FXL, which leases equipment to consumers and business, stock was up over 10% year to date before June 22

nd but following the exit news of chief Tarek Robbiati the stock is now down 1% YTD. Investors certainly didn’t like the news, which though understandable, will only have a short-term impact on the stock price, and soon we could expect the company to hit earlier levels.

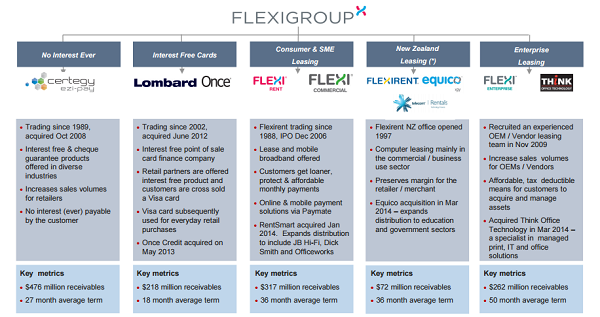

Group Overview (Source - Company Reports)

Mr. Robbiati, since taking up the role in January 2013, helped FXL with its profits along with a string of acquisitions of finance and leasing companies. Though the exit definitely raises growth concern into financial year 2015-2016, the board is already in action with an internal and external search to find a suitable replacement. We expect, FXL to find a suitable replacement soon, who will continue with the impressive growth in years to come. What’s interesting to note here is, on the day the company announced the exit of Mr. Robbiati, it also reaffirmed its cash net profit forecast for 2014/15 of $90-91 million. By this, the management wants to send out the signal to the stakeholders that the exit of Mr. Robbiati won’t impact the operations.

.png)

Financial Highlights (Source - Company Reports)

First half of the financial year has been strong for FXL with five divisions of the groups including business and individual equipment rental, lay-by plans and credit card finance, witnessing a growth in profits for the first time in over two years. FXL is determined to accelerate the growth in the second half of the financial year. For the same, it is investing to come up with products that meet the taste of this new generating, who prefer to pay with their smartphone. Such a shift in customers demand is seen as a major change in Australia's $50 billion consumer payments industry.

.png) NZ Leasing Source - Company Reports)

NZ Leasing Source - Company Reports)

For the first half of the year, FXL increased its net profit $34.6 million to of $38.5 million. The increase in the profit was primarily due to a 9% rise in the volumes to $587 million and a 10% gain in the receivables to $1.35 billion. FXL’s New Zealand division witnessed the biggest jump in the profits of 23% to $3.2 million, with Certegy emerging as the biggest earner. The growth in New Zealand was mainly the result of Equico business purchase, organic growth also played its part.

Cost to income ratio (Source - Company Reports)

Cost to income ratio (Source - Company Reports)

For FXL, upside is also expected following the government’s initiatives to push small business purchases, towards the end of the year. FXL, which also finance big retailers' interest-free repayment offers to customers, is poised well to benefit from this initiative as the firm is high on the consumer confidence due to its Rent-Try-Buy product and SmartWay Leasing system.

Flexigroup daily chart (Source - Thomson Reuters)

Flexigroup daily chart (Source - Thomson Reuters)

Further, its dividend yield of over 5%, provides another good reason to pick this stock. Apart from this, FXL has been consistently growing its revenue streams and improving cash flows. For the first half of the 2015, the company reported an impressive 8% rise in the EPS while interim dividend jumped 9%, along with a robust forward outlook. The robust performance can be majorly attributed to the company’s Interest Free Cards and No Interest Ever business groups.

Over the past few years, FXL has increased its focus on the digital finance opportunity, and the management is confident that the company is on track to dominate digital finance in Australia and New Zealand. While preparing for the cashless future, the company is eyeing expansion in the flourishing electronic wallet technology.

Over the years, FXL has been making efforts to push its growth by taking support of the New Zealand economy. For the 1H15, the company’s New Zealand Leasing division reported a 23% rise in the cash net profit after tax (NPAT). In March, FXL revealed that following the acquisition of market leader Telecom Rentals for $NZ106 million, it would become the biggest IT leasing company in New Zealand. The acquisition is expected to contribute around $3 million to NPAT in 2016 financial year. The full-year NPAT for 2015 is expected to rise by 7.6%. Previous to this deal, FXL made its first New Zealand acquisition, buying technology leasing group Equico for an undisclosed amount.

To diversify its retail partners, over the past few years, FXL acquired numerous businesses such as Harvey Norman and Dick Smith. Also, the company has expanded its roots into business equipment leasing, mobile broadband and online payments. Its recent acquisitions RentSmart and Once and Lombard retail credit cards are already contributing to the top line. It’s not just stopping here, it has considered numerous other takeover targets like GE Capital's consumer finance business, and probably company Fisher & Paykal's finance arm.

FXL is currently trading at a PE of 14.6, which is well below the competitors and the industry average of around 20. This along with a yield of over 5% is one of the highest in the industry. The consumer segment for the group is back to profitability, cost of funds are also on a decline and its receivables gained more than 10% in the first half of 2015, all these factors and more (such as potential acquisitions, robust growth in NZ, etc.), position FXL well to expand its growth in the second half of 2015 and beyond. Also, the recent decline in the stock price following the exit news of Mr. Robbiati, provides a good buying opportunity to the investors.

Based on the above the reasoning, we recommend FXL as a BUY at the current price of $2.97.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...