Kalkine has a fully transformed New Avatar.

Company Overview: Estia Health Limited is engaged in operating and developing owned and leased residential aged care facilities throughout Australia. The Company's homes offer a range of care services, from providing semi-independent living, to specific and comprehensive care for those with memory or cognitive support needs. The Company offers services, including personal assistance, meals, therapies and lifestyle activities. It offers residents with general activities, such as gardening, reading, movies, music, parties, cultural celebrations, art sessions or daytrips and lifestyle coordinators, and can also cater for many specialist interests. It offers clinical care that includes regular reviews and includes daily medication; pain management program; medical services, such as physiotherapy, pharmacy, podiatry, optometry and dental; specialist dementia care, and personal care. It operates homes in Victoria, South Australia, New South Wales and Queensland.

.png)

EHE Details

Higher Investments & Portfolio Expansion are Key Catalysts: Estia Health Limited (ASX: EHE) is involved in providing high-quality residential aged care services across Australia. It provides care services to over 8,000 residents across ~69 homes in Victoria, South Australia, NSW and Queensland. The Company offers services including personal assistance, therapies, meals, & lifestyle activities. It also provides clinical care that comprises frequent assessments and includes pain management programs, daily medication, medical services, expert dementia care, along with personal care.

For the year ended 30 June 2019, the company reported revenue of $585.98 million, up around 7.1% year over year. EBITDA for the year stood at $93.97 million, up by 4.3% year over year. Profit before income tax (PBIT) for the year came in at $57.8 million, marginally up from $57.16 million reported in FY18. In FY19, net profit after tax (NPAT) came in at $41.29 million, almost flat on a year over year basis. Diluted earnings per share for the period came in at 15.77 cents per share, as compared to 15.75 cents per share in FY18. The company declared a fully franked final dividend of 7.8 cps, which brought the full year dividends (fully franked) to 15.8 cents per share.

For FY20 & beyond, the company continues to improve its strategy and focus pertaining to occupancy, which would become more crucial in an environment of increased competition and heightened customer expectations. The company remains on track for new quality standards, with increased investment in resident amenity and improvements in quality and safety systems. Further, the company focuses on expanding its portfolio and continues to take necessary measures to improve the quality of its existing homes. In doing so, the company has been carrying out the acquisition of new homes since FY18 and is continuously looking for single and multiple home acquisition opportunities to expand its portfolio and improve the financial performance in the coming years.

The company witnessed a compound annual growth rate of 19.8% in revenue in the time span of FY15-FY19. The company has been investing in new technology and service enhancement. Further, the company’s focus on enhancing clinical governance, quality management and resident care systems by construction of new homes and refurbishment of existing properties to expand bed capacity, will drive future earnings. The company has also witnessed growth in EBITDA from $30.9 million to $93.97 million over a time span of FY15-FY19. Professional development programs (PDP) increased from 3,894 in FY17 to 4,959 in FY19.

.png)

Growth in Revenue & EBITDA (Source: Company Reports)

.png)

Growth in PDP (Source: Company Reports)

FY19 Performance: During the period, revenue stood at ~$586 million, increasing 7.1% year over year. Revenues from Government-funded residential care subsidies & supplements came in at $438.3 million, whereas revenues from Resident daily care fees and other resident fees came in at $104.3 million and $43.4 million, respectively. EBITDA for the year stood at $93.97 million, up 4.3% year over year. Notably, average occupancy rate stood at 93.6% in FY19, as compared to 94.2% in FY18. In FY19, net profit after tax (NPAT) stood at $41.3 million, as compared to $41.2 million reported in FY18. Operational beds in FY19 increased to 6,102, from 6,046 in FY18.

.png)

FY19 Results (Source: Company Reports)

Geographical performance: During the year, total number of operational homes in Queensland stood at 8 homes in 851 operational places. With respect to North South Wales, total number of operational homes was 17 homes in 1,890 operational places. Further, total number of operational homes in South Australia was 17 homes in 1,348 operational places. Victoria had around 27 homes in 2,091 operational places. Total number of operational homes as at 16 August 2019 came in 69 homes with 6,180 total operational places.

.png)

EHE’s Network of Homes (Source: Company Reports)

Balance Sheet Position: At the end of the year, the company reported cash and cash equivalents of $14.63 million. For the year, the company had a net bank debt of $110.4 million with $201.0 million in undrawn debt facilities. As at 30th June 2019, the company had total bank facilities of $330 million with an expiry date of 22nd August 2020. The gearing ratio was 1.2x EBITDA. An amount of $93.8 million was utilised as capital investment to expand and enhance the company’s home portfolio, which was the highest level of capital investment since listing in 2014. Net RAD inflows came in at $14.6 million in the year, with a RAD balance of $805.0 million, recorded as at 30 June 2019.

