1. Sector Landscape and Outlook

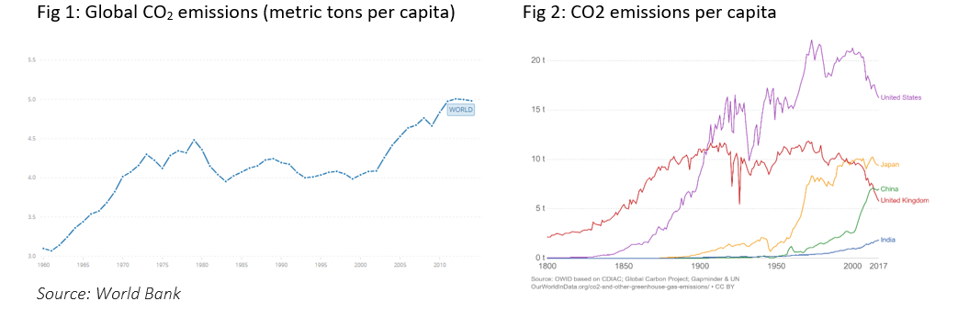

'Carbon emissions' has been an area which has recently received a lot of attention given the hazardous impact seen on people, infrastructure and economy as a whole. Factors such as the recent Australian Bushfires, and warmer than normal winters have further cemented the world’s attention towards carbon emissions. In the past, few decades, the global temperatures have risen steeply. In comparison to 1850s, we already have had experienced an average temperature increase of 1.10C. The industry experts anticipate that if the current emissions remain unrestricted, there could be an average increase in global temperatures by over 40Cabove the pre-industrial levels.

Negotiated by 196 state parties in April 2016 and already ratified by 55 state parties accounting to almost 55% of the world’s global GHG (Green House Gas Emissions), the Paris climate accord under the United Nations Framework Convention on Climate Change (UNFCCC), targets the average increase in temperature at 1.5 0Cabove the pre-industrial levels for the 21st century.

Let us understand the major contributing factors to the ever-ballooning emission issues and the counter measures taken to address the same.

.

Global Emissions Under Lens

Annual Emissions from the transportation sector accounts to almost 14% (including non-carbon dioxide emissions). Transportation is responsible for up to 30% of PM emissions in Europe & ranges from 12-70% varying unduly from transport-generated pollution, especially in Asia, Africa and the Middle East.

The per capita GHG emissions for Australia are more than twice as much per person as the average of the "Group of Twenty" (G20) in terms of greenhouse gas emissions. The per capita carbon dioxide emissions stood at 4.981 tonnes of carbon dioxide (2014 data) and at 16.89 tonnes of carbon dioxide in Australia. In Australia, ~61% emissions come from the electricity sectors and ~17.8% emissions from the transportation sector.

Considering that the transportation sector is one of the major contributors to the emission issues, it becomes pertinent to mitigate the same via sustainable initiatives. Let’s have a detailed look at the way out.

Electric Vehicle: Solution to the Puzzle

To battle the growing menace caused due to conventional vehicles, the Electric Vehicles might be an appropriate solution, reducing the emissions effectively and controlling the temperature rise.

The transition to electric mobility is progressing quicker than estimated, with regular reviewal to the sector’s outlook. Automotive majors committed in excess of $200 billion towards EV and its value chain. It is interesting to note that the auto major such as Ford rolled out EV variant of its iconic muscle car Mustang, the all-new “Ford Mustang Mach-E”. Initiatives such as these help to change the mindset of people in favour of electric cars. It is no surprise that market is assigning the electric car pioneer, Tesla a high premium with its market capitalisation almost reaching top spot in the beginning of this year.

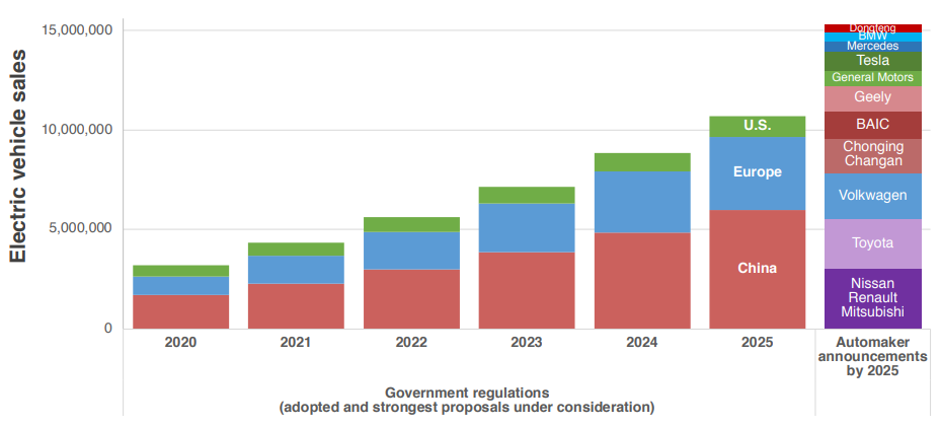

Fig 3: Global EV Outlook

Source:The International Council on Clean Transportation

Let us look at the existing market scenario and understand the outlook for the EV sector.

Current Market Dynamics

The EV sales surpassed the 2 million units' milestone in 2018, and the future depends on multiple factors affecting the sector. As per the EV Volumes portal, the Global plug-in electric sales reached a volume of 1.134 million units during the first half of 2019, which is a staggering 46% growth in comparison to 2018. The global EV adoption increased its market share to 2.5% in H1,2019 in comparison to the total vehicle sales. The first half growth accounted to the implementation of amendment in taxation and subsidy schemes globally, full availability of Tesla Model 3 and Europe’s enactment of rigorous regulations for CO2 emissions.

Outlook

The Industry, in general, is sanguine about the EV demand, but there is uncertainty over what the actual scenario would be in 2025 or 2030. International organisations such as the IEA estimates that EV sales would reach 44 million units in 2030. Impeding the government reforms and initiative are the price and supply disruption of the key metals like Cobalt and Nickel, which could thwart the cost declines that have been the bases for the affirmative EV future demand estimates.

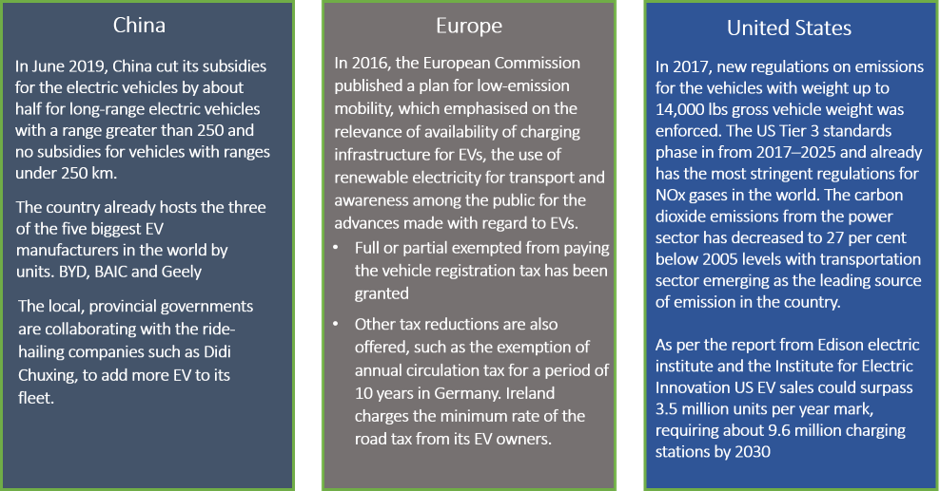

Governments across the globe have played their part in shaping the EV ecosystem and have been continuously nudging the auto manufactures to meet the goals set by the local authorities. Let’s have a quick look at few of the reform measures undertaken by the major sovereigns.

