging trading climate. It was followed by robust online leisure sales growth in Australia and overseas during FY19. In the same period, the company posted a record $1.3 billion in TTV globally from leisure branded websites as well as dedicated online travel agency (or OTA) brands. The company’s key personnel stated that Jetmax OTAs, BYOjet and Aunt Betty, and flightcentre.com.au together garnered over $250 million in TTV in Q1 in Australia. The following image has been extracted from Morgans Queensland Conference presentation:

.png)

Diversity & Globalisation (Source: Company Reports)

Capital Management and Dividends: The company has been maintaining a conservative funding structure, which enables it to meet operational as well as regulatory requirements, and, at the same time, provides sufficient flexibility to finance growth, working capital requirements and future strategic opportunities. On February 20, 2019, the company has entered into the series of bilateral debt facilities amounting to $250,000,000 in order to give additional liquidity to finance the acquisitions.

.png)

Dividends (Source: Company Reports)

In recent years, the company initiated strategies in order to strengthen the balance sheet by increasing the general cash and maintaining moderate debt levels, and it has a view to creating greater shareholder value. At the time of determining dividend returns to shareholders, the Board of the company takes into consideration numerous factors, that include its expected cash requirements to finance growth and operational plans. The payments may vary from time to time and according to expected needs, the company targets to return to shareholders around 50 – 60% of NPAT. The company stated that special dividend amounting to 149.0 cents per fully paid ordinary share was announced on February 21, 2019, which was paid out of general cash. The combined interim and final dividend payments reflect $159,533,000 return to the shareholders and 60% of the company’s statutory NPAT. Notably, the combined payments imply 60% of underlying NPAT.

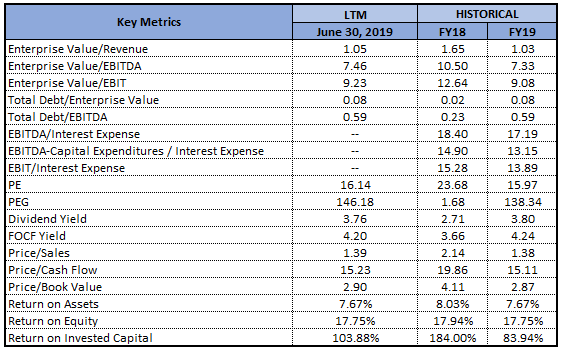

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1:Price to Cash Flow based Valuation:

.png)

Price to Cash Flow based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Method 2:EV/EBITDA Multiple Approach:

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, Peer related information for the calculation purposes include that of Corporate Travel Management Limited and Webjet Limited

What to Expect from FLT Moving Forward: The company’s key personnel stated that, while TTV has been increasing solidly early in FY20, the underlying profit will be below the prior corresponding period (or PCP) during the first half and is likely to be heavily weighted towards 2H FY20. It was mentioned that Thomas Cook’s high profile collapse in the UK had minimal impact on Flight Centre Travel Group Limited and its customers. However, the company is anticipated to incur in the order of $7 million in costs to ensure that its customers were re-accommodated and not adversely affected by collapse of Bentours and Tempo Holidays in Australia. The company is currently expecting to separate these costs from underlying results for FY20.

It was also stated that while TTV has been increasing in Australia, the company had not witnessed tangible benefits flowing from the recent interest rate cuts and tax refunds and that any benefits were expected to be witnessed later in FY20. However, there is an assumption that consumer confidence gets improved ahead of the year’s peak booking periods. The company anticipates to maintain the robust balance sheet in order to ensure that it can reap the benefits of future growth opportunities and can continue to deploy towards key business drivers across the economic cycle.

Stock Recommendation: On a YTD basis, the company’s stock has delivered a return of 3.73%, while in the time span of the previous six months, it posted a return of 9.63%. The company has been planning to disclose its FY20 guidance at the AGM in the month of November 2019, which happens to be in line with the normal practice. There are expectations that the results would be driven by corporate and international businesses, and improvement has also been expected in Australia. Over the full year, FLT has managed to record $278.9 million of operating cash inflow, in comparison to $314.3 million inflow during FY18. It stated that a YoY movement was because of the timing factors related to the staff pay (Australian leisure business introduced weekly pay system) as well as payments to the non-air suppliers. Based on the foregoing, we have valued the stock using two relative valuation methods, i.e., Price/Cash Flow and EV/EBITDA multiples, and arrived at a target price of high-single digit to low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of A$42.0 per share.

FLT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...