Kalkine has a fully transformed New Avatar.

Company Overview: EVENT Hospitality and Entertainment Limited, formerly Amalgamated Holdings Limited, is engaged in cinema exhibition operations; ownership, operation and management of hotels and resorts in Australia and Overseas, and property development. The Company's principal activities include cinema exhibition operations in Australia, including technology equipment supply and servicing, and the State Theatre; cinema exhibition operations in New Zealand and Fiji; cinema exhibition operations in Germany; operation of the Thredbo resort, including property development activities, and investment properties and investment in shares in listed and unlisted companies. The Company's segments include Entertainment Australia, Entertainment New Zealand, Entertainment Germany, Hotels and Resorts, Thredbo Alpine Resort, and Property and Other Investments. The Company has operations in Australia, New Zealand, Fiji and Germany.

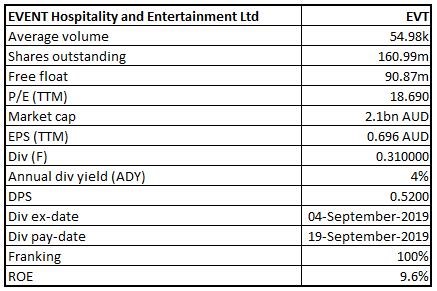

EVT Details

Decent Performance in FY19: EVENT Hospitality & Entertainment Limited (ASX: EVT) is an Australian company, which operates cinemas, hotels, and resorts in Australia, New Zealand, and Germany. As on November 7, 2019, the market capitalisation of the company stood at ~A$2.1 billion. Amidst certain challenges, the company has delivered decent FY19 results, driven by the continued strength from Hotels, Thredbo, & New Zealand cinemas, offset by a relatively weaker 2H performance from Australian cinema market. During FY19, revenue (including other income) and statutory NPAT, including discontinued operations, were recorded at $1,009.309 Mn and $111.889 Mn, respectively. Statutory NPAT is consistent with the prior year. It stated that the Hotels result was particularly pleasing with growth achieved on a record prior year profit despite headwinds in the key hotel markets with new supply.

With respect to the dividends, the Board has approved fully franked final dividend for the year amounting to 31 cents per share. The total fully franked dividend stood at 52 cents per share, which is consistent as compared to the prior year. It needs to be noted that, since 2001, the total dividend of the company has witnessed a rise from 10 cents to current 52 cents per share and, thus, it can be said that EVT has been maintaining its focus towards shareholders’ returns irrespective of market conditions. The company’s Board has chosen to maintain the dividend policy, which is mindful of the needs and expectations of the shareholders, and also gives expansion opportunities for businesses and continuity of earnings for shareholders and group. The company’s total cash balance, excluding the discontinued operations, at June 30, 2019, amounted to $72 million and total debt figure stood at $377 million that positions the company with modest gearing level and with substantial headroom in terms of available facilities which was $168 million. The Board of the company continues to review, assess and monitor appropriate capital management initiatives and strategies, and this might help the overall company moving forward.

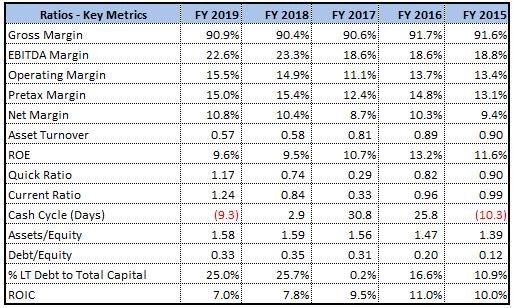

Over the period of FY15-FY19, the company has witnessed an improvement in margins. EBITDA margin has improved from 18.8% in FY15 to 22.6% in FY19. Net margins also increased from 9.4% in FY15 to 10.8% in FY19. Operating margins at 15.5% in FY19 reflect an increment of 210 basis points from 13.4% in FY15, indicating that the company has a consistent check on cost factors.

The company would continue to generate robust cash flows and maintain a robust balance sheet, which could help act as tailwinds for long-term growth. It might also acquire assets, which enhance property portfolio and complement its operating businesses, including evaluating the growth opportunities in new segments with respect to the industries it carries out operations. Considering these parameters, we have valued the stock using a relative valuation method, i.e., EV/EBITDA multiple, and 3-year average P/E market multiples of ~19.23x to FY20E consensus EPS of $0.71 and have arrived at a target price upside of high single-digit to low double-digit growth (in percentage term). At CMP of $13.03, the stock of the company is trading at P/E multiple 18.35x of FY20E EPS.

.png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters)

Decent Position of Key Margins: The company’s net margin stood at 10.8% in FY19, which is higher than FY18 figure of 10.4% and, therefore, it can be said that EVT is possessing better capabilities to convert its top-line into the bottom-line as compared to the broader industry. Notably, the company’s gross margin stood at 90.9% in FY19, which is higher than the previous year figure of 90.4%. The company’s RoE stood at 9.6% in FY19 as compared to FY18 figure of 9.5% and, therefore, it looks like that EVT has delivered improved returns to its shareholders in FY19 as compared to the previous year.