Fig 4: EV adoption and reforms

Having understood the EV regulatory framework, we need to now look upon the battery architecture.

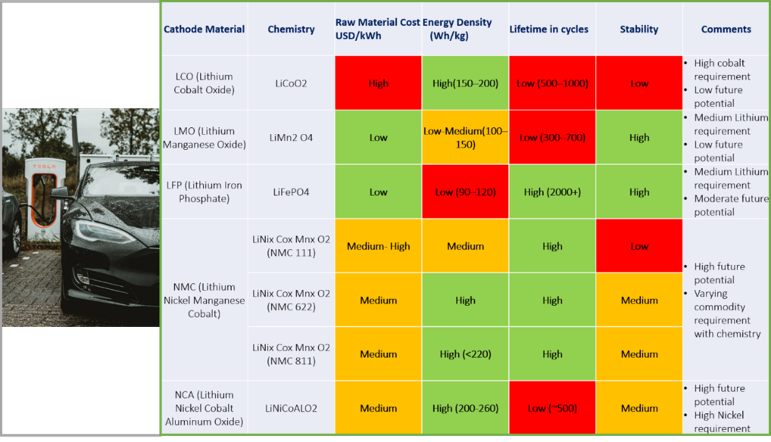

What is considered while selecting a battery pack for EVs?

For electric vehicles, the battery packs are developed with objectives of high power to weight ratio, specific energy and energy density as the lighter and smaller batteries reduce the size and weight of the vehicle, improving its performance. The high specific energy and energy density allows vehicles to last a longer range per recharge cycle. The charging/discharging cycle time and the cost of the batteries are also taken into consideration.

Here is a comparative analysis of the different existing battery technologies and their suitability in future.

Fig 5: Current Battery Technologies

Source: Kalkine Research

The future battery technology would require high energy density, long life and low manufacturing cost to keep the OEMs interested in high-quality battery manufacturing.

The major risks that could hamper the EV adoption rates in future are posed by the disruption in the supply of the metals. Now it calls for an insight into the supply dynamics of the battery metals.

Global Production and Consumption Trend

Backed by a strong support from various governments across the globe, green energy in general and EV sector, in particular, is seeing a strong push. Which in turn has fuelled the demand for battery materials which includes non-ferrous metals like lithium, cobalt, nickel, and graphite.

Lithium- Supply Overhang

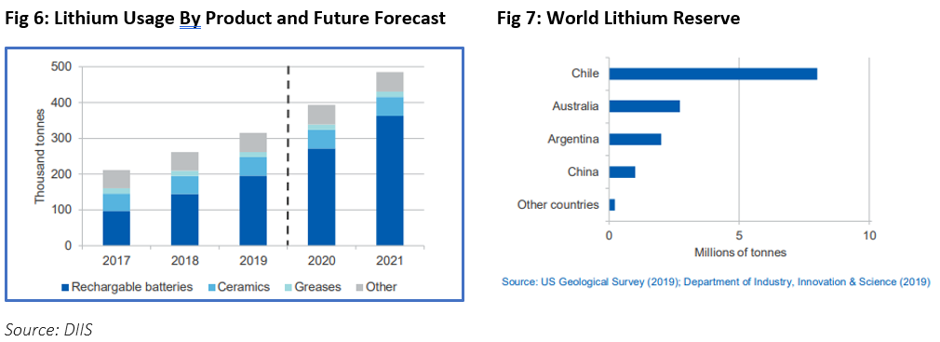

The global consumption for lithium carbonate equivalent stood at 315,000 tonnes in 2019, which is further forecasted by the Department of Industry, Innovation and Science (or DIIS) to grow at an annual average rate of 20 per cent to stand at 489,000 tonnes by 2021.

The increase in battery manufacturing across China and especially across South Korea amid growing uptake of electric vehicles and improvements in battery capacity is particularly supportive for lithium chemicals.

How are the players adopting to cope with the challenges due to lower lithium prices?

Going Up the Value Chain

The trade for lithium chemicals is somewhat picking momentum across the globe, which has prompted many lithium mining companies across Australia to go up on the value chain. Recent examples of such an up move include

(a) Mineral Resources Limited's sell-down of Wodgina to the global lithium chemical giant- Albermarle to obtain hydroxide processing.

(b) Pilbara Minerals and POSCO JV negotiations for setting up a lithium carbonate and hydroxide conversion facility in South Korea.

The global lithium production surged by 18 per cent on a yearly basis to stand at 470,000 tonnes in 2019, which is further anticipated by DIIS to stand at 489,000 tonnes in 2021.

Let us now dig into the supply scenario for one of the world’s largest lithium producer.

Australia Production Capacity

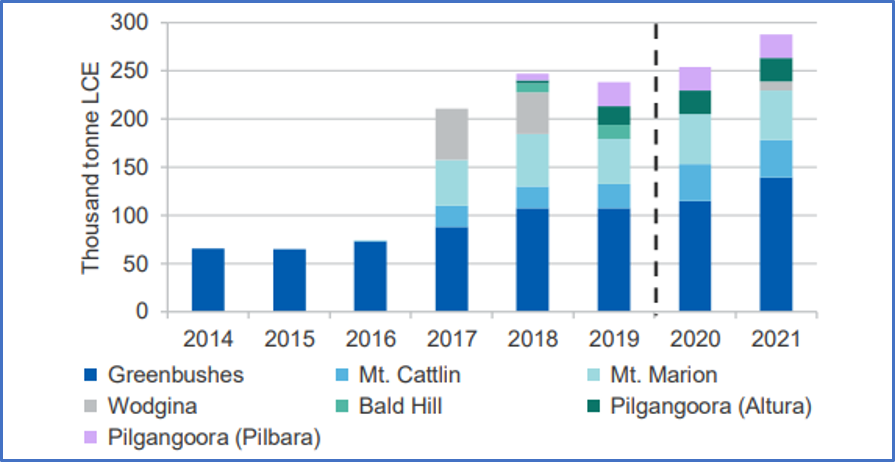

Australia’s spodumene concentrate production for 2018-19 stood at 1.1 million tonnes to 1.3 million tonnes, an increase of 20 per cent over the previous year. Further, Spodumene production is forecast to increase to 1.9 million tonnes by 2020–21.

Mineral Resources’ Mt Marion Doubles Capacity: Mt Marion-operated by Mineral Resources was initially designed to produce 206,000 tonnes of spodumene concentrate per year; however, a current upgrade for the project, increased the production capacity to 450,000 tonnes at 6 per cent spodumene.

