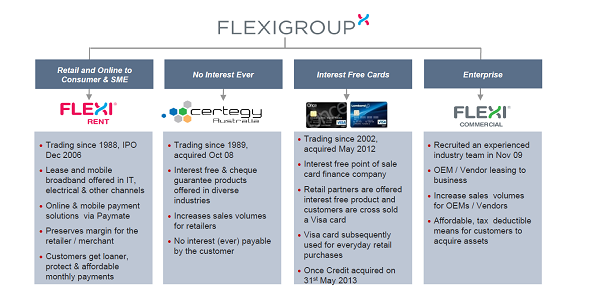

Company Overview - FlexiGroup Limited is a diversified financial services company. The Company provides no interest ever, leasing, vendor finance programs, interest free and visa cards, mobile broadband, lay-by and other payment solutions to consumers and businesses. It primarily operates through four core business areas: interest free (no interest ever and take home lay by plans) and cheque guarantee services offered through diverse merchants by Certegy; consumer and small and medium sized enterprise (sme) (leases), which offers leasing products to consumers through key partners including Australian retailers; enterprise offers leases (commercial and larger sized transactions) through vendor programs and direct to medium and large businesses, and interest free cards business has been complimented by the acquisition of Once Credit Pty Limited.

Analysis – FXL reported 1H14 cash Net Profit after Tax of $39m, up 20% year on year. Dividend of 8.0 cents per share fully franked was up from 7.0 cents per share in the previous corresponding period. A significant uplift in the Interest free cards was a standout as was the ability to hold Certegy volumes after the wind back of the government rebates. Guidance for cash Net Profit after Tax of $84 - $86m remains in place, seeing the company on track for its sixth successive year of double digit cash earnings per share growth. We remain positive on FXL with an outstanding track record of earnings growth and value accretive acquisitions. Management has shown a commitment to new product innovation and have done a good job at balancing growth of receivables while limiting impairment losses. We believe strong cashflow generation and conservative gearing will see FXL well placed in a market where it is becoming increasingly important for companies to deliver on earnings to justify current valuations.

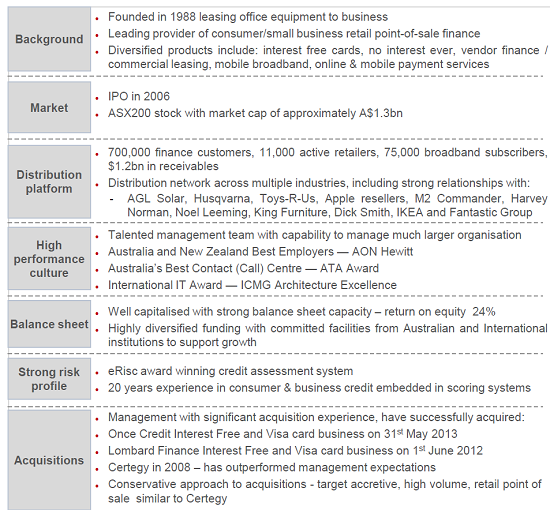

FXL Overview (Source - Company Reports)

FXL Overview (Source - Company Reports)

Established in 1988, Flexigroup is a specialist finance business providing retail point of sale leasing and lending services for consumers and SME’s in Australia and New Zealand. Flexigroup’s flagship leasing product competes with point of sale finance alternatives such as credit cards and interest free plans but differentiates itself through its marketing lead approach that shares the benefit of leasing products with the consumer, sales person and retail chain. Industry outlook is positive driven by increasing consumer confidence and broader recovery in domestic economic conditions. An improving domestic economic outlook bodes well for FXL via greater organic volume growth from retail and commercial partners across the suite of products the business now offers. There are also a number of internal initiatives likely to assist top and bottom line growth, including new product innovation, increased product penetration, cost improvements and further selective acquisitions.

