Kalkine has a fully transformed New Avatar.

Company Overview: Empired Limited is an information technology (IT) services provider. The Company is engaged in design, development and integration of business knowledge, information technology and creativity. The Company operates through two segments: Australia and New Zealand. The Company's business solutions include Cloud Services, Identity and Access Management, Systems Integration, Data Insights and Business Intelligence, Internet of Things, Spatial Services, Mobile Solutions, Digital and Experience Design, Enterprise Content Management (ECM), Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Digital and Experience Design, Infrastructure Transformation Services, Managed Infrastructure Services, Project Management Office (PMO) and Unified Communications. The Company operates in various industries, including retail and manufacturing, public sector, financial services and insurance, health, mining, oil and gas, utilities, transport and education.

.PNG)

EPD Details

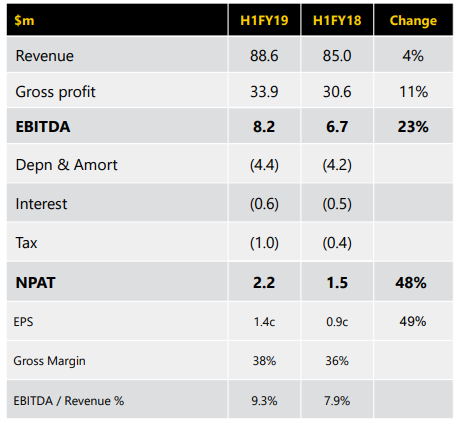

Decent Performance in 1HFY19: Empired Ltd (ASX: EPD) is a small-cap information technology (IT) company with the market capitalisation of circa $51.24 Mn as of 09 July 2019; and is known for partnering with government and corporate customers across the globe for delivering tech-related services. The group had earlier released its results for 1H FY 2019 in which the company witnessed an increase in key metrics on the YoY basis. Its revenues increased by 4% on the pcp basis and stood at $89 million while EBITDA witnessed a 23% increase on pcp basis to $8.2 million. Also, the company’s NPAT stood at $2.2 million, which reflects an increase of 50% on pcp basis. Resultantly, earnings per share witnessed a significant rise of 49% and stood at $0.014. During 1H FY19, the company had secured multi-year, multi-million dollar digital transformation contract in NZ Public Sector with DIA (or Department of Internal Affairs). It can be said that the company is positioning itself for growth and its solutions are aligned to the high growth market opportunities and its strengthening of the balance sheet and growing of free cash flow are expected to support the growth initiatives. From the analysis standpoint, the company’s stock seems to be quite decent as its key financial ratios have improved on the YoY basis in 1H FY 2019, which reflects that the company is possessing decent financial position. In the time frame of FY 2014- FY 2018, the company's top line and bottom line have witnessed a CAGR growth of 27.10% and 6.56%, respectively which can be considered at respectable levels. It looks like that the company has decent operational capabilities as its cash from operating activities have witnessed a CAGR growth of 31.04% in the time span from FY 2014- FY 2018.

Overview of 1H FY 2019 Results (Source: Company Reports)

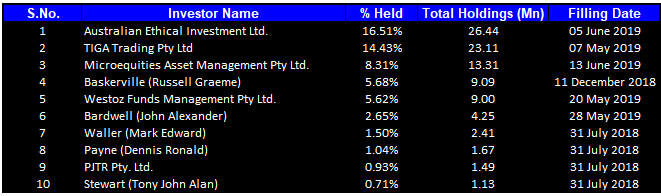

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 57.39% of the total shareholding. Australian Ethical Investment Ltd and TIGA Trading Pty Ltd hold the maximum interest in the company at 16.51% and 14.43%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