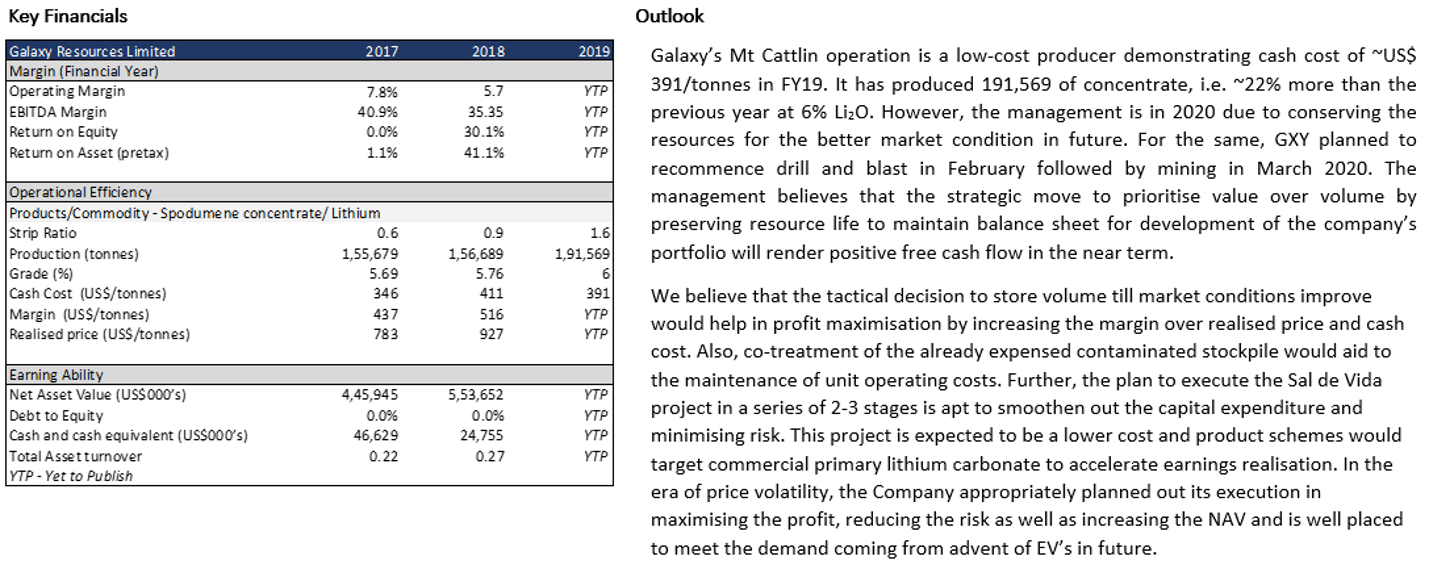

Galaxy Resources’ Mt Cattlin Operations Record Production of 191,000 tonnes of Spodumene: Mt Cattlin-fully owned and operated by Galaxy Resources holds the potential to process 1.6 million tonnes per annum pegmatite ore in order to produce 180,000 tonnes per annum of 6 per cent spodumene. The Mt Cattlin operations produced a total of 191 kilotonnes of Spodumene concentrate with a cash cost per tonne produced of US$391 for the full year, reinforcing Mt Cattlin’s market position as a low-cost producer of spodumene concentrate.

The anticipation of the upsurge in demand has caught the eyes of not only the existing companies but also newer companies throwing in the hat.

The New Entrants in 2019

In October 2019, Rio Tinto unfolded a large potential source of lithium while looking for gold in piles of waste rock of borate in California. Rio now plans to invest an initial $10 million over a pilot plant (on-site), which would purify the waste rocks and extract lithium into a form suitable for the electric vehicle batteries, which would mark another phase of $50 million booster towards a plant capable of industrial-scale with a capacity of approx. 5,000 tonnes of lithium carbonate equivalent a year.

In March 2019, Altura Mining Limited announced a commercial production at the Pilgangoora Mine, which is now rated to produce 220,000 tonnes of spodumene concentrate per annum.

We need to look at one of the world’s largest lithium producing nation – Chile to completely understand the supply situation going forward.

Chile: World’s largest Lithium reserves, moving Slow with Lithium

The South American nation possesses the world's largest reserves of lithium which is of high quality; however, Chile's government has been slow to allow new players to enter the market. Also, the stringent policy for lithium mining in Chile could keep new entrants at the bay. Chile places lithium under the list of “Strategic Metals” and lithium mining in Chile requires either joining hand with the government or obtain a special permit known as a CEOL to mine lithium.

Albermarle and SQM remain to be the top Chilean producers and the entry of new entrants looks difficult under the stringent policies. For example, as per the current plans of the government, a mining company also needs to set up the value chain in Chile (such as a processing plant for lithium chemical production) to obtain the Chilean lithium brine.

The producers are taking proactive measures to battle the oversupply situation plaguing the lithium market.

How are Lithium Miners Addressing the Supply Glut?

The rush for lithium, which once took the prices to a record high in 2018, witnessed a halt amid higher exploration and large production from big suppliers such as Australia and Chile. However, the large supply created by the lithium mining companies played out negatively for the small entrants amid a massive fall in prices.

Many lithium mining companies such as Alita Resources Limited ran out of business amid higher cost and fall in demand and price of lithium. The shutdown of operation by such small caps served as a signal for the large Australian players such as Galaxy Resources, Pilbara Minerals Limited, Orocobre Limited, and these mining companies kept the production steady in line with the offtake agreements or demand.

The measured production from many lithium mining companies across Australia has resulted in a pullback in spodumene supply, which is expected by a number of industry experts to ease the downward pressure on lithium prices over the short run.

Now, let’s ponder over the measures taken by the lithium producers to mitigate the oversupply issue.

Short-term Cutbacks on the Spodumene Production Across Australia: Galaxy announced a halt in mining at Mount Cattlin in October 2019, and the company is currently using the existing stockpiles to meet the offtake demand from consumers, whilst adopting cost-cutting measures. The Wodgina prospect (Mineral Resources Limited) has been placed under maintenance, and the deteriorating market condition has led many other producers to concentrate on product quality rather than on volumes, leading to an overall decline in spodumene production across Australia in 2019.

Fig 8: Australian spodumene ore production

Source: DIIS

Defer FID for Mount Holland by SQM: The Chilean lithium chemical behemoth- SQM along with its partner Wesfarmers Limited decided to defer the final investment decision (FID) over Mount Holland, which is one of the biggest undeveloped hard-rock lithium projects in Australia, until the first quarter of 2021.

Difficulty for Brine Producers: While the spodumene producers had pulled back their production in 2019, the brine producers across South America (especially Chile) had also faced some hard times, which kept the brine production in check. La Negra- operated by Albermarle in Chile, has been experiencing production setbacks, and Albermarle has delayed works on La Negra III & IV.

Post analysing the scenario for lithium, let us discuss the other battery materials.

Cobalt

Cobalt is another battery chemical, which is in focus with the demand for the metal presently strong with EV makers who are continuously looking for a stable supply.

The Australian cobalt mining companies are particularly gaining attention of global investing community amid its potential to provide the clean and ethical supply of cobalt, a quality seemingly lacking in the largest resources holder- Democratic Republic of Congo, over its unethical practices such as child labour, volatile mining policies to increase royalties, and labour abuse.

In terms of projects in Australia, Sconi Project- operated and owned by Australian Mines Limited, is anticipated to be one of the most cost-efficient nickel sulphate and cobalt prospect across the globe with an estimated production capacity of 1,405,000 tonnes of nickel sulphate and 209,000 tonnes of cobalt sulphate over its initial mine life of 30 years.