Diversified product suite (Source - Company Reports)

Diversified product suite (Source - Company Reports)

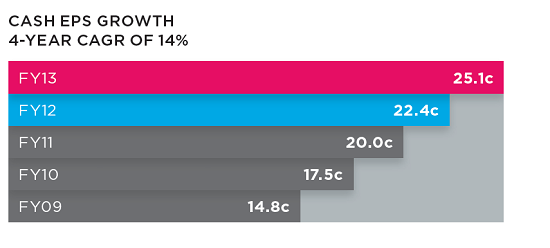

A significant uplift in Interest Free Cards was a standout, with cash NPAT of $5m well up from $1m in 1H13 and $1.7m in 2H13. A sustained strong performance from Certegy was also a positive given the wind back of government rebates in solar. Enterprise saw encouraging growth in receivables of 26% year on year. FXL’s funding position remains incredibly favorable with the average cost of debt at 6.3% in 1H14. Earnings growth remains a strong feature of the FXL. However we note that while cash net profit after tax has grown at a 5 year compound annual growth rate of 21%, cash earnings per share has grown at a compound annual growth rate of 14% over the same period given the increase in shares on issue. More disclosure has been provided on Certegy, specifically in Solar, with management remaining upbeat around the opportunities in this market. The shift in mix away from consumer towards Small & Medium Enterprises sees slightly lower margins in Flexirent, although this also sees lower level of impairments.

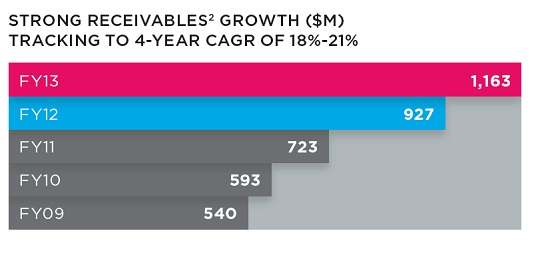

Strong Receivables Growth (Source - Company Reports)

Strong Receivables Growth (Source - Company Reports)

In terms of leverage to the broader consumer/retail recovery, FXL now has around 12,000 retail partners up from 11,000 in FY11 – FY13 and 4400 back in 2006 when the business went public. We outline key estimated exposures for FXL’s receivables book. Consumer electronics (computers, tablets, TV’s, appliances) make up around 27% of overall receivables. Solar makes up 17% of receivables while home improvement and furnishings (indoor and outdoor) together account for 22%. While there are still structural issues in consumer electronics in terms of lower prices and a shift to tablets from laptops, the overall portfolio is reasonable well placed to capture an improvement in the domestic retail and housing environment.

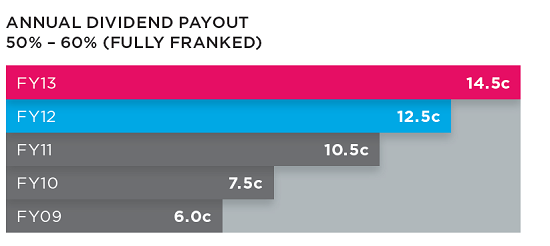

Annual dividend payout (Source - Company Reports)

Annual dividend payout (Source - Company Reports)

We retain a positive view on FXL and believe at current levels the stock represents attractive value. The superior growth profile we have seen in prior years looks tougher to achieve post FY15 in the absence of new product initiatives or acquisitions. However we feel that the market is currently discounting the cyclical leverage to an improving consumer in FXL’s base business as well as growth opportunities in Enterprise and Interest Free Credit Cards. We also highlight FXL’s strong track record of innovation, product leadership, cross selling and sales generation as well as disciplined, value accretive acquisitions. The key risk to the story remains a sharp increase in unemployment or interest rates which would likely see a rise in impairments/higher cost of funds. Other risks include solar volumes dropping off more than current expectations, additional competitive pressures driving margin compression and an increasing amount of residual risks as Enterprise grows within the portfolio.

Cash EPS growth (Sourcce - Company Reports)

Cash EPS growth (Sourcce - Company Reports)

FXL has done an excellent job growing the book in recent years with a 5 year compound annual growth rate of 20% in terms of average receivables. With the book now coming off a larger base, core consumer FlexiRent volumes maturing and residential solar installations stabilizing, the high levels of growth experienced to date will be difficult to replicate in coming years. While the issue has been a focus for investors, we feel the market is discounting cyclical tailwinds likely to support FXL’s underlying business, additional growth avenues in Interest Free Credit Cards and Enterprise/SME leasing and further opportunities in solar. M&A will remain a feature and is a natural part of FXL’s growth strategy, with the company having a strong track record for disciplined, value accretive acquisitions. We like the FXL story and reiterate our BUY on the stock at the current price of $3.42.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...