The company’s current ratio stood at 1.24x in FY19 as compared to FY18 figure of 0.84x and, therefore, it can be said that EVT is possessing decent capabilities to meet its short-term obligations. Also, a decent liquidity position places the company well to make deployments towards strategic business objectives, which can help it in achieving long-term growth. The company’s Debt/Equity ratio stood at 0.33x in FY19, which is lower than FY18 figure of 0.35x and, therefore, it can be said that the company has managed to deleverage its balance sheet. Generally, lower debt on the balance sheet reflects stability and gives the company an opportunity to focus on long-term growth objectives.

Key Metrics (Source: Thomson Reuters)

Key Takeaways from Annual General Meeting of Shareholders: The company’s Chairman stated that, in addition to the group’s major property developments, numerous upgrades and improvements have been planned at its Thredbo Alpine Resort and other identified cinema as well as hotel properties. The company’s CEO stated that the company posted earnings growth throughout Hotels and Resorts, Entertainment New Zealand, and Thredbo divisions. However, Entertainment Australia was impacted by genre mix of films, less screen advertising, new sites, which are yet to mature and impact of new revenue accounting standard on the gift voucher breakage revenue. In Entertainment Australia, the revenue was relatively flat, and this was achieved despite a less desirable genre mix of films for the audiences.

The company mentioned that Hotels and Resorts division posted record earnings result within the more competitive market and the revenue was up 5% to $353 million, which was because of new hotel openings (QT Perth and Atura Adelaide Airport), growth in conference and events, and rise witnessed in food and beverage revenues. The like-for-like growth was also witnessed throughout all the key metrics (like occupancy, average room rate and revpar). It was witnessed even though there was closing of Rydges Queenstown wings late in the month of February 2019 because of seismic rating issues that impacted the result by an estimated $1.7 Mn. The company’s CEO added that Thredbo witnessed record result, and the revenue rose 12% to $81.8 million while its EBITDA increased by 12.5% to $28.9 million. Notably, the normalised profit rose by 14.6% to $25 million. This was because of the strong 2018 snow season with consistent snowfall and snowmaking, which drove higher visitation and improved yield. However, strong food and beverage revenues made a contribution to overall growth.

.png)

Hotels & Resorts Business- Financial Highlights (Source: Company Reports)

Decent Dividend-Related Parameters Might Attract Investors: The company’s Board approved a fully franked final dividend amounting to 31 cents per share. Resultantly, its total fully franked dividend amounted to 52 cents per share that is consistent with the prior year. Since 2001, total dividends of the company have increased from 10 cents to current 52 cents per share and, thus, it can be said that EVT has been maintaining focus towards shareholders’ returns.

The company manages a capital with the objective of maintaining robust capital base so that investor, creditor and market confidence can be maintained and to have capacity to reap the benefits of opportunities, which would be enhancing existing businesses and enable future growth and expansion. The Board of the company also monitors return on capital, which is defined as operating profit after income tax divided by the shareholders’ equity and long-term debt. It also monitors the gearing ratio.

.png)

Key Parameters (Source: Company Reports)

Key Update: EVENT Hospitality & Entertainment Limited has recently made an announcement that Ken Chapman has resigned from the post of an independent non-executive director.

What to Expect from EVT Moving Forward: In Australia, there are expectations of screen upgrades which would be commenced at priority locations in this financial year, and it includes George Street, Macquarie, Chermside, Robina, Tuggerah, Shellharbour and Toowoomba Central. In New Zealand, the company is planning to open a new cinema complex in Newmarket, Auckland, in early 2020, which incorporates the group’s new Boutique premium cinema concept as well as multi-seating Vmax and traditional auditoria. It also stated that upgrades are underway at Event Cinemas Queen Street and Westgate in Auckland and in Albany and Manukau. All these are expected to be completed during 2020 financial year.

The company stated that, in Thredbo, the development plans in order to increase the capacity and continue to improve skier experience are advanced. In the month of May, a soft upgrade to Thredbo Alpine Hotel and outdoor venues was wrapped up, while Merritts Chairlift would be replaced with the high-speed gondola in time for 2020 ski season.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/EBITDA Multiple Approach

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

.png)

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: In the span of previous three months, the company’s stock price has witnessed a rise of 8.24% and, at the current market price of A$13.030 per share, the annual dividend yield stood at 4%. For group and within each division, the company is focussed towards 3 strategic priorities for the operating businesses, i.e., 1) increasing the existing revenue, via smarter pricing, better sales practices and focus towards the high margin products, 2) maximising the asset performance, through innovating and upgrading priority locations, deploying towards key property developments and acquiring new assets which have the potential to deliver immediate positive yields and can be developed into hotels, and 3) business transformation, i.e., reducing the duplication, increasing automation, digital capability and performance. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., EV/EBITDA multiple, and 3-year average P/E market multiples of ~19.23x to FY20E consensus EPS of $0.71 and have arrived at a target price upside of high single-digit to low double-digit growth (in percentage term). Hence, we give a “Buy” recommendation on the stock at the current market price of $13.030 (up 0.154% on 07 November 2019).

EVT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...