Nickel

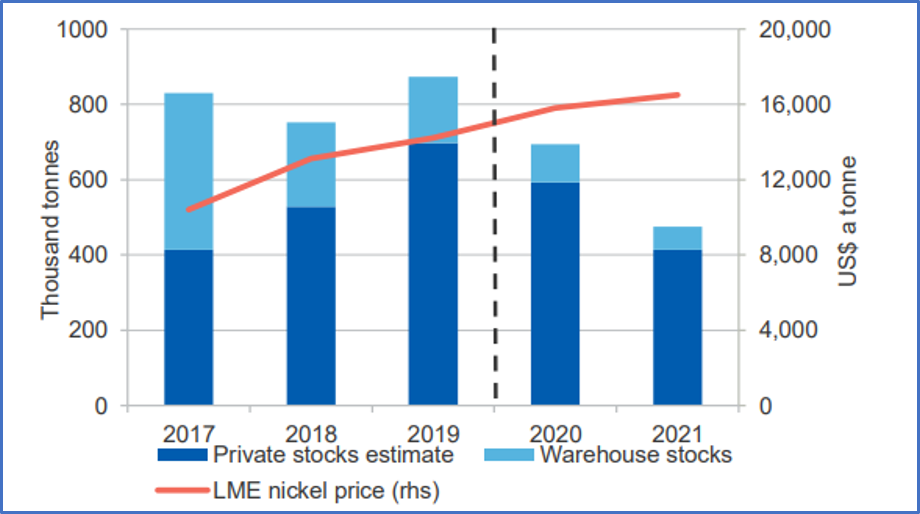

Nickel prices are expected to grow over the short-run amid a push in demand for energy storage devices. Currently, Australia is the sixth-largest miner of nickel with a production of over 200 thousand tonnes of nickel each year.

The export ban for nickel in Indonesia is anticipated to play-out for the Australian nickel mining companies ahead.

Fig 9: Forecast nickel spot price and stock levels

Source: DIIS

Graphite

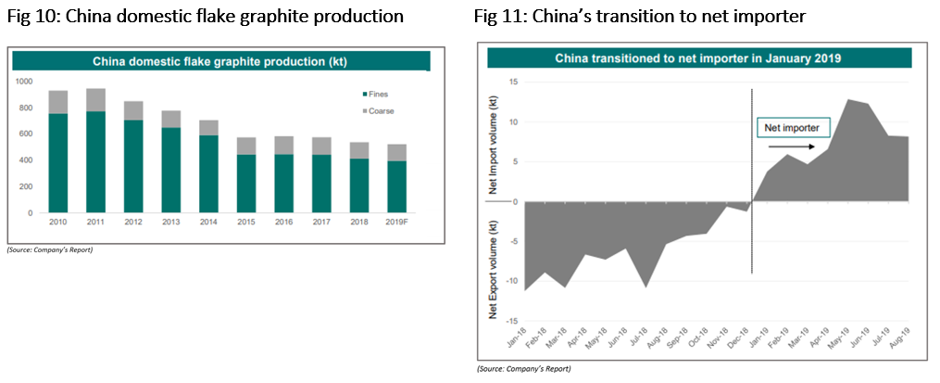

The prices for natural graphite still remain soft in China; however, the outlook over the lithium and much over the penetration of the battery storage devices into the global energy storage market is keeping the graphite in focus across the battery material space.

The supply chain of the Chinese flake graphite is losing the momentum, which could provide an advantage to Syrah as the Company holds its flagship project in Mozambique, which supplied 17 per cent of the global graphite market in 2018, while we are cognisant of few risks here.

The gradual decrease in China’s flake graphite chain led the country to start importing natural graphite from January 2018, which further led to make China a net importer.

2. Investment Theme and Stocks under Discussion

The demand for the EVs is well placed to follow an upward trend in the upcoming years, with this backdrop, we anticipate the battery materials to be in greater demand with the EV sales approaching inflection point, accelerated by government reforms, improvement in the EV range making it more competitive as against the conventional ICE vehicles. Australia backed by a conducive mining environment would continue to expand the supply for the battery materials.

After understanding the sector, let’s take a detailed look at seven miners in terms of their outlook and performance. To gauge the potential of the mining stocks, we have followed the market multiple approach and used ‘EV/Sales’ for most of the cases.

