Company Overview: EVENT Hospitality and Entertainment Limited, formerly Amalgamated Holdings Limited, is engaged in cinema exhibition operations; ownership, operation and management of hotels and resorts in Australia and Overseas, and property development. The Company's principal activities include cinema exhibition operations in Australia, including technology equipment supply and servicing, and the State Theatre; cinema exhibition operations in New Zealand and Fiji; cinema exhibition operations in Germany; operation of the Thredbo resort, including property development activities, and investment properties and investment in shares in listed and unlisted companies. The Company's segments include Entertainment Australia, Entertainment New Zealand, Entertainment Germany, Hotels and Resorts, Thredbo Alpine Resort, and Property and Other Investments. The Company has operations in Australia, New Zealand, Fiji and Germany.

.png)

EVT Details

Decent Results Supported Dividend Payments: EVENT Hospitality & Entertainment Limited (ASX: EVT) is engaged in the business of motion picture exhibition, operation of hotels and restaurants, ownership and operation of Thredbo Alpine Resort, ownership of cinema, hotel and other rental properties. As on December 19, 2019, the market capitalisation of EVT stood at $2.11 billion. The company released a decent set of numbers for FY19, wherein revenue from continuing operations increased by 2% to $998 million, and statutory net profit after tax (including discontinued operations) was consistent on YoY basis to $111.9 Mn. Resultantly, basic earnings per share stood at 69.6 cents per share. The company’s results were supported by strength from Hotels, Thredbo, and New Zealand cinemas. However, the impact was offset by the relatively weaker 2H performance from its Australian cinema market. The Hotels' result were strong as the growth was achieved on the record prior-year profit amidst headwinds witnessed in the key hotel markets. Moving forward, the company is expected to focus on growing its existing business revenue, maximising its asset performance and business transformation.

The company has delivered growth in the earnings throughout Hotels and Resorts, Entertainment New Zealand, and Thredbo divisions. On the other hand, Entertainment Australia business segment was impacted by the genre mix of films, less screen advertising, new sites which are yet to mature and an impact of new revenue accounting standard on gift voucher breakage revenue. Considering the decent performance in FY 2019, the company managed to declare a fully franked final dividend amounting to 31 cps, and as a result, the total dividends for FY 2019 come out to 52 cps, which is consistent on the previous year. The company’s dividends have increased from 45 cps in FY 2015 to 52 cps in FY 2019 and, therefore, it can be said that EVT is possessing capabilities, which are sound enough deliver returns to shareholders across different business cycles. Based on the current market price of $13.000, the stock is trading at P/E multiple of ~18.73x at FY20E EPS.

There are expectations that decent standing with respect to liquidity position, YoY improvement in its RoE, capabilities to convert its top-line into the bottom-line and focus towards business transformation might help the company in gaining traction among the market participants..png)

Key Financial Highlights (A$ Mn) (Source: Company Reports, Thomson Reuters)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in EVT:.png)

Top 10 Shareholders (Source: Thomson Reuters)

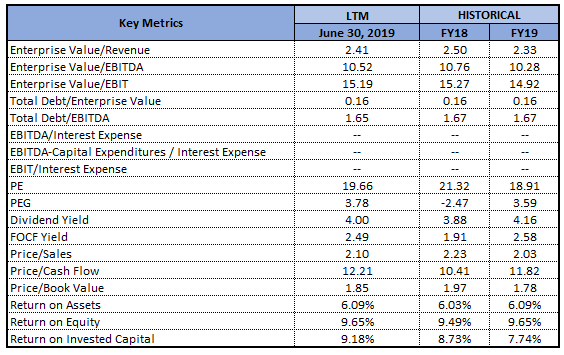

Decent Position From Margins’ Perspective: EVT has a net margin of 10.8% in FY 2019, which reflects a marginal rise from FY 2018 figure of 10.4% and, therefore, it can be said that the company is possessing respectable capabilities to convert its top-line into the bottom-line. The company’s gross and operating margin stood at 90.9% and 15.5%, respectively. Considering an improvement in operating margin in FY 2019 on YoY basis, it can be said that EVT is possessing respectable operational capabilities which could help it in witnessing decent performance moving forward..png)

Key Metrics (Source: Thomson Reuters)

The company’s RoE stood at 9.6% in FY 2019, which reflects a marginal rise from FY 2018 figure of 9.5% and, therefore, it can be said that EVT is providing decent returns to its shareholders, which could help it in attracting the attention of market participants. From the liquidity standpoint, the company is having decent standing, which is evidenced by its current ratio of 1.24x in FY 2019 as compared to 0.84x in FY 2018. Thus, it can be said that EVT is well-placed to meet its short-term obligations, and it has capabilities to make further deployments towards strategic growth objectives. Debt/Equity ratio stood at 0.33x in FY 2019, which is lower as compared to FY 2018 figure of 0.35x and, therefore, it can be said that EVT has deleveraged its balance sheet. Lower debt on a balance sheet reflects that company could focus towards its growth prospects.