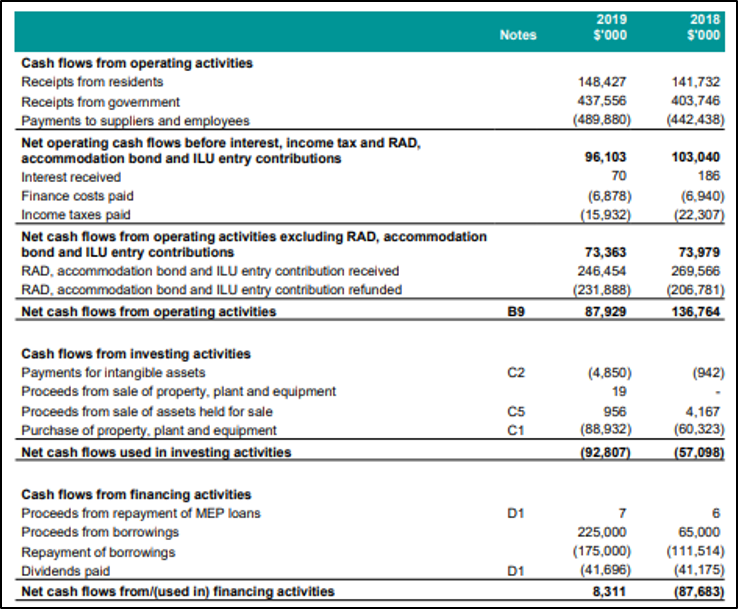

Cash Flow Position: Operating cash inflow in FY19 came in at $87.9 million as compared to $136.7 million in FY18. Net cash outflow from investing activities in FY19 came in at $92.8 million as compared to $57.1 million in FY18. Net cash inflow from financing activity in FY19 came in at $8.3 million.

Cash Flow Details (Source: Company Reports)

In FY19, the company had around 13 homes with a total of 1,105 beds, which were all redeveloped via a $15.5 million capital investment. The company expects to refurbish 15 more homes with additional 1,562 beds during FY2020. This will result in ~49 homes with a total of 4,801 beds for the Higher Accommodation Supplement by 30 June 2020. With the above scenario in place, the company is confident about retaining its existing customer base and expects to maintain dominant growth momentum in FY20.

Recent Update:

Shareholding Update: Recently, the company issued an announcement stating that United Super Pty Ltd has become a substantial holder of the company, with a voting power of 5.01%.

Trading Update: The company stated that its spot occupancy has declined to 93.5% across its portfolio of 5,944 operational beds at 30 November 2019. However, the company now expects dynamics and sentiment of customers to improve in the near term. The company will report its FY20 Half Year results for the period ended 31st December 2019 on 25th February 2020.

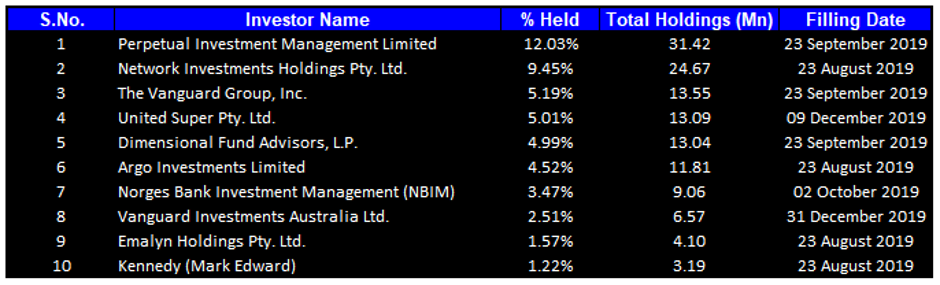

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 49.98% of the total shareholding. Perpetual Investment Management Limited is the entity holding maximum shares in the company at 12.03%. Network Investments Holdings Pty. Ltd. is the second-largest shareholder, with a holding of 9.45%.

