Company Overview - FlexiGroup Limited is a diversified financial services company. The Company provides no interest ever, leasing, vendor finance programs, interest free and visa cards, mobile broadband, lay-by and other payment solutions to consumers and businesses. It primarily operates through four core business areas: interest free (no interest ever and take home lay by plans) and cheque guarantee services offered through diverse merchants by Certegy; consumer and small and medium sized enterprise (sme) (leases), which offers leasing products to consumers through key partners including Australian retailers; enterprise offers leases (commercial and larger sized transactions) through vendor programs and direct to medium and large businesses, and interest free cards business has been complimented by the acquisition of Once Credit Pty Limited.

Analysis - FlexiGroup (FXL), the financial services’ company which is known to operate via five core business areas, has reported a robust performance in FY14. The recent AGM of November 2014 further elucidated FXL’s strong growth in profit, volume and receivables supporting its strategy of diversification.

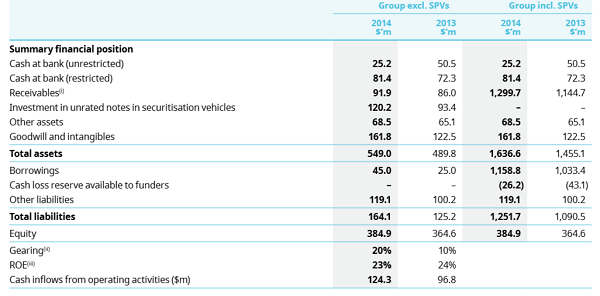

Financial Performance (Source – Company Reports)

Financial Performance (Source – Company Reports)

The Interest Free Cards business provides personal finance products including store finance or a Visa card for the Australian market. The Enterprise business has been expanded in 2014 in view of the acquisition of the Think Office Technology (TOT) to offer a full suite of office equipment, tailored print services, cloud computing solutions, etc. across regional Queensland. The acquisition of RentSmart ANZ added scale while providing a wider distribution channel to the Consumer and SME leasing business.

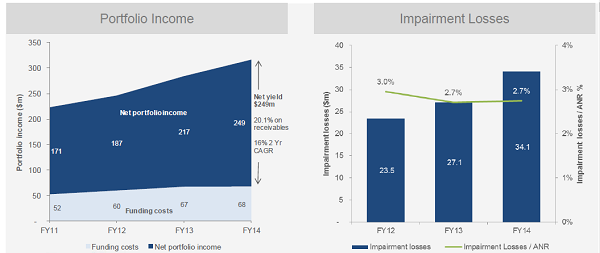

FXL 3-Year Financial Performance Overview (Source – Company Reports)

FXL 3-Year Financial Performance Overview (Source – Company Reports)

Looking at the FY14 performance, FXL reported a statutory profit of $57.6m, down by 13% year on year. Factors such as several one off, non-recurring expenses relating to impairment of goodwill and IT software, integration expenses, etc. reduced the statutory profit. FXL recently brought forward a $2.5m after-tax one-off loss provision relating to the residual value for an individual major retail customer. However, cash NPAT increased by 18% to $85.0m, which was steered by volume increase of 19% and net receivables of 13%. Cash EPS increased by 12% to 28.0 cents per share on the prior comparative period, indicating the effect of higher Cash NPAT in 2014.

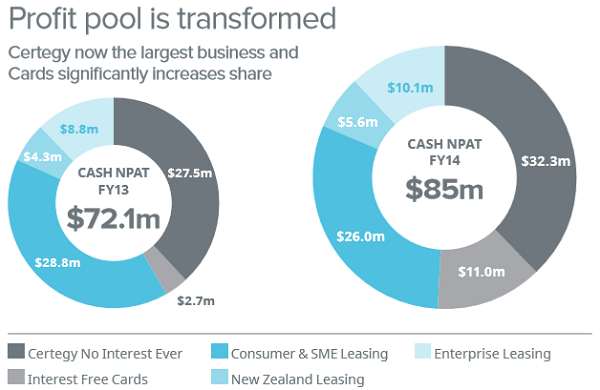

Business-wise Cash NPAT (Source – Company Reports)

Business-wise Cash NPAT (Source – Company Reports)

There was a 15% increase in net portfolio income to $249.1m driven by a 13% increase in receivables due to growth in No Interest Ever, New Zealand Leasing business, Enterprise and Interest Free Cards. However, a weak performance in the Consumer and SME (Leases) segment lowered the increase witnessed in aforementioned segments. There was a decline in performance for the mobile broadband (Blink) business in view of low volumes during the year.

FXL’s impairment losses increased to $34.1m. However, impairment losses were reported to be stable at 2.7% when measured as percentage of average receivables. This is indicative of a healthy result. There was an 18% increase in operating expenses to $109.5m driven by costs to support volume growth, operating costs, acquisition costs for RentSmart and TOT, one off strategy review costs and acquired business integration costs. Further, impairment of goodwill and IT software was at $12.5m.

The Company committed capital expenditure to align its IT systems to the growth strategy with an expectation to enable FXL achieve volume increase and future cash.

The acquisition of the Australian and New Zealand businesses of ThinkSmart Ltd (‘RentSmart ANZ’) for $42.4m, facilitated FXL to have access to new relationships, enhance distribution channels and provide strong growth potential from selling the Company products into new retailers. Similarly, the acquisition of TOT (March 2014) allowed FXL to consolidate and grow in the print and managed services industry. Moreover, the completion of the acquisition of certain assets and the business of Equico Limited, a New Zealand based leasing company (March 2014) allowed expansion of leasing footprint within the New Zealand market.