How New Zealand Entertainment Business Performed: The company’s New Zealand Entertainment revenue amounted to $89.8 million, reflecting an increase of 5.3% on the prior year. However, New Zealand nationwide box office rose 1.4%, and the company out-performed the market, and the box office revenue rose 2.7%. Marketshare also rose 0.59 percentage points as compared to the prior year, and half of this share increase relates to the new site opening in Tauranga..png)

Entertainment- New Zealand (Source: Company Reports)

The normalised PBIT of the business rose by 9.6% after adjusting for the impact of $2.0 million loss of profits booked in the previous year for the closure of Queensgate cinema. The company also added that New Tauranga cinema happens to be a success and new concepts have been generating positive earnings from 1st month.

Hotels Revenue Rose 4.9% YoY: The company stated that the overall Hotels revenue amounted to $353.4 million, reflecting a rise of 4.9% on YoY basis which was mainly because of 2 new hotel openings, which includes QT Perth and Atura Adelaide Airport, growth which was encountered in the conference and event revenues as well as in food and beverage revenue. Also, fee income, from the existing managed hotels and new management agreements, witnessed a rise of 13.6% and that too in a competitive market. .png)

Hotels & Resorts (Source: Company Reports)

Understanding the Performance of Entertainment – Australia: EVT added that Australian Entertainment revenue was, more or less, flat as compared to the prior year and the figure stood at $451.2 million. This was witnessed even though there was a less desirable genre mix of the films for the company’s audience. The group managed to achieve market share growth on the blockbusters, and while, the company attracts lower market share when it comes to family films, the company managed to grow the market share for the segment by 1.2 percentage points. Even though there was a genre challenge, the overall market share for the company was relatively stable in 2H of the year.

Dividends Remained Stable in FY 2019: EVT announced a fully franked final dividend of 31 cps, which brought the total dividend for FY 2019 to 52 cps, and this is consistent as compared to the prior year. The following picture provides a broader overview of the company’s dividends (along with other parameters), which could be important for the investors seeking dividend income..png)

Overview of Past Performance (Source: Company Reports)

The company has been managing capital with the objective of maintaining robust capital base so that investor, creditor and market confidence can be maintained, and it has a capacity to reap the benefits of opportunities that would enhance its existing businesses as well as enable growth and expansion in the future. The Board has been monitoring return on capital. The Board of the company also manages the gearing ratio.

What to Expect from EVT: EVT’s strategic plan would be dependent on the industry, economic and political conditions, impact of global events, future financial performance and available capital, competitive environment, evolving customer needs and trends, as well as availability of the attractive opportunities. There are expectations that the company’s strategies would continue to evolve as well as a change in response to the factors.

With respect to Hotels and Resorts business, the company would continue to provide hotel guests with accommodation which delivers product and service that is anticipated to meet or exceed expectations of guest. In order to provide this, it would continue to pursue strategies which primarily include upgrading of key properties, growing its conference and events revenue and leveraging the technology in order to improve efficiency via automation. The company’s focus on growing its existing business revenue, business transformation and maximising its asset performance might support its future operations, which could help it in generating respectable growth in key financial numbers.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

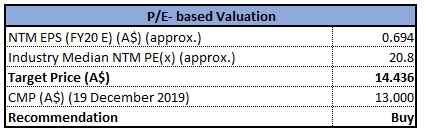

Method 1: P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters), NTM: Next Twelve Months

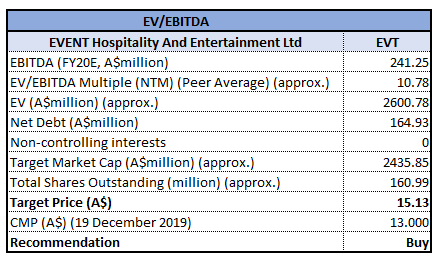

Method 2: EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Between FY 2015- FY 2019, EVT’s cash receipts witnessed a CAGR of 2.19% and, therefore, it can be said that EVT is possessing respectable capabilities to build cash levels. There are expectations that these capabilities might support its overall cash position and might further strengthen its cash base. In the span of the previous six months, the company’s stock has delivered a return of 4.90%. The company’s annual dividend yield stood at 3.98%, which is higher than the industry median (Hotels & Entertainment Services) of 2.7%. With respect to the cinema business, over the time span of next 3 years, the company would be upgrading its best locations by incorporating new and innovative cinema concepts developed as part of the ‘Future of Cinema’ strategy. Based on the foregoing, we have valued the stock using two relative valuation methods, i.e., P/E multiple and EV/EBITDA multiple, and arrived at a target price of lower double-digit update (in percentage terms). Hence, we give a “Buy” rating on the stock at the current market price of A$13.000 per share (down 0.459% on 19 December 2019).

EVT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...