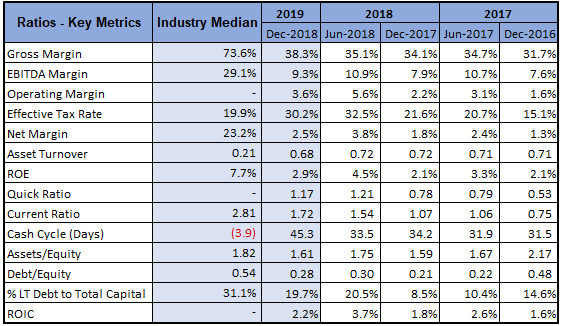

Decent Standing From Key Margins Perspective: The key margins of Empired Ltd have witnessed an improvement in 1H FY 2019 on the YoY basis as its net margin stood at 2.5%, which reflects a rise of 0.7% and, thus, it can be said that the company has been effectively converting its top line into bottom line. Also, the company gross margin and EBITDA margin stood at 38.3% and 9.3%, implying an increase of 4.2% and 1.4%, respectively on a YoY basis. The company’s current ratio stood at 1.72x, which implies an increase of 60.7% on the YoY basis that reflects that the company can meet its short-term obligations effectively. Talking about the leverage ratios, the company’s long-term debt percentage to total capital stood at 19.7% in 1H FY 2019, which is lower than the industry median of 31.1% and, thus, it can be said that the company total capital has lesser debt component as compared to the broader industry median. Debt to equity ratio stood at 0.28x in 1HFY19, which is lower than the industry median of 0.54x.

Key Metrics (Source: Thomson Reuters)

Announcement to Undertake On-market Share Buy Back: Empired Limited’s Directors have made an announcement about their intention to undertake the on-market share buy-back of up to maximum 15,269,298 shares over the twelve-month period starting July 17, 2019. As per the release dated July 2, 2019, the company is of the view that an on-market share buy-back happens to be an effective method of returning the capital to shareholders and it also stated that Empired’s shares are trading at the significant discount to the intrinsic value of the company. Additionally, there are expectations that the buyback might be earnings per share positive based on the existing circumstances.

A Look at Recent Update: Recently, Empired Limited had made an announcement that it has not been selected as the preferred bidder and has been selected as reserve bidder for Contract 125/17 - Provision of ICT Infrastructure and Systems Services 2018-2023 with Main Roads WA. The release also mentioned that, during the 2H, Main Roads has reduced services under the existing contract in preparation for transition to a new contract. The management is of the view that FY 2019 underlying EBITDA will be between $1.5 million and $2.0 million less than originally anticipated. Also, the revenue impact in FY 2020 is estimated to be around $10 million. The company is confident that the growth in other areas of the business would be offsetting this reduction and lead to relatively flat revenue growth in FY 2020.

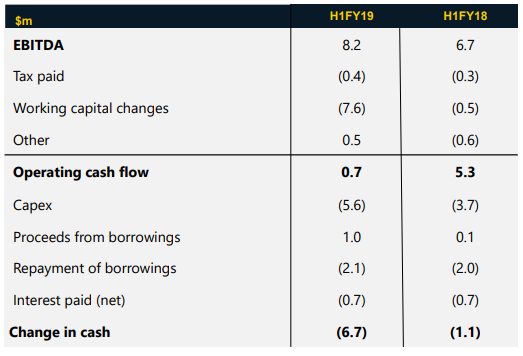

Understanding Empired’s Cash Flow and Financial Position: Empired Limited stated that its operating cash flow got impacted by the working capital outflow. However, there are expectations that the working capital in-flow in H2 FY 2019 would be delivering solid operating cash flow for a full year and net debt reduction at the end of the year. Further, the company stated that 2H FY 2019 capex would be lower than 1H FY 2019 which would be leading to the full year capex similar to that of FY 2018. Coming to the financial position, the company stated that the net debt had witnessed a rise to $15.4 million because of working capital outflow in H1 FY 2019 which would have the corresponding inflow in H2 FY 2019.

Cash Flow (Source: Company Reports)

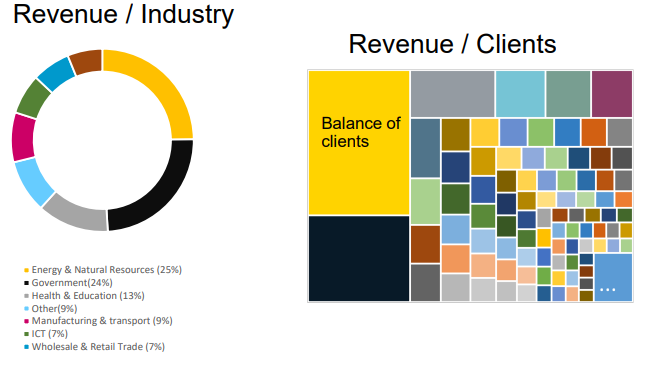

No Over-Reliance On Any Key Sector Might Support EPD: Empired stated that it does not have over-reliance on any key sector and there are expectations that this strategy might support the growth of the company moving forward. The company stated that it is focused towards the growth opportunities in Finance & Insurance on East Coast and that it is strongly positioned in the number of large corporate and government organisations for the expansion. The company also added that the YoY growth would be supported by the existing major clients.