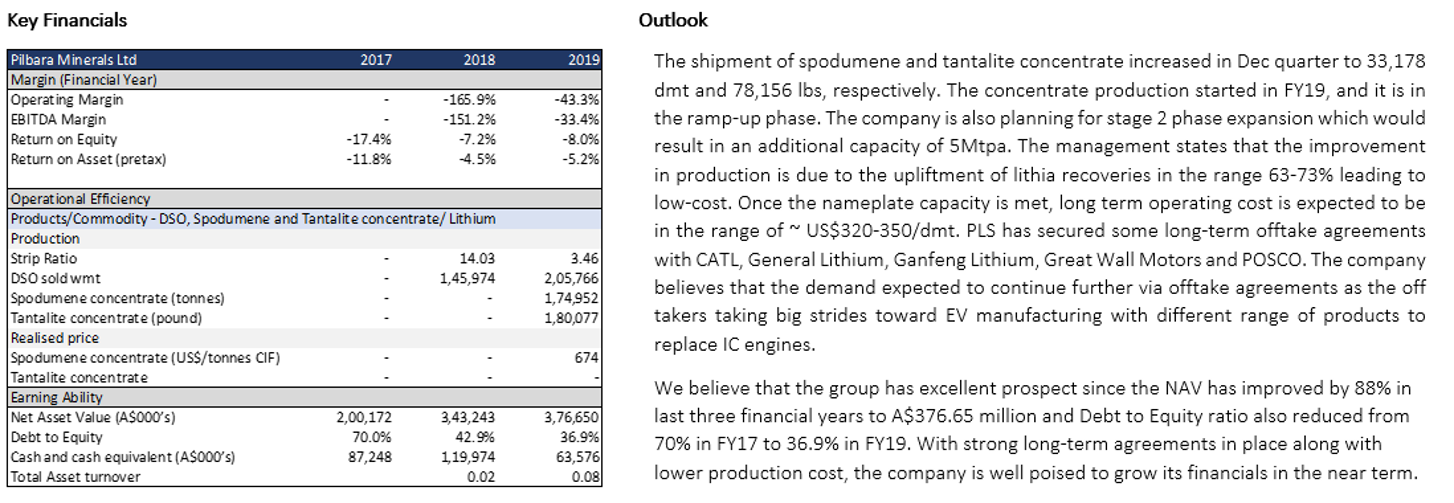

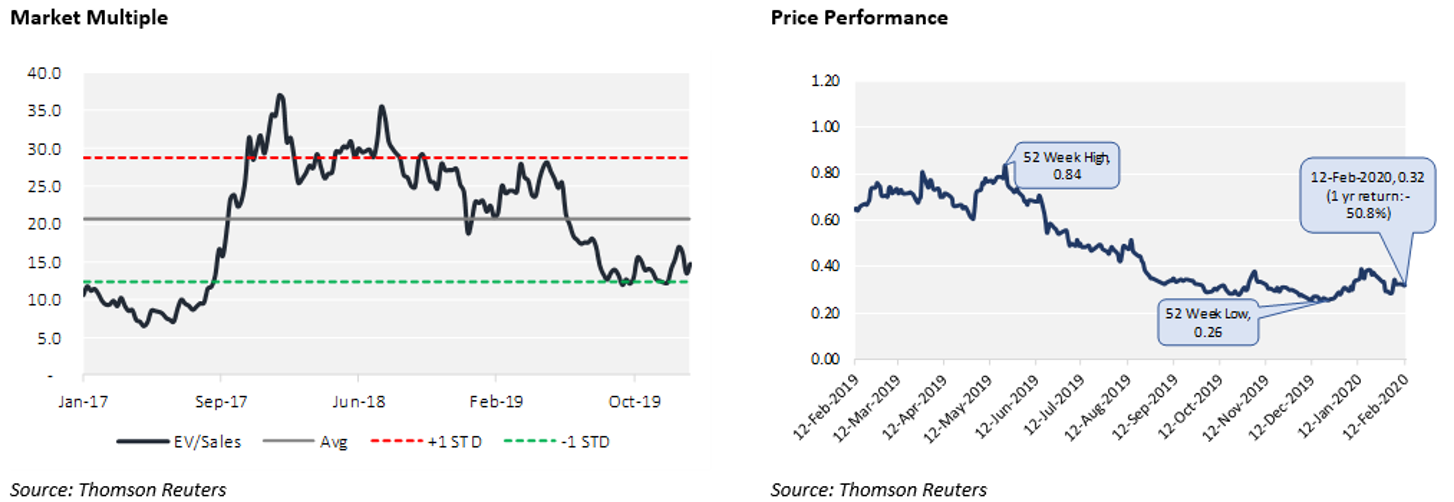

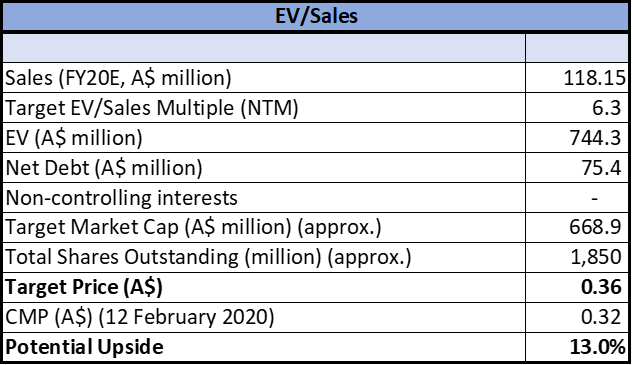

1) ASX: PLS (PILBARA MINERALS LIMITED)

(Recommendation: Buy, Potential Upside: 13%)

Valuation

Our valuation model suggests that the stock has a potential upside of ~13% on 12 February 2020 closing price. The stock is currently trading at a forward EV/Sales multiple of ~14x. The group has a strong pipeline of offtakes which is expected to result in an improved financial performance in the coming years and is the reason for the group trading at a higher multiple. However, we believe that commanding such higher multiple is not feasible in the long term and the stock would eventually trade at a lower and more sustainable multiple in future, given the current industry dynamics. We also believe that despite a multiple contraction, improving financials would be driving the share price going forward.

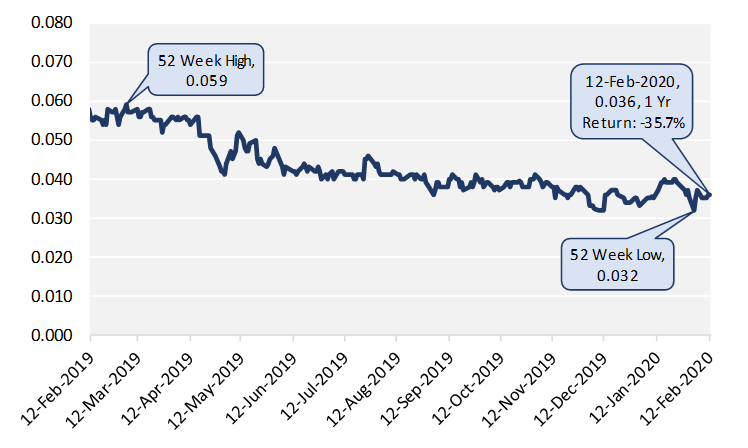

2) ASX: LIT (LITHIUM AUSTRALIA NL)

(Recommendation: Speculative Buy)

Outlook

LIT has developed a number of lithium extraction processes (LieNA® & SiLeach ®). Lithium Australia has been awarded a grant by the Australian federal government’s CRC-P initiative to support the next stage of its $3.6 million LieNA® research and development program for the recovery of lithium from fine spodumene. LIT seeks to integrate the operations of VSPC and Envirostream in the long run. VSPC (a LIT subsidiary) has successfully obtained a co-funding grant from AMGC in the $5 million battery development program. VSPC will further develop its proprietary technology for lower-cost and recycled raw materials for the manufacture of lithium-ferro-phosphate (‘LFP’) cathode material.

Envirostream Australia Pty Ltd, a subsidiary of Lithium Australia (90% stake), focusses on the battery recycling business segment. In FY19, Envirostream generated a revenue of $1.3 million from the recycling of 149 tonnes of spent LIBs. It also signed an offtake agreement with Korean-based SungEel Hitech mixed metal dust product (containing the battery materials), for which the shipment started in December 2019.

We anticipate that offtake agreement along with recycled MMD product would drive the company’s revenue in the near term. MMD product is also expected to enable the company to enjoy high margin in the era of low lithium and other battery commodities prices.

On TTM basis, the stock is available at a price to book value of 1.3x as compared with 1.6x of the industry median. It reflects undervalued position at the current levels. Based on the company’s positive outlook we have a ‘speculative buy’ recommendation on the stock.

Price Performance

(29).png)

3) ASX: CXO (CORE LITHIUM LIMITED)

(Recommendation: Speculative Buy)

The company’s core asset Finniss Lithium project is expected to commence operation by the end of 2021. The project already has an offtake agreement with Sichuan Yahua Industrial Group Co. Ltd for 75ktpa of spodumene concentrate, 40% of total 175ktpa capacity. Interestingly, the project also has a deal with the Port of Darwin to handle the future export of lithium product. The logistic agreement is in place for export of up to 250ktpa of spodumene concentrate or 1Mtpa of spodumene Direct Shipping Ore (DSO). CXO is presently working toward the increment of reserves and resources of the Finniss project, and the management believes that the lithium product would be of high quality at a lower C1 cost of US$300/t.

We believe that the company would be able to produce high quality and lower cost product since the project is well located and presence of apt infrastructure within 25km to port, power and rail along with DMS (gravity) processing method is likely to lower the operating cost. Also, the company recently identified new gold and base metal prospect at Adelaide River Gold Project, located 25km south-east of Finniss Project create positivity due to its leverage position. Further, High-grade nickel and cobalt potential also reported at the company area during the historical data review at Adelaide River Project.

From the valuation standpoint, P/BV multiple on TTM basis stood at 1.0x which is lower than the industry median of 1.6x, indicating that the stock is undervalued at the current juncture. Based on the company’s positive outlook we have a ‘speculative buy’ recommendation on the stock.

Price Performance

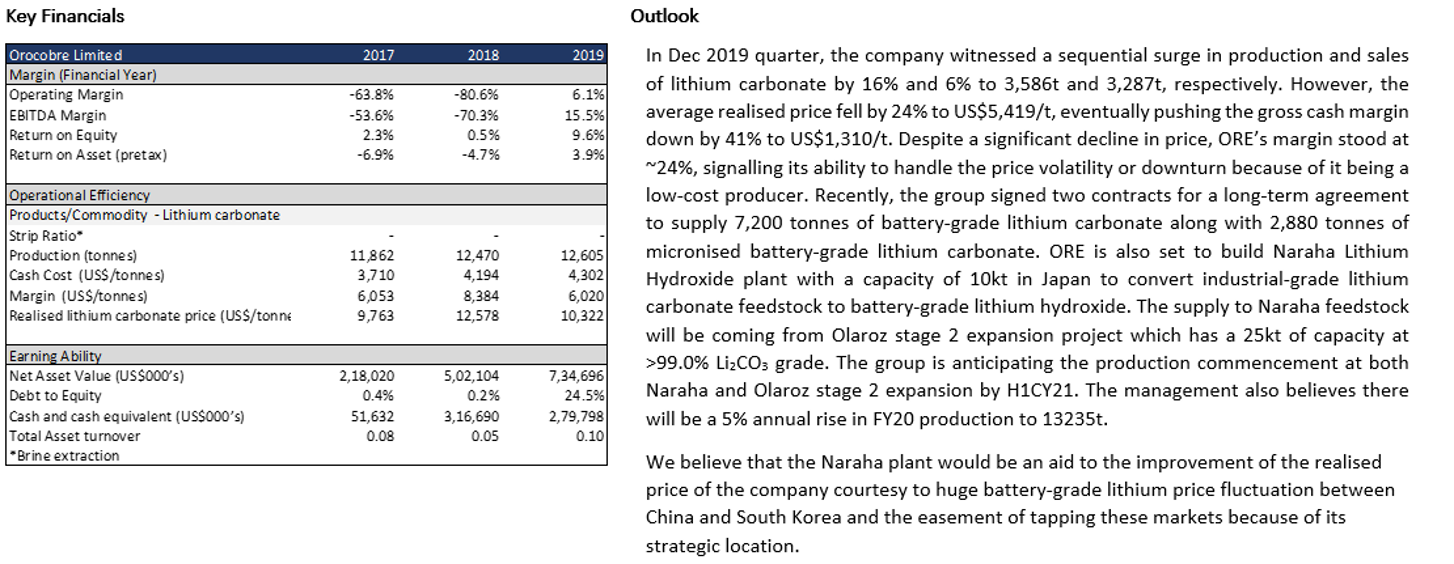

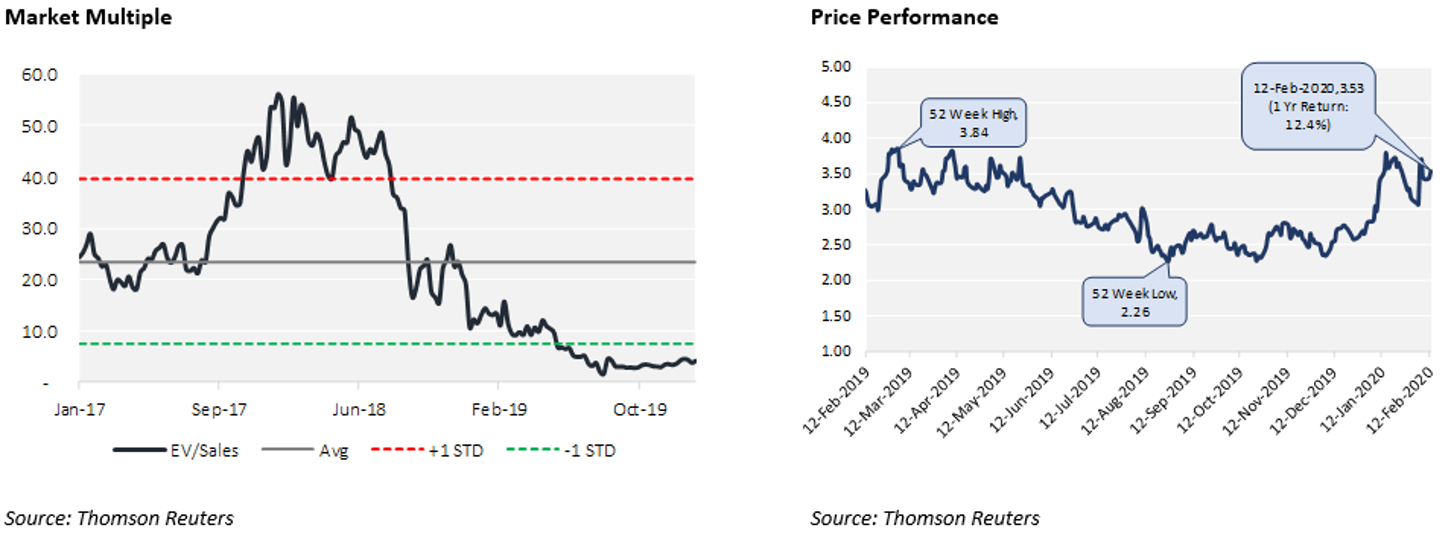

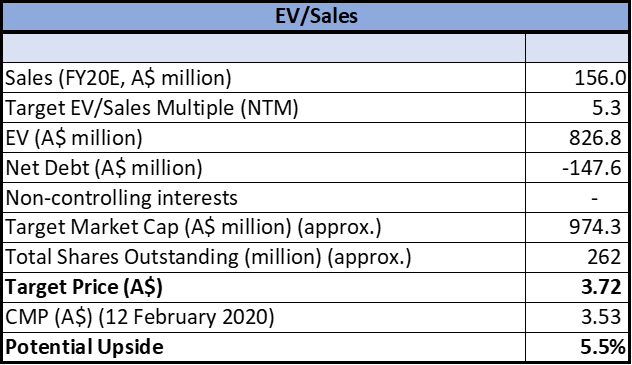

4) ASX: ORE (OROCOBRE LIMITED)

(Recommendation: Hold, Potential Upside: 6%)

Valuation

Our valuation model suggests that the stock has a potential upside of ~6% on 12 February 2020 closing price. The stock is currently trading at a forward EV/Sales multiple of ~4.5x. The anticipated completion of Olaroz stage 2 expansion project which would provide the feed for the Naraha plant is the key catalyst. Consequently, there would be an improvement in the group’s top line and an expansion in its market multiple.

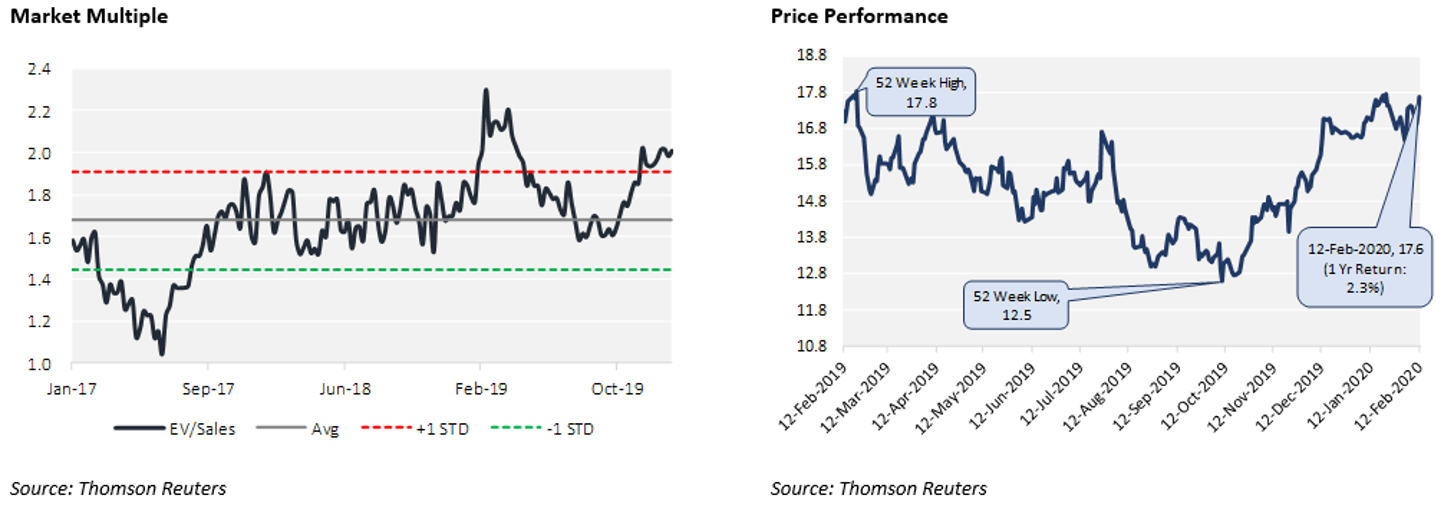

5) ASX: GXY (GALAXY RESOURCES LIMITED)

(Recommendation: Hold, Potential Upside: 4%)

Valuation

Our valuation model suggests that the stock has a potential upside of ~4% on 12 February 2020 closing price. The stock is currently trading at a forward EV/Sales multiple of ~2.8x. The management is focusing on resource preservation by reducing the mining and production rate which is expected to benefit in the longer run. We do not see any significant changes in the group’s operating metrics and believe that the group would continue to trade near the current multiple.

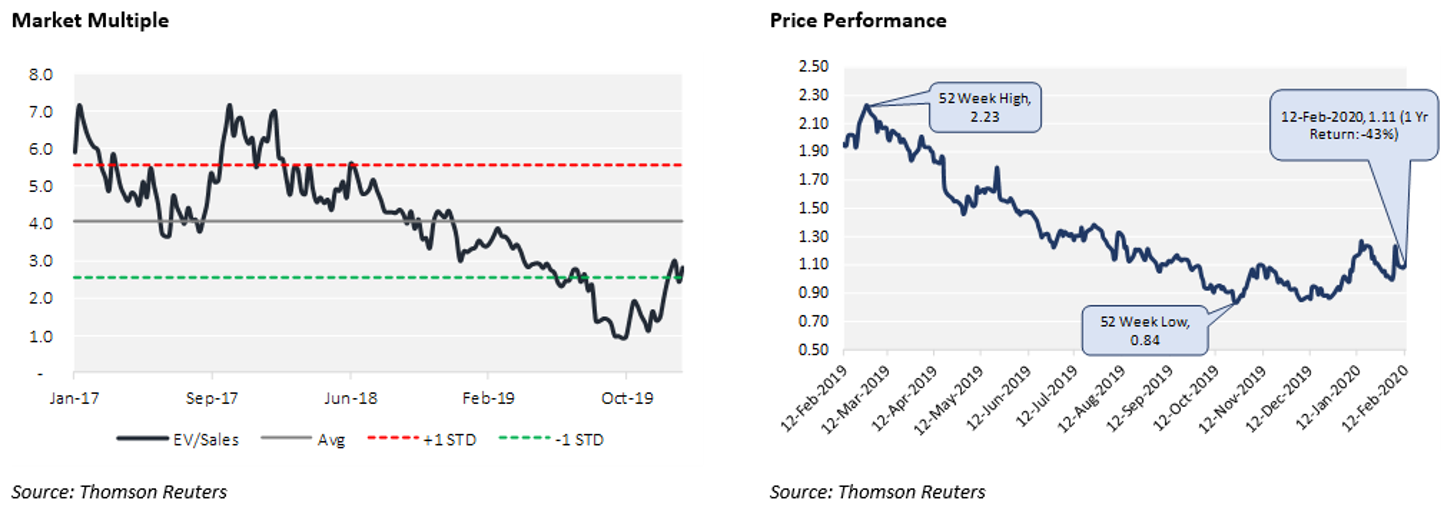

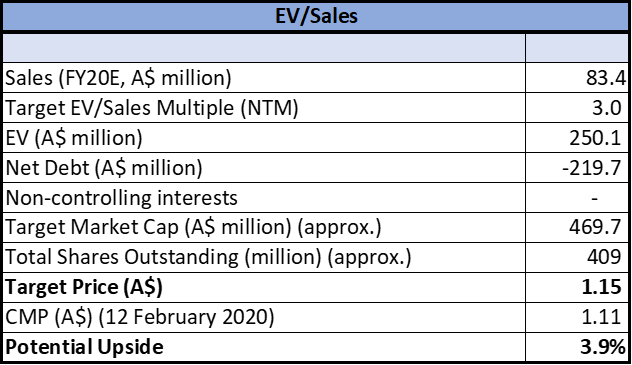

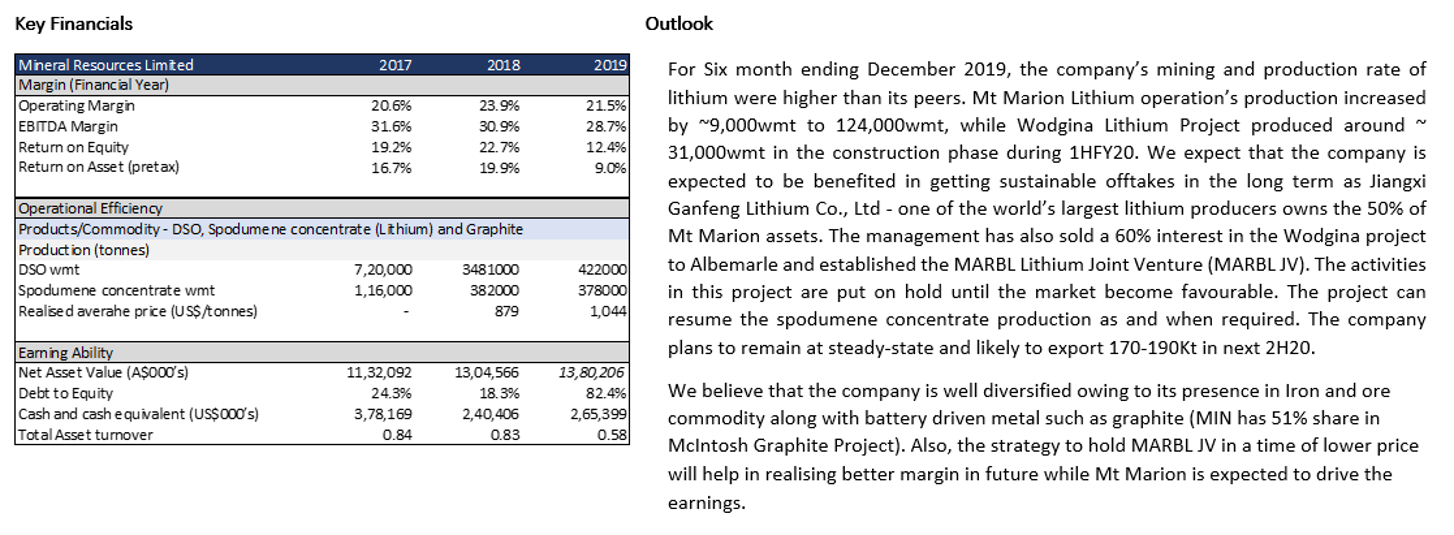

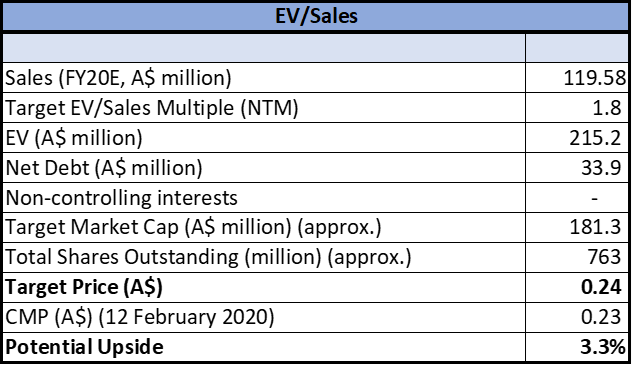

6) ASX: MIN (MINERAL RESOURCES LIMITED)

(Recommendation: Hold, Potential Upside: 8%)

Key Financials:

Valuation

Our valuation model suggests that the stock has a potential upside of ~8% on 12 February 2020 closing price. The stock is currently trading at a forward EV/Sales multiple of ~2.0x. We believe that the group’s partnership with Jiangxi Ganfeng Lithium (one of the world’s largest lithium producers) in Mt Marion assets would result in securing more sustainable offtake agreements. We expect the group’s multiple to expand following its association with Lithium majors such as Albemarle.