For the Consumer and SME Leasing (Australia, including Ireland), the cash NPAT was $26.0m, a reduction of 10% on the prior comparative period based on decrease in net portfolio income. The lowering electronic products (e.g. computers) prices continue to have an effect on the volume. There was 1% increase in sales volume to $189m (2013 - $187m) in spite of the difficult consumer computer leasing market driven by a decrease in consumer demand and a decline in computers and other hardware prices. The decline in consumer market is equipoised by SME market.

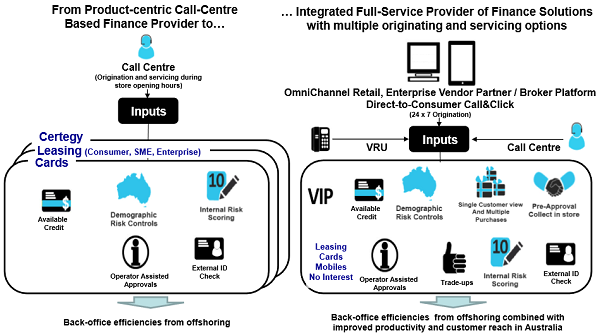

Business Integration (Source – Company Reports)

Business Integration (Source – Company Reports)

For New Zealand Leasing business, cash NPAT is $5.6m which is an increase of 30% on the prior comparative period. This was driven by 29% increase in net portfolio income to $14.3m which was mainly due to strong growth in all income streams. There was a 14% decrease in impairment losses to $0.6m steered by effective arrears management and the mix of receivables toward a lower risk for larger commercial customers. There is a 30% increase in operating expense to $6.1m owing to incremental post acquisition costs relating to Equico and cost to support volume growth. Sales volume increased by 31% to $38m.

No Interest Ever (Certegy) business witnessed cash NPAT of $32.3m indicating a 17% increase on the prior comparative period. This increase was steered by net portfolio income increase of 13% to $85.1m. The revenue growth has been driven by repeat volumes attributable to the VIP loyalty card program initiatives and thrust in solar even with reduced government subsidies. Impairment losses increased with portfolio growth to $13.5m and the operating expenses also increased slightly by 3% to $25.5m. Sales volume increased by 3% to $507m as solar volumes were successfully stabilized.

For the Enterprise business, cash NPAT of $10.1m was supported by a 15% increase on the prior comparative period. The increase was owing to net portfolio income increase of 27% to $27.4m, largely driven by a 34% growth in receivables and 32% in volumes. TOT acquisition led to strong results. There was an increase in impairment losses to $2.4m in line with the continued growth in the receivables portfolio. Operating expenses increased by 24% to $9.8m and sales volume increased by 32% to $149m largely as a result of consistent volumes through new strategic partnerships and increased penetration within existing vendors.

For the Interest Free Cards business, cash NPAT was $11.0m (2013 - $2.7m) attributable to the full year contribution made by Once Credit (2013 - 1 month) and synergy realization resulting from the integration of Lombard and Once. Impairment losses were $5.3m (2013 - $1.0m) indicating 2.7% of average net receivables. Operating expenses were $15.3m (2013 - $7.9m) driven by the impact of Once Credit and growth initiatives. Sales volume of $200m were reported.

FXL has a conservative funding strategy with wholesale debt facilities in place with five Australian trading banks and a major institutional entity along with numerous institutional investors in its Asset Backed Securities (ABS) program. FXL’s $100m of corporate debt facilities were drawn to $45m and these facilities are secured by the Company’s assets with a maturity date in 2017.

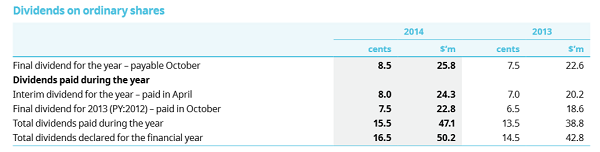

Dividends on Ordinary Share (Source – Company Reports)

Dividends on Ordinary Share (Source – Company Reports)

The total shareholder dividend grew by 14% to 16.5 cents (per share) and was paid after declaration of a fully franked final dividend of 8.5 cents (compared to a 7.5 cents final dividend last year).

The Company expects mid, single-digit growth for FY2015 with cash NPAT between $90m–$91m and with higher growth returns expected in the following years. Although, the Company highlighted that the first four months have seen tough trading conditions, there is still a ray of hope for positive outcome. The key drivers are expected to entail solid performance from Certegy, growth and improved returns from Interest Free Cards with completion of an integrated Once and Lombard IT platform, volume uplift in Consumer and SME Leasing, strong growth in New Zealand Leasing volume owing to the low-risk SME sector and benefits emanating from Equico acquisition, and scaling-up in Enterprise Leasing with the digital originations platform rolled-out in FY2014.

Flexigroup Daily Chart (Source - Thomson Reuters)

Flexigroup Daily Chart (Source - Thomson Reuters)

Moreover, new products and distribution relationships will drive growth in FY2015. New product offerings through the SmartWay and FlexiWay brands are expected to further drive volume uplift. FXL’s long-term agreement with Dick Smith Electronics for leasing will set a platform as a business finance provider. Expansion of product offerings into the mobile and tablet market is another door to opportunities. Then FlexiCommercial brand launched in 2H14 will help build strong customer value proposition.

The entire game-plan looks interesting, and accordingly, we put a

BUY recommendation for this stock at the current price of $3.23.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...