Industry & Clients (Source: Company Reports)

What To Expect From Empired Moving Forward: There are expectations that, in FY 2020, Empired would be witnessing growth in the revenues and it has recently secured numerous new recurring managed services contracts plus the number of increases to the existing managed services contracts. There are expectations that these would be commencing the revenue generation in Q1 FY 2020. The company has confirmed that it anticipates an improvement in the EBITDA & material improvement in the NPAT & cash flow. The cost reduction programme had started, which would be delivered throughout FY 2020. The company stated that the material reduction in the capital investments is planned for FY 2020 and the focus is also on optimising the existing assets and driving the free cash flow generation throughout the year.

In FY 2019, the company is expected to post revenue between $174 million and $177 million. During the same period, the underlying EBITDA is anticipated to be between $15.2 million-$15.8 million.

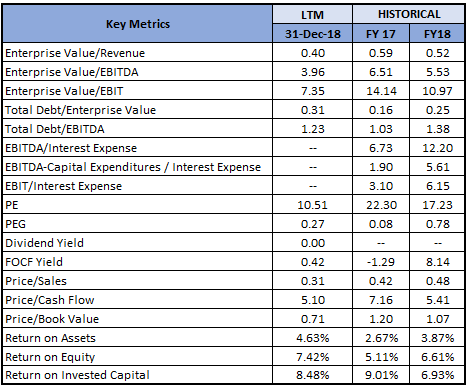

Key Valuation Metrics (Source: Thomson Reuters)

Outlook: On the outlook front, the company updated that it is conducting a review of the carrying value of the assets as part of its end of financial year processes, with expected completion prior to the finalisation of Empired’s FYY19 financial report. The company expects to incur a non-cash impairment charge in the range of $22 million to $25 million in the financial year 2019. As a result of the above anticipation, the company expects FY20 depreciation and amortisation to reduce to approximately $3.6 million prior to the adoption of AASB16 Leases. Cash flow, Operations and FY19 underlying EBITDA will not be impacted by the impairment charge. In addition, the company provided guidance of $14.3 million for net debt at 30 June 2019.

Stock Recommendation: The stock of the company generated returns of 28.00% and -17.95% over a period of 1 month and 3 months, respectively. In FY20, the company expects to witness improved margins, reduced capital expenditure and increased cash flow which will support its goal to commence the payment of dividends in the medium term. The first half of FY19 was characterised by an increase in key financial metrics including revenue, EBITDA and NPAT. Earnings per share for the period grew at a remarkable rate of 49% at 1.4 cents per share. During the period, the company witnessed a 64% rise in revenue owing solely to multi-year contracts and expects further growth in FY20 with increased SaaS revenue and managed services revenue. Over the coming 12 months, the company is expected to contest approximately $300 million pipelines of large multi-year contracts. In Australia, the company has a solid sales pipeline on the east coast for growth in the second half of 2019. Growth in Western Australia is dependent upon the success of Main Roads contract which is expected to expedite development in FY20. Further, the strengthening of Q4 sales pipeline for Auckland provides confidence in the company’s outlook. Currently, the stock is trading below the average of 52 week high and low prices of around $0.402 with reasonable PE multiple of 9.09x, indicating a decent opportunity for accumulation. Hence, considering the financial performance in the first half with a pipeline of large multi-year contracts expected to deliver growth in near future with recent guidance and risks being kept in mind, we recommend a “Speculative Buy” rating on the stock at a current market price of $0.350 (up 9.37% on 09 July 2019), and expect high single to low double-digit growth in the next 12-24 months.

EPD Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...