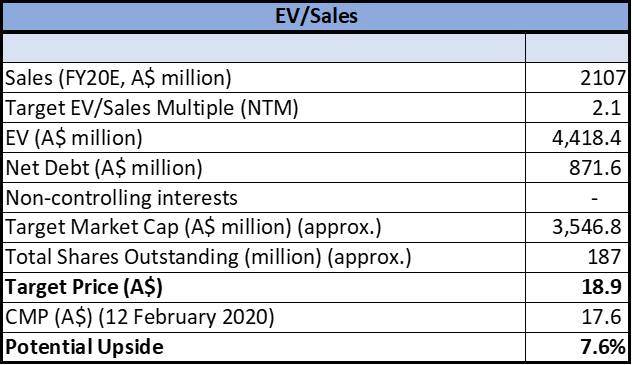

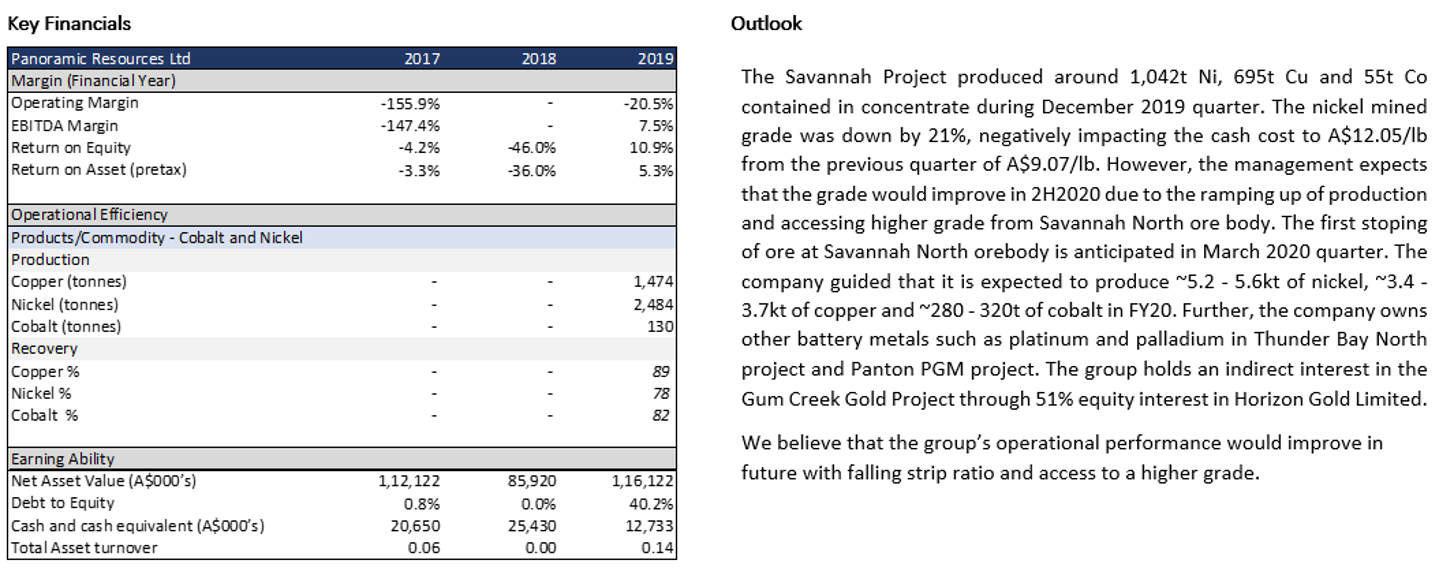

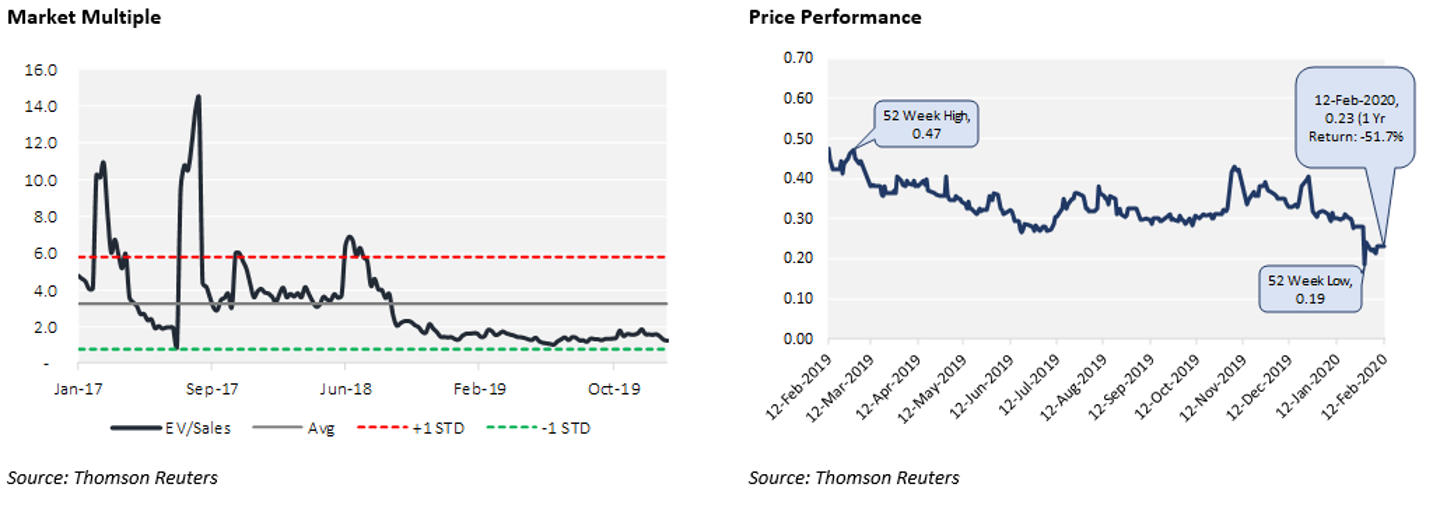

7) ASX: PAN (PANORAMIC RESOURCES LIMITED)

(Recommendation: Watch, Potential Upside: 3%)

Valuation

Our valuation model suggests that the stock has a potential upside of ~3% on 12 February 2020 closing price. The stock is currently trading at a forward EV/Sales multiple of ~1.2x. The management has guided for higher production in FY20. We believe that higher production resulting from higher grade along with low strip ratio would result in a better financial number which eventually lead to a multiple expansion in FY20.

Note: All the recommendations and the calculations are based on the closing price of 12 February 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

AU

AU

Please wait processing your request...

Please wait processing your request...