Top Ten Shareholders (Source: Thomson Reuters)

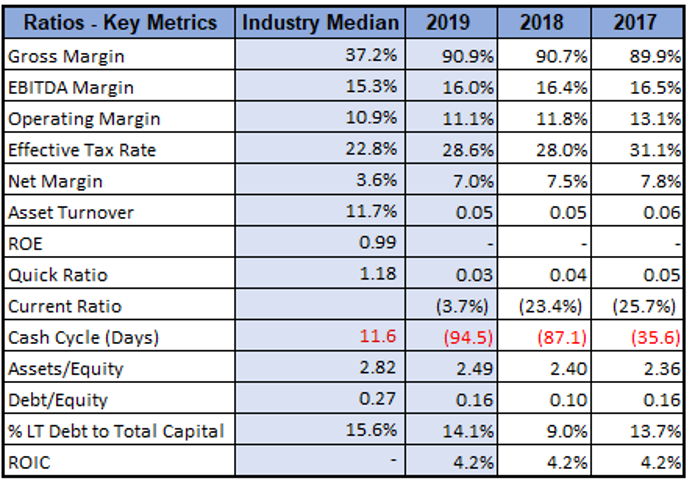

Key Metrics: In FY19, the company had a gross margin and EBITDA margin of 90.9% and 16.0%, which is higher than the industry median of 37.2% and 15.3%, respectively, representing decent fundamentals. The company’s debt-to-equity multiple in FY19 stood at of 0.16x, lower than the industry median (debt-to-equity multiple) of 0.27x, demonstrating a better financial position. Net margin of the company was reported at 7.0%, higher than the industry median of 3.6%.

Key Metrics (Source: Thomson Reuters)

Outlook: For FY20, the company expects EBITDA on Mature Homes to be in the range of $78 million to $82 million. The company remains on track to accommodate new quality standards, with increased investment in resident amenity as well as improvements in quality and safety systems. It continues to improve its strategy and focus related to occupancy, which would become even more vital in an environment of increased competition and heightened consumer expectations. Further, Estia Health Limited would be carrying out activities which would support it in the refurbishment as well as execution of expansion plans for the existing homes. The company’s balanced approach with respect to growth coupled with the expansion of its existing portfolio reflects its progress towards sustainable future growth.

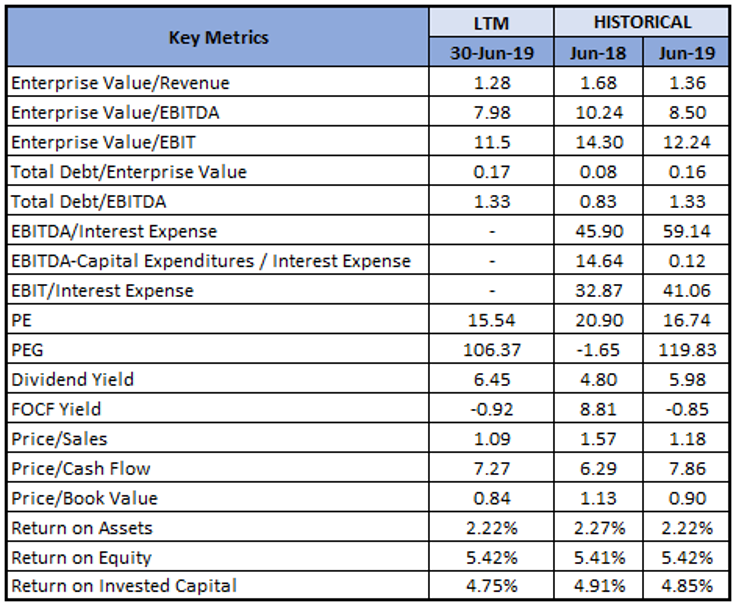

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company is currently trading below the average of its 52-week trading range of $2.25 - $2.99. In FY19, the company delivered a decent result, driven by increased investment in resident amenities as well as improvements in quality and safety systems. The company made substantial investments in infrastructure, people, and technology. The company has also planned for the refurbishment of further 15 homes with an additional 1,562 beds during FY2020. In FY19, the company reported an uplift in key profitability margins and depicted a stable financial position with debt remaining at decent levels. From the analysis standpoint, the company has recorded revenue CAGR of 19.8% over the last four years. Considering the above factors, we have valued the stock using a relative valuation method, i.e., Enterprise Value to Sales multiple, and for the purpose, we have taken the peer group Ansell Ltd (ASX: ANN), ResMed Inc (ASX: RMD), Virtus Health Ltd (ASX: VRT), Cochlear Ltd (ASX: COH). As a result, we have arrived at a target price depicting an upside of higher single digit (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.52, up 2.857% on 29th January 2020.

